1. Introduction

India’s retirement environment is shifting from institution-led security to individual-led planning, driven by longer lifespans, rising post-retirement expenses, and the decline of guaranteed pension structures outside government service. In this context, the National Pension System has become a central pillar of India’s formal retirement framework, designed to help individuals convert long working years into a stable, inflation-adjusted retirement corpus through regulated, market-linked investing.

- Retirement planning in India is increasingly self-driven rather than employer-guaranteed

- Longevity and healthcare inflation have materially increased retirement funding requirements

- Market-linked instruments are now essential for long-term real wealth creation

- A regulated, low-cost pension structure improves predictability and governance

1.1 Overview of India’s National Pension System

The National Pension System (NPS) is a government-backed, defined-contribution retirement scheme that enables individuals to systematically invest over their earning life and accumulate a retirement corpus linked to capital market performance. It was created to bring structure, transparency, and professional fund management to retirement savings, replacing fragmented or informal approaches with a nationally regulated pension architecture.

- Operates under a clear regulatory framework with independent oversight

- Separates account administration, fund management, and custody for transparency

- Allows investors to participate in equity and debt markets within defined limits

- Emphasizes long-term accumulation rather than short-term return optimization

1.2 Role of NPS in Long-Term Retirement Planning

For professionals, entrepreneurs, and self-employed individuals, the National Pension System functions as a strategic retirement planning tool rather than a standalone investment product. Its long lock-in period enforces financial discipline, while its cost-efficient structure enhances compounding over multi-decade horizons, making it particularly relevant for those building retirement wealth without relying on traditional pensions.

- Encourages consistent, goal-aligned retirement contributions over time

- Supports retirement planning even with irregular or non-salaried income

- Reduces the erosion of returns through one of the lowest cost structures in India

- Complements other long-term assets to create diversified retirement income sources

2. Why the National Pension System Matters

India’s pension framework has transitioned from limited, employer-centric arrangements to a broader, individual-driven model of retirement preparedness. The National Pension System (NPS) matters because it was designed to address structural gaps in retirement coverage by combining regulatory oversight, market participation, and cost discipline into a single, scalable framework suited for a modern workforce.

- Traditional pension access has been restricted to a small segment of the population

- Informal retirement saving often lacks discipline, diversification, and governance

- Long-term financial security now depends on structured, self-managed planning

- A national pension architecture improves consistency and transparency

2.1 Evolution of NPS in India’s Pension Ecosystem

The development of NPS reflects India’s broader shift toward contributory retirement systems, where outcomes depend on long-term savings behavior rather than guaranteed payouts. Initially introduced for government employees, the framework was later expanded to include private-sector professionals, entrepreneurs, and self-employed individuals, integrating retirement planning into the mainstream financial ecosystem.

- Transitioned India away from unfunded pension promises toward sustainable models

- Expanded coverage beyond government employment to the wider workforce

- Introduced professional fund management into retirement savings

- Created a unified pension framework with national portability

2.2 Cost Efficiency and Low-Expense Advantage

One of the defining strengths of the National Pension System (NPS) is its cost structure, which is materially lower than most long-term investment and pension products in India. By minimizing fund management and administrative expenses, the system ensures that a larger portion of investor contributions remains invested and compounds over time, directly improving retirement outcomes.

- Ultra-low expense ratios reduce long-term return leakage

- Transparent fee disclosure improves investor accountability

- Lower costs significantly enhance net corpus over multi-decade periods

- Efficient scale benefits are passed directly to contributors

2.3 Impact of Compounding Over Long Investment Horizons

Retirement planning is fundamentally a long-duration exercise, and NPS is structured to maximize the benefits of compounding across extended timeframes. By encouraging early entry, consistent contributions, and disciplined investing, the system allows market-linked returns to accumulate meaningfully, even when annual contributions appear modest in isolation.

- Long holding periods amplify the effect of reinvested returns

- Small, regular contributions can grow into substantial retirement capital

- Market-linked growth helps offset inflation over decades

- Time in the market often matters more than timing the market

3. Types of NPS Accounts

The account structure under the National Pension System (NPS) is intentionally segmented to separate long-term retirement discipline from optional liquidity. This design allows investors to anchor retirement planning in a locked-in framework while retaining flexibility for supplementary investments aligned with evolving financial goals.

- Two distinct account types serve different planning objectives

- Retirement discipline and liquidity are deliberately segregated

- Account choice influences tax treatment, withdrawals, and usage

- Strategic alignment with life-stage goals is critical

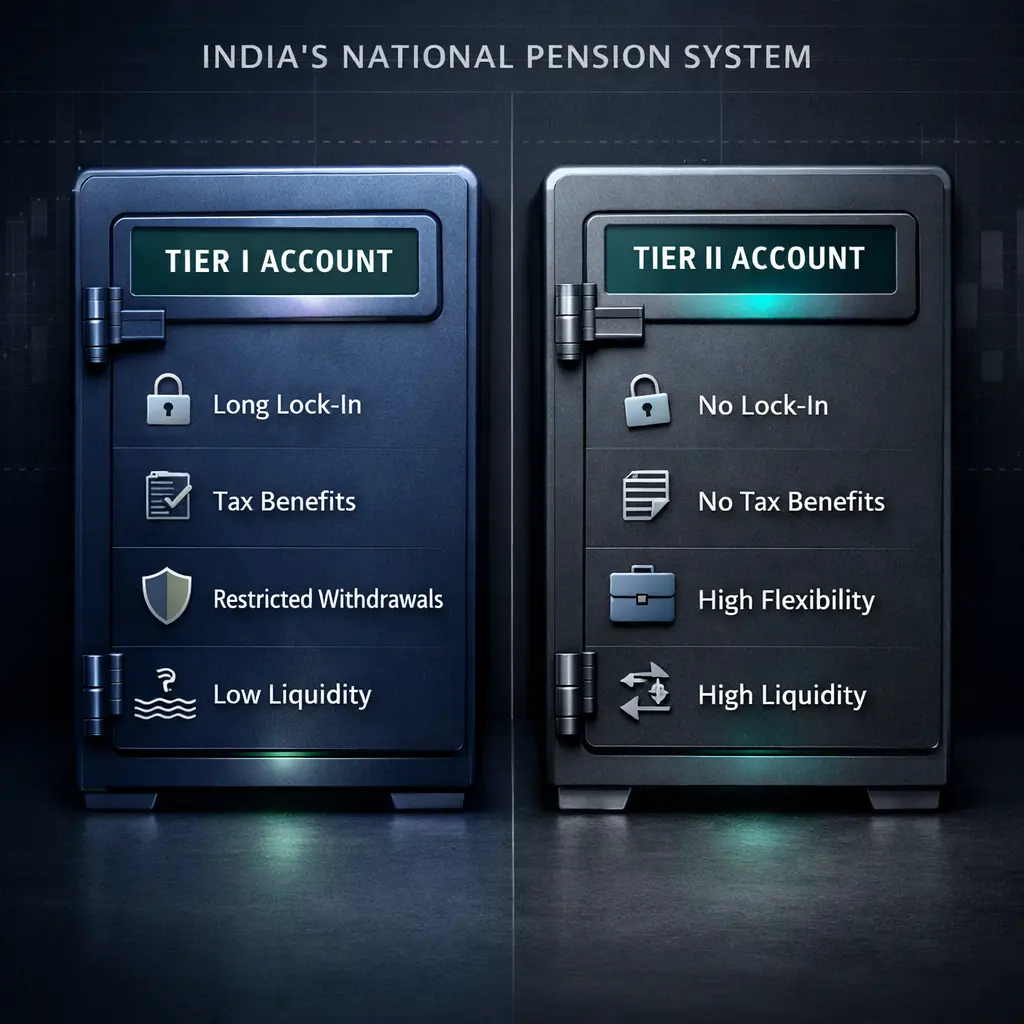

3.1 Tier I Account

The Tier I account is the core retirement account and the foundation of long-term participation in NPS. It is designed to enforce disciplined savings by restricting withdrawals, ensuring that contributions remain invested through the accumulation phase and are converted into retirement income at maturity.

- Mandatory for all NPS subscribers

- Subject to lock-in until retirement age, with limited exit options

- Eligible for statutory tax benefits tied to retirement savings

- Structured to prioritize corpus creation over short-term access

3.2 Tier II Account

The Tier II account functions as a voluntary, flexible investment account that operates alongside Tier I but without retirement-specific restrictions. It allows contributors to invest surplus funds using the same fund management framework while retaining full liquidity, making it a tactical extension rather than a retirement anchor.

- The optional account is activated only after Tier I is opened

- Allows unrestricted deposits and withdrawals

- No mandatory retirement lock-in or annuity requirement

- Better suited for medium-term allocation than retirement income

3.3 Choosing the Right Account Based on Financial Goals

Selecting between Tier I and Tier II is less about preference and more about purpose. Tier I aligns with long-term retirement security, while Tier II supports liquidity-driven objectives, making it essential to map each account to a clearly defined financial goal within an overall wealth strategy.

- Use Tier I for non-negotiable retirement corpus building

- Allocate Tier II only after core retirement funding is secured

- Match account selection with time horizon and income stability

- Avoid using Tier II as a substitute for disciplined retirement saving

4. How NPS Works: Investment and Contribution Mechanics

The operational design of the National Pension System (NPS) is built around simplicity, scalability, and long-term discipline. Its contribution and investment mechanics are structured to accommodate varied income profiles while maintaining centralized oversight, ensuring that retirement savings remain systematic, traceable, and aligned with long-term objectives rather than short-term market behavior.

- Contributions are investor-driven rather than mandate-driven

- Investment flows are automated once preferences are set

- Centralized administration ensures continuity and accuracy

- System design balances flexibility with retirement discipline

4.1 Contribution Rules

NPS follows a defined-contribution model where retirement outcomes depend on the amount invested and the duration of participation rather than promised payouts. The system sets basic minimum thresholds to ensure account activity while allowing contributors to scale investments based on their financial capacity and planning horizon.

- Minimum annual contribution requirements ensure account continuity

- No upper limit on contributions supports accelerated corpus building

- Contributions can be made by individuals or through employers

- Retirement accumulation is directly linked to consistency of funding

4.2 Contribution Flexibility

A key strength of NPS lies in its adaptability to changing income patterns, making it particularly suitable for professionals and entrepreneurs. Contributors can adjust both the amount and timing of investments, enabling alignment with cash flows, business cycles, and career transitions without disrupting long-term retirement planning.

- Supports irregular or variable income streams

- Allows multiple contributions within a financial year

- Enables scaling up investments during high-income phases

- Reduces dependency on rigid monthly saving commitments

4.3 Role of Central Recordkeeping Agency (CRA)

The Central Recordkeeping Agency serves as the operational backbone of NPS, maintaining individual account records and ensuring seamless coordination between contributors, fund managers, and intermediaries. This centralized system enhances transparency, reduces operational risk, and preserves account portability across jobs and geographies.

- Maintains a single permanent retirement account for each subscriber

- Tracks contributions, investments, and transactions in real time

- Enables portability across employers and employment types

- Strengthens governance through standardized record management

5. Employer Contribution and Corporate NPS

Employer participation strengthens retirement outcomes by converting workplace benefits into long-term financial security rather than short-term compensation. Within the National Pension System (NPS) framework, employer contributions and corporate participation enable organizations and employees to align compensation structures with sustainable retirement planning while improving cost efficiency and workforce stability.

- Employer-supported retirement benefits enhance long-term employee retention

- Structured pension contributions reduce reliance on ad hoc retirement planning

- Corporate participation improves predictability of post-retirement outcomes

- Shared responsibility strengthens retirement discipline

5.1 Employer-Sponsored NPS

Employer-sponsored NPS allows organizations to contribute directly to an employee’s retirement account as part of the compensation framework. This approach shifts retirement planning from an individual-only responsibility to a shared model, improving participation rates and long-term financial outcomes without increasing administrative complexity.

- Employer contributions supplement individual retirement savings

- Integrated seamlessly into payroll and HR systems

- Enhances perceived value of total compensation packages

- Encourages consistent long-term participation

5.2 Tax Efficiency of Employer Contributions

Employer contributions to NPS are structured to deliver tax efficiency for both the organization and the employee. By directing a portion of compensation into retirement savings, companies can reduce tax outflows while employees benefit from higher effective take-home value over the long term.

- Employer contributions are excluded from the employee’s taxable income up to limits

- Organizations benefit from deductible retirement expenses

- Improves post-tax retirement accumulation without increasing cash salary

- Creates a more efficient compensation structure

5.3 Corporate NPS for Structured Retirement Planning

Corporate NPS enables organizations to formalize retirement planning across their workforce using a standardized framework. This structure supports long-term financial well-being, reduces employee financial stress, and indirectly contributes to higher productivity and engagement levels.

- Establishes a uniform retirement benefit across employee categories

- Reduces uncertainty around post-retirement financial readiness

- Aligns corporate governance with employee welfare objectives

- Supports workforce stability and long-term organizational planning

6. Fund Management and Investment Choices

Investment performance within the National Pension System (NPS) is driven not by static returns but by how effectively contributions are managed, allocated, and adjusted over time. This section explains how fund management works, the strategic choices available to investors, and how asset allocation evolves across a working lifetime to balance growth and risk.

- Market-linked structure focused on long-term compounding rather than guaranteed returns

- Regulated fund management framework with clear accountability

- Multiple investment approaches aligned to different risk appetites

- Built-in mechanisms to adjust risk as retirement approaches

6.1 Pension Fund Managers

Pension Fund Managers (PFMs) are responsible for investing subscriber contributions across approved asset classes within defined regulatory limits. Their role is not speculative trading, but disciplined capital deployment aimed at steady, risk-adjusted growth over decades. In the National Pension System (NPS), investors can choose their preferred fund manager, introducing an element of performance accountability rarely seen in traditional retirement products.

- PFMs operate under strict oversight and investment mandates

- Performance is measured over long horizons, not short-term volatility

- Managers invest across equity, corporate debt, and government securities

- Switching PFMs is permitted, enabling performance-driven decision-making

6.2 Active vs Auto Choice

Investment choice determines how much control an investor exercises over asset allocation. Active Choice suits financially informed individuals who want to decide exposure levels, while Auto Choice is designed for those who prefer a structured, age-linked approach. Within the National Pension System (NPS), both options coexist to serve different decision-making styles without compromising regulatory safeguards.

- Active Choice offers flexibility to set asset allocation caps

- Auto Choice follows predefined allocation paths based on age

- Risk exposure is transparent and rule-based in both options

- Switching between choices is allowed as financial maturity evolves

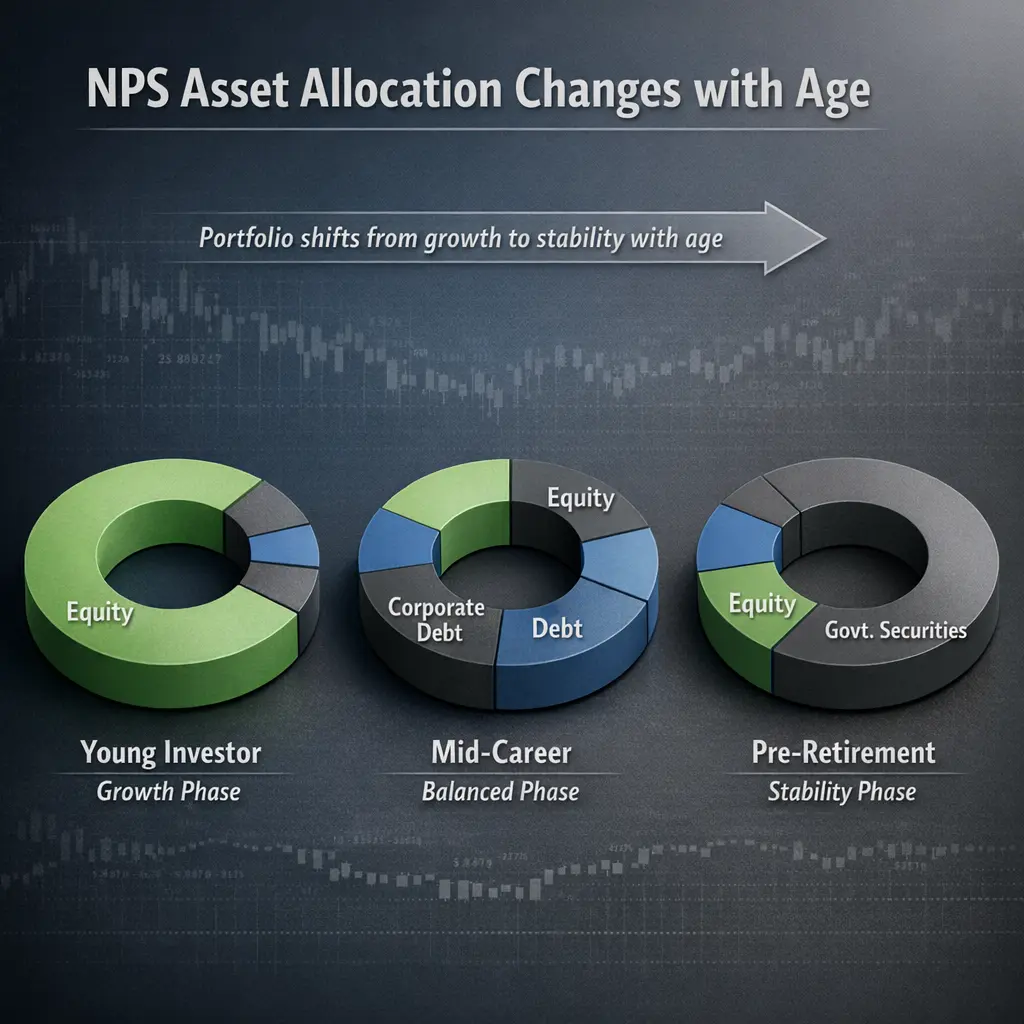

6.3 Lifecycle Asset Allocation

Lifecycle allocation gradually shifts investments from growth-oriented assets to stability-focused instruments as retirement nears. This approach recognizes that risk tolerance is not static and should evolve with income security and time horizon. In the National Pension System (NPS), lifecycle models are designed to reduce downside risk while preserving accumulated gains.

- Higher equity exposure in early earning years for growth

- Progressive reduction in volatility closer to retirement

- Automatic rebalancing reduces emotional investment decisions

- Designed to protect retirement corpus from late-stage market shocks

7. NPS Asset Classes and Portfolio Construction

Portfolio construction within the National Pension System (NPS) is designed to balance growth, stability, and risk management across long investment horizons. By offering multiple asset classes under a regulated framework, the system enables investors to align retirement portfolios with age, risk tolerance, and income visibility while maintaining diversification and cost efficiency.

- Asset allocation drives long-term retirement outcomes more than product selection

- Diversification reduces dependency on any single market cycle

- Risk exposure is calibrated through predefined asset class limits

- Portfolio design evolves across different life stages

7.1 Equity

Equity exposure within NPS serves as the primary engine for long-term capital growth, particularly during the early and mid-career phases. Allocations to equities allow retirement portfolios to participate in economic expansion and corporate earnings growth, helping counter inflation over multi-decade periods under the National Pension System (NPS) framework.

- Highest long-term return potential among available asset classes

- Greater short-term volatility compared to fixed-income assets

- Most effective when combined with long investment horizons

- Gradually reduced as retirement approaches to manage risk

7.2 Corporate Debt

Corporate debt investments provide income stability while offering returns superior to government securities over time. This asset class plays a critical role in smoothing portfolio volatility by generating predictable cash flows from high-quality corporate issuers.

- Lower volatility compared to equity investments

- Returns linked to credit quality and interest rate cycles

- Supports steady portfolio growth during market fluctuations

- Acts as a stabilizer within diversified retirement portfolios

7.3 Government Securities

Government securities anchor portfolio stability by prioritizing capital preservation and predictable returns. Within the National Pension System (NPS), this asset class is particularly relevant during the later stages of retirement planning, when protection from market volatility becomes increasingly important.

- Backed by sovereign credit, minimizing default risk

- Lower return potential compared to equity and corporate debt

- Highly sensitive to interest rate movements

- Enhances portfolio resilience near retirement

7.4 Alternative Assets

Alternative assets introduce diversification benefits by reducing correlation with traditional equity and debt markets. Though allocated in limited proportions, they enhance risk-adjusted returns and portfolio efficiency under the National Pension System (NPS) investment structure.

- Includes assets such as infrastructure and real estate-linked instruments

- Low correlation with conventional asset classes

- Enhances diversification without dominating portfolio risk

- Exposure is capped to maintain overall portfolio stability

Comparative View of NPS Asset Classes

| Asset Class | Primary Objective | Risk Level | Role in Retirement Portfolio |

|---|---|---|---|

| Equity | Long-term growth | High | Inflation protection and wealth creation |

| Corporate Debt | Income and stability | Moderate | Volatility control with return potential |

| Government Securities | Capital preservation | Low | Portfolio safety and predictability |

| Alternative Assets | Diversification | Moderate | Risk-adjusted return enhancement |

10. Returns, Performance, and Long-Term Wealth Creation

Retirement outcomes under NPS are driven not by short-term performance but by sustained participation across market cycles. The return profile of the National Pension System (NPS) reflects disciplined asset allocation, low costs, and time-driven compounding, making it a long-horizon wealth creation vehicle rather than a tactical investment product.

- Returns vary by asset allocation and investment horizon

- Performance must be evaluated over full market cycles

- Cost efficiency materially improves net long-term outcomes

- Consistency matters more than annual return rankings

10.1 Historical Returns

Historically, NPS has delivered competitive long-term returns by combining equity-led growth with debt-driven stability. While annual performance fluctuates, extended holding periods have demonstrated the system’s ability to generate real returns that outpace inflation for disciplined contributors.

- Equity-oriented portfolios have delivered higher long-term growth

- Debt-heavy allocations have provided stability with moderate returns

- Performance improves meaningfully beyond 10–15 year horizons

- Return dispersion narrows as investment duration increases

10.2 Market Cycles

Market cycles play a significant role in shaping interim NPS performance, but their impact diminishes over time. The structure of the National Pension System (NPS) is designed to absorb volatility through diversification and lifecycle-based asset allocation, reducing the risk of poor timing decisions near retirement.

- Short-term volatility is inherent in market-linked investments

- Diversification cushions portfolios during downturns

- Lifecycle allocation gradually reduces risk exposure with age

- Long participation periods smooth cyclical fluctuations

10.3 Compounding Effect

The most powerful driver of retirement wealth under NPS is compounding, enabled by early entry, regular contributions, and reinvestment of returns. When combined with the low-cost structure of the National Pension System (NPS), compounding transforms incremental savings into a substantial retirement corpus over decades.

- Early contributions have disproportionate long-term impact

- Low expenses allow returns to compound more efficiently

- Time in the system outweighs contribution size in early years

- Consistent investing amplifies wealth creation exponentially

11. Cost Structure and Transparency in NPS

Cost efficiency is one of the most underappreciated drivers of long-term retirement outcomes. The National Pension System (NPS) is structured to minimize investment and administrative expenses, ensuring that a larger share of contributions remains invested and compounds over time rather than being eroded by fees.

- Costs directly influence net retirement returns over long horizons

- Transparency improves investor confidence and accountability

- Lower expenses magnify the benefits of compounding

- Fee discipline is critical in long-duration retirement products

11.1 Expense Ratios

Expense ratios under NPS are among the lowest across Indian investment products, reflecting the system’s scale-driven and regulator-monitored design. These low charges significantly reduce performance drag, especially when investments are held over multiple decades.

- Fund management charges are a fraction of typical mutual fund costs

- Administrative fees are standardized and tightly regulated

- Lower costs improve return predictability over time

- Cost savings compound meaningfully across long holding periods

11.2 Comparison with Other Products

When compared with traditional pension plans, insurance-linked products, and actively managed funds, NPS stands out for its structural cost advantage. The National Pension System (NPS) separates distribution, fund management, and custody, reducing embedded commissions and opacity that often inflate investor costs elsewhere.

- No high upfront commissions or embedded sales incentives

- Clear segregation of roles reduces cost duplication

- Lower total expense ratios than most long-term alternatives

- Greater transparency than bundled pension or insurance products

11.3 Long-Term Cost Impact

Over a 25–30 year investment horizon, even small differences in annual costs can translate into large variations in retirement corpus. The low-cost architecture of the National Pension System (NPS) allows compounding to work efficiently, directly enhancing real retirement wealth without increasing contribution levels.

- Reduced fee leakage preserves more invested capital

- Compounding amplifies cost savings over decades

- Net returns improve without taking additional market risk

- Cost discipline strengthens long-term retirement certainty

12. Tax Benefits under NPS

Tax efficiency significantly enhances the effectiveness of retirement planning, especially for high-income professionals and entrepreneurs. The National Pension System (NPS) integrates multiple tax provisions that reward long-term discipline while reducing current tax liability, making it a structurally efficient retirement vehicle rather than merely a tax-saving option.

- Tax incentives are aligned with long-term retirement objectives

- Benefits apply across salaried and self-employed profiles

- Multiple sections allow layered tax optimization

- Tax efficiency directly improves net retirement corpus

12.1 Section 80CCD(1)

Section 80CCD(1) covers individual contributions made to NPS and forms the foundational tax benefit for most subscribers. This provision allows contributors to claim deductions within the overall limits of income-tax law, linking retirement savings directly to annual tax planning.

- Applicable to both salaried individuals and self-employed taxpayers

- Deduction is linked to a percentage of income rather than a flat cap

- Encourages systematic annual retirement contributions

- Works in conjunction with other Section 80C investments

12.2 Section 80CCD(1B)

Section 80CCD(1B) provides an exclusive additional deduction over and above standard limits, specifically to promote higher retirement savings. This provision materially improves tax-adjusted returns and strengthens the long-term appeal of the National Pension System (NPS) for individuals with surplus saving capacity.

- Offers an additional deduction beyond Section 80C limits

- Designed exclusively for retirement-focused contributions

- Particularly beneficial for mid- to high-income earners

- Enhances long-term compounding through higher investible surplus

12.3 Section 80CCD(2)

Section 80CCD(2) applies to employer contributions and is one of the most powerful yet underutilized tax provisions within NPS. By shifting part of compensation into structured retirement savings, both employers and employees can achieve meaningful tax efficiency under the National Pension System (NPS) framework.

- Employer contributions are deductible separately from individual limits

- Not counted within Section 80C or 80CCD(1B) caps

- Reduces taxable salary without reducing retirement benefits

- Supports structured, employer-led retirement planning

Summary of Tax Benefits under NPS

| Tax Section | Applicable To | Nature of Benefit | Strategic Value |

|---|---|---|---|

| 80CCD(1) | Individual contribution | Income-based tax deduction | Core retirement tax efficiency |

| 80CCD(1B) | Additional contribution | Extra deduction beyond standard limits | Enhanced long-term wealth creation |

| 80CCD(2) | Employer contribution | Separate deduction from salary income | Optimized compensation structuring |

13. NPS vs Other Retirement Instruments

Retirement planning in India offers multiple avenues, but each instrument differs in risk, return potential, liquidity, and tax treatment. The National Pension System (NPS) distinguishes itself by combining market-linked growth with structured long-term discipline, making it a strategic complement rather than a direct replacement for traditional savings products.

- Comparative evaluation helps align retirement goals with investment choice

- Understanding risk-adjusted returns ensures portfolio efficiency

- Cost and tax structure materially influence long-term corpus

- Diversification across instruments mitigates dependency on a single product

13.1 EPF & VPF

The Employees’ Provident Fund (EPF) and its voluntary extension, VPF, offer guaranteed returns and capital protection. While ideal for risk-averse salaried employees, these instruments have limited growth potential and minimal equity exposure, constraining long-term wealth creation compared with market-linked frameworks like NPS.

- Provides fixed, predictable interest on contributions

- Full capital safety and government-backed guarantee

- Limited inflation-adjusted growth over multi-decade horizons

- Less flexibility in asset allocation compared to NPS

13.2 PPF & Pension Plans

Public Provident Fund (PPF) and traditional pension plans are long-term instruments emphasizing capital protection and tax efficiency. These products offer stability but often fall short in generating substantial corpus in real terms due to capped interest rates and limited exposure to equities, which are crucial for long-horizon compounding.

- Low-risk, government-secured returns

- Tax benefits under Section 80C and maturity exemptions

- Interest rate caps limit long-term compounding potential

- Suitable as a safety layer but insufficient alone for retirement adequacy

13.3 Mutual Funds for Retirement

Mutual funds provide diversified market exposure with flexibility in asset allocation, making them attractive for long-term growth. However, they lack the structural discipline and mandatory retirement orientation of NPS, and costs can erode returns if portfolios are actively managed or held inefficiently.

- Potential for high returns through diversified equity and debt exposure

- Flexible contribution and withdrawal schedules

- Expense ratios can materially reduce net corpus over decades

- Absence of retirement-specific lock-in reduces enforced discipline

14. Withdrawal Rules and Exit Options

Understanding the withdrawal and exit framework is critical to maximizing the strategic value of the National Pension System (NPS). The system is designed to ensure that accumulated retirement savings are deployed efficiently post-retirement while maintaining regulatory oversight, predictable cash flows, and tax efficiency.

- Retirement corpus is primarily preserved for long-term income generation

- Withdrawal rules balance flexibility with structured retirement discipline

- Exit options are aligned with annuity requirements and tax treatment

- Clear rules enhance predictability of retirement income

14.1 Maturity Rules

The NPS mandates that accounts remain active until the subscriber reaches retirement age, generally 60 years, to ensure corpus accumulation. Subscribers can, however, continue beyond 60 under certain conditions, reinforcing the system’s objective of providing sustained post-retirement income.

- Mandatory maturity age ensures disciplined long-term saving

- Option to extend account beyond 60 for delayed retirement

- Encourages gradual accumulation and reduces premature depletion

- Preserves principal while allowing strategic planning for retirement needs

14.2 Lump Sum & Annuity

Upon reaching maturity, a portion of the NPS corpus can be withdrawn as a lump sum, while the remainder must be converted into an annuity to provide regular retirement income. This balance ensures liquidity while safeguarding against the risk of exhausting retirement savings prematurely.

- Up to 60% of corpus may be withdrawn as lump sum

- Remaining 40% must be used to purchase an annuity

- Annuity provides stable post-retirement cash flows

- Flexibility in lump sum withdrawal supports one-time financial needs

14.3 Taxation on Exit

Tax treatment at the point of exit is a key consideration for NPS investors. While lump sum withdrawals are partially tax-exempt, annuity income is taxable, making it essential for retirement planning to account for post-tax income rather than gross corpus alone.

- Lump sum withdrawals enjoy partial tax exemption under current law

- Annuity payments are treated as taxable income

- Effective planning reduces post-retirement tax liability

- Understanding tax implications is critical for accurate retirement budgeting

15. Partial and Premature Withdrawals

While the National Pension System (NPS) is designed to promote long-term retirement discipline, it also allows for partial or premature withdrawals under defined circumstances. These rules provide flexibility for life events or financial contingencies without compromising the overall objective of building a sustainable retirement corpus.

- Withdrawal options are structured to balance liquidity with long-term planning

- Premature access is regulated to prevent erosion of retirement capital

- Flexibility enhances appeal for professionals with variable income streams

- Strategic use can address critical financial needs while maintaining corpus growth

15.1 Conditions

Partial and premature withdrawals are permitted only under specific conditions such as higher education, medical emergencies, or purchase of a first home. The system mandates formal approval and documentation to ensure withdrawals serve meaningful purposes rather than discretionary spending.

- Eligible only for defined life events like health or education needs

- Requires submission of proof and regulatory approval

- Maintains the integrity of long-term retirement savings

- Encourages disciplined use rather than ad hoc access

15.2 Limits

The system caps withdrawal amounts to preserve the majority of the retirement corpus. Typically, only a fraction of the accumulated contributions can be withdrawn, with remaining funds continuing to grow under the National Pension System (NPS) framework.

- Partial withdrawals generally capped at a percentage of total contributions

- Frequency of withdrawals is restricted to maintain investment continuity

- Limits prevent significant depletion of retirement corpus

- Ensures that long-term compounding benefits are largely preserved

15.3 Financial Impact

Even limited withdrawals can have a measurable impact on long-term corpus growth due to the compounding effect over decades. Subscribers need to carefully evaluate the trade-off between immediate liquidity and potential reduction in retirement wealth.

- Early withdrawals reduce the base for long-term compounding

- Potential loss of future growth may outweigh short-term benefits

- Strategic planning mitigates adverse effects on retirement corpus

- Understanding financial impact ensures informed withdrawal decisions

16. Annuity Planning under NPS

Annuity planning is the final stage of the National Pension System (NPS), converting the accumulated retirement corpus into a structured stream of income. Effective annuity selection ensures predictable cash flows, mitigates longevity risk, and complements other retirement assets to create a financially secure post-retirement life.

- Annuities provide guaranteed income for life or a fixed period

- Choice of provider and plan directly affects post-retirement financial stability

- Inflation-linked considerations are essential for maintaining real purchasing power

- Structured payouts support long-term financial planning and lifestyle continuity

16.1 Providers

Subscribers must select from approved insurance providers to purchase annuity plans under NPS. The regulatory framework ensures credibility, risk management, and timely payments while providing multiple options suited to different retirement objectives.

- Only IRDAI-approved insurance companies offer NPS annuities

- Providers are evaluated for financial stability and claim settlement record

- Choice of provider affects returns, fees, and service quality

- Regulatory oversight ensures consistent and secure payouts

16.2 Payout Structures

Annuity payouts under NPS can be customized to meet individual needs, including lifetime income, joint-life coverage, or fixed-term payments. The selection of payout structure directly influences monthly cash flow, flexibility, and financial resilience in retirement.

- Options include life annuity, joint-life annuity, and period certain plans

- Payout frequency can be monthly, quarterly, half-yearly, or yearly

- Structured payouts reduce the risk of depleting corpus prematurely

- Choice should align with personal cash flow requirements and dependency obligations

16.3 Inflation Risk

While annuities provide stability, fixed payouts are exposed to inflation risk over long retirements. Considering inflation-adjusted annuities or combining NPS with other inflation-protected assets can help maintain real purchasing power and ensure sustainable lifestyle post-retirement.

- Fixed payouts may erode purchasing power over decades

- Inflation-linked annuities provide partial protection against rising costs

- Diversifying with market-linked instruments mitigates long-term inflation risk

- Strategic planning ensures the retirement income maintains its real value over time

17. Risks and Limitations of NPS

While the National Pension System (NPS) offers structured retirement savings and long-term wealth creation, it is not without inherent risks. Understanding these limitations is crucial for professionals and entrepreneurs to align NPS participation with overall financial planning and risk tolerance.

- Market-linked returns introduce variability in retirement corpus

- Liquidity constraints can limit access to funds before retirement

- Regulatory changes may alter contribution rules or tax benefits

- Awareness of risks ensures more informed decision-making

17.1 Market Risk

Since NPS investments include equities and corporate debt, performance is subject to market fluctuations. Subscribers should recognize that short-term volatility may impact interim returns, although long-term participation generally smooths cyclical swings.

- Equity allocation exposes portfolios to stock market volatility

- Corporate debt performance is influenced by interest rates and credit quality

- Diversified asset allocation mitigates concentration risk

- Long-term horizon reduces the impact of short-term market downturns

17.2 Liquidity

Liquidity is a notable limitation of NPS, particularly for Tier I accounts, which are locked until retirement with restricted withdrawal options. While Tier II accounts offer flexibility, premature access can incur penalties and reduce the benefits of compounding.

- Tier I contributions are largely illiquid until maturity

- Partial withdrawals are subject to conditions and caps

- Liquidity limitations encourage disciplined saving behavior

- Early withdrawals can materially reduce the retirement corpus

17.3 Regulatory Risk

Changes in government policy, tax laws, or investment guidelines can affect NPS operations and returns. While the system is regulated and generally stable, subscribers must stay informed about regulatory developments that may impact contributions, withdrawals, or tax efficiency.

- Alterations in tax treatment may change net retirement outcomes

- Investment limits and asset class rules can be revised

- Regulatory changes may affect annuity purchase requirements

- Monitoring updates ensures strategic adjustments to retirement planning

18. Tracking and Managing NPS Investments

Effective management of the National Pension System (NPS) requires disciplined monitoring and organized record-keeping. By combining regular portfolio tracking with digital tools, subscribers can optimize asset allocation, ensure compliance with contribution schedules, and maintain clarity over retirement planning progress.

- Active monitoring enhances long-term wealth creation

- Digital tools improve organization and decision-making efficiency

- Document management ensures compliance and audit readiness

- Informed tracking supports strategic retirement planning

18.1 Portfolio Monitoring

Regular tracking of NPS portfolios allows subscribers to evaluate performance, assess asset allocation, and make adjustments aligned with retirement goals. Monitoring enables proactive responses to market changes while preserving the long-term focus of the plan.

- Track equity, corporate debt, and government security allocations

- Assess performance against historical benchmarks

- Adjust contribution or allocation strategy if risk tolerance changes

- Helps identify underperforming funds early to optimize returns

18.2 Using My Wealth Locker

Digital wealth management platforms like My Wealth Locker offer subscribers an integrated approach to manage NPS alongside other investments. The platform provides a consolidated view of contributions, fund performance, and retirement projections without promotional emphasis, enhancing strategic decision-making.

- Centralizes NPS and other wealth instruments in one dashboard

- Enables real-time tracking of contributions and fund performance

- Supports scenario analysis for retirement planning

- Reduces administrative burden and improves portfolio oversight

18.3 Document Organization

Organized record-keeping is critical for compliance, tax reporting, and audit readiness. Proper management of NPS statements, annuity contracts, and contribution receipts ensures smooth administration and supports long-term financial planning.

- Store account statements, tax receipts, and annuity documents systematically

- Facilitates easy access during regulatory or personal reviews

- Reduces risk of missing critical deadlines or submissions

- Enhances clarity and control over retirement savings trajectory

19. Real-World Use Cases of NPS

The National Pension System (NPS) demonstrates practical value across diverse professional and financial profiles. By structuring retirement savings in a disciplined, cost-efficient, and market-linked framework, it serves as a cornerstone for long-term wealth creation and financial security.

- NPS caters to different income types and career stages

- Long-term discipline enables sustainable corpus accumulation

- Flexible contribution options support life-cycle planning

- Real-world adoption illustrates measurable retirement outcomes

19.1 Salaried Professionals

For salaried employees, NPS offers a structured, tax-efficient retirement vehicle integrated with employer contributions. This enables individuals to systematically build a retirement corpus while benefiting from payroll-based convenience and regulatory incentives.

- Automatic contributions via payroll improve consistency

- Employer participation enhances retirement corpus

- Tax benefits amplify net savings and long-term wealth

- Reduces dependency on ad hoc retirement planning measures

19.2 Self-Employed & Entrepreneurs

Entrepreneurs and self-employed professionals often face irregular income streams. NPS provides flexibility in contributions while still enforcing long-term discipline, making it a suitable retirement planning tool for non-salaried individuals.

- Contribution amounts can be tailored to fluctuating cash flows

- Ensures retirement savings without compromising operational liquidity

- Supports long-term wealth creation alongside business growth

- Facilitates disciplined investing despite variable income cycles

19.3 Early Investors

Early entry into NPS maximizes the power of compounding, converting modest contributions into a significant retirement corpus over decades. This use case highlights the strategic value of starting young to achieve financial independence and sustainable retirement outcomes.

- A longer investment horizon magnifies compounding benefits

- Early contributions require a lower absolute monthly commitment

- Reduces pressure on later-life savings to meet retirement goals

- Provides flexibility in risk-adjusted asset allocation over career span

20. Strategic Role of NPS in Retirement Planning

The National Pension System (NPS) serves as a strategic pillar in a comprehensive retirement plan, balancing long-term growth with financial security. By integrating disciplined contributions, asset allocation, and regulatory benefits, NPS enables professionals and entrepreneurs to systematically build a retirement corpus while managing risk and optimizing tax efficiency.

- NPS complements other retirement instruments for a holistic strategy

- Balances growth potential with capital preservation over decades

- Supports scenario-based planning and portfolio adjustments

- Enables alignment with personal financial goals and lifestyle aspirations

20.1 Holistic Strategy

Incorporating NPS into a broader retirement framework allows individuals to align contributions, asset allocation, and risk tolerance with life-stage requirements. Its structured approach ensures retirement wealth creation is consistent and predictable, reducing reliance on ad hoc investment decisions.

- Integrates seamlessly with PF, PPF, mutual funds, and other instruments

- Encourages disciplined saving behavior over the entire career

- Provides flexibility for contribution scaling as income grows

- Enhances overall retirement corpus through consistent market participation

20.2 Growth vs Security

NPS allows subscribers to balance equity exposure for long-term growth with fixed-income assets for stability. This lifecycle approach mitigates volatility while ensuring that retirement savings continue to appreciate, reflecting the strategic duality of growth and security.

- Early-stage investors can emphasize equities for higher returns

- Gradual shift to debt and government securities preserves capital near retirement

- Asset allocation options are customizable to risk appetite

- Strategic diversification reduces exposure to market downturns

20.3 My Wealth Locker Integration

Digital wealth management platforms like My Wealth Locker enable comprehensive tracking and planning of NPS investments within a broader financial ecosystem. Integration facilitates performance monitoring, document organization, and scenario analysis without promotional emphasis, enhancing strategic oversight of retirement planning.

- Consolidates NPS and other assets in a single interface

- Provides insights into portfolio performance and future projections

- Simplifies management of contributions, statements, and annuities

- Supports informed decision-making and long-term retirement planning

21. Key Considerations Before Investing

Investing in the National Pension System (NPS) requires careful evaluation of personal financial circumstances, risk tolerance, and retirement objectives. Strategic planning at the outset can maximize long-term wealth creation, optimize tax benefits, and ensure the retirement corpus aligns with lifestyle aspirations.

- Early planning enhances compounding benefits and corpus growth

- Risk assessment guides asset allocation decisions

- Awareness of common pitfalls prevents erosion of retirement wealth

- Tailored contributions improve long-term retirement outcomes

21.1 Age & Risk Profile

Age and individual risk tolerance are central to determining the appropriate asset allocation within NPS. Younger investors can generally absorb higher equity exposure for growth, while older subscribers benefit from conservative allocations to protect accumulated capital.

- Younger investors have longer horizons to recover from market volatility

- Risk appetite influences the proportion of equity vs debt in portfolios

- Life-stage adjustments help balance growth and security

- Matching allocation to personal risk profile mitigates emotional investment decisions

21.2 Time Horizon

The duration until retirement affects both contribution strategy and asset allocation. Longer horizons allow for aggressive growth-oriented investments, while shorter horizons necessitate capital preservation and lower volatility to protect accumulated savings.

- Early entry maximizes the benefits of compounding over decades

- Shorter horizons require conservative strategies to safeguard the corpus

- Contribution frequency and amount should align with the retirement timeline

- Monitoring and adjusting allocations ensures alignment with evolving goals

21.3 Common Mistakes

Understanding typical errors can prevent suboptimal outcomes in NPS investing. Missteps such as inconsistent contributions, ignoring lifecycle allocation, or premature withdrawals can significantly reduce the effectiveness of this retirement vehicle.

- Inconsistent or insufficient contributions undermine corpus growth

- Ignoring equity allocation early limits long-term returns

- Premature withdrawals erode compounding benefits and future income

- Overlooking tax advantages reduces net retirement wealth

22. FAQs

The National Pension System (NPS) generates numerous questions among subscribers due to its structured long-term nature and tax implications. Understanding key aspects around contributions, returns, taxation, and account management helps investors make informed decisions and maximize retirement outcomes.

- Clarifies common doubts regarding participation and benefits

- Reinforces understanding of tax efficiency and contribution rules

- Provides guidance on practical account management and withdrawals

- Enhances confidence in long-term retirement planning

22.1 Contributions & Returns

Subscribers often seek clarity on how much to contribute and what returns to expect. Contributions can be flexible within minimum thresholds, and returns are market-linked, reflecting equity and debt allocations over time.

- Minimum annual contribution ensures the account remains active

- Returns vary with equity and debt allocation strategies

- Long-term participation smooths volatility and improves net growth

- Regular monitoring helps optimize allocation for better outcomes

22.2 Taxation

Tax treatment is a critical consideration for NPS participants. Contributions, additional voluntary contributions, and employer contributions enjoy specific tax deductions, while withdrawals and annuities are subject to structured tax rules.

- Section 80CCD(1), 80CCD(1B), and 80CCD(2) provide layered tax benefits

- Partial withdrawals and annuity income are taxed differently

- Tax planning enhances net corpus and post-retirement income

- Awareness of tax rules prevents unexpected liabilities

22.3 Account Management

Effective account management ensures NPS accounts remain compliant, contributions are tracked, and retirement planning objectives are met. Subscribers can use digital tools to monitor investments and maintain proper documentation.

- Monitor fund performance and asset allocation regularly

- Keep contribution schedules consistent to maximize corpus growth

- Maintain records for tax and regulatory compliance

- Digital platforms like My Wealth Locker can consolidate NPS and other investments for better oversight

23. Conclusion

The National Pension System (NPS) stands out as a core retirement instrument, offering a disciplined, cost-efficient, and market-linked framework for long-term wealth creation. By integrating structured contributions, strategic asset allocation, and tax efficiency, NPS enables professionals and entrepreneurs to systematically build a retirement corpus while managing risk and ensuring financial security.

- Serves as a foundational pillar within a diversified retirement portfolio

- Long-term participation leverages compounding for substantial corpus growth

- Balances growth and security to sustain a post-retirement lifestyle

- Complements other retirement and wealth management strategies

Strategic Takeaways

Subscribers who incorporate NPS into their financial planning gain a combination of predictable retirement income, tax efficiency, and the potential for market-linked growth. This makes the system an essential tool for securing financial independence and ensuring long-term retirement readiness.

- Early and consistent contributions maximize the power of compounding

- Lifecycle-based asset allocation mitigates risk while capturing growth

- Integration with digital tools, such as My Wealth Locker, enhances portfolio management

- Understanding withdrawal rules, annuity planning, and taxation ensures optimal retirement outcomes

By positioning the National Pension System (NPS) at the center of retirement strategy, investors can achieve sustainable wealth creation, disciplined savings behavior, and the confidence that their financial future is well-protected. The system’s combination of long-term growth potential, cost efficiency, and structured payouts underscores its strategic value in achieving lasting retirement security.