Introduction

Gold occupies a distinct position in Indian households, not only as a symbol of security and cultural continuity, but also as a stabilizing asset during periods of inflation and currency volatility. As the rupee faces sustained depreciation pressures and global uncertainty drives demand for safe-haven assets, investors are reassessing how they hold gold in their portfolios. This shift has brought the discussion of digital gold vs physical gold into mainstream financial decision-making, especially among urban professionals and younger investors seeking transparency and ease of ownership.

At the same time, digitization has widened the menu of gold investment options. Traditional physical gold remains deeply rooted in emotional value and long-term wealth preservation, but digital alternatives have gained traction for their convenience and frictionless buying experience. Sovereign Gold Bonds (SGBs) add a third dimension by offering financial exposure without the burdens of storage or resale, although they come with their own liquidity considerations. As investors evaluate digital gold vs physical gold in 2026, the question is no longer about tradition versus technology-it is about cost efficiency, safety, taxation, and long-term financial outcomes.

This guide provides a structured view of how to navigate the evolving landscape of digital gold vs physical gold, along with the strategic role of SGBs. Readers will learn:

- Key factors influencing gold investment decisions in 2026

- Risks and advantages of various gold formats

- Tax and liquidity considerations relevant to Indian investors

- How to select the right gold option based on investment horizon and financial goals

This foundation will help investors make informed, data-backed choices suited to the economic realities of 2026.

Understanding Physical Gold

For most Indian households, physical gold remains the default choice for wealth storage, gifting, and long-term financial security. Within the broader digital gold vs physical gold conversation, it continues to offer emotional reassurance and a tangible sense of ownership that many investors value. However, buying and holding gold in its physical form involves several cost layers and practical constraints that have become more visible as investors compare traditional and digital channels.

Physical gold is typically purchased as jewellery, coins, or bars. Jewellery remains the most common format, but it also carries the highest non-recoverable costs. Making charges range between 8–25 percent, wastage deductions occur during crafting, and purity verification often requires independent testing. Coins and bars offer comparatively better value, but investors must still evaluate hallmarking, storage risks, and resale flexibility. These operational frictions are central to the evolving digital gold vs physical gold debate for 2026.

When evaluating cost efficiency, investors should consider the full acquisition and holding lifecycle:

- GST: A flat 3 percent GST on purchase, payable upfront.

- Making charges: Add-on costs for jewellery that are not recoverable during resale.

- Wastage: Reduces the net weight value of jewellery when selling.

- Purity risk: Non-hallmarked gold may trade at lower buyback rates.

- Insurance and storage: Bank lockers cost between ₹3,000–₹12,000 annually, depending on city and size.

- Resale deductions: Jewellers typically deduct 2-7 percent, and resale policies differ widely.

Liquidity is another key factor. Selling physical gold usually involves delays for purity testing, price negotiation, and document verification. While it remains one of the most widely accepted collateral forms in India, cash conversion is not always immediate. These liquidity gaps stand out sharply when investors evaluate digital gold vs physical gold choices, especially for emergency planning.

From a taxation standpoint, physical gold attracts capital gains tax when sold after three years, with indexation benefits available under long-term capital gains. Short-term gains are added to taxable income. Documentation quality-bills, weight details, and purity-plays a crucial role in accurate tax reporting, reinforcing the importance of organized record-keeping.

Overall, physical gold retains its relevance but requires disciplined cost assessment, proper storage, and careful exit planning. As investors weigh digital gold vs physical gold, understanding these operational realities is essential for making informed decisions in 2026.

Understanding Digital Gold

Digital gold has become a widely adopted entry point for Indian investors, driven by app-based investing, low minimum ticket sizes, and 24×7 convenience. In the broader digital gold vs physical gold framework, it offers simplicity and accessibility, especially for millennials and first-time investors. However, despite its frictionless user experience, digital gold carries structural risks, cost layers, and regulatory gaps that investors must understand before relying on it as a long-term wealth asset.

Most digital gold platforms partner with private vaulting companies and bullion suppliers. While the buying interface appears seamless, investors pay a spread-the difference between buy and sell prices-which can range from 2-6 percent. Additionally, platforms may levy storage charges, delivery fees for physical conversion, and ancillary convenience fees. These costs, although subtle, create meaningful differences when comparing digital gold vs physical gold from a total ownership perspective in 2026.

Key operational risks include:

- Ownership structure: Investors hold gold in the name of the platform’s vaulting partner, not directly in their own name.

- Delivery risk: Converting digital units into physical coins or bars may involve delays, limited availability, or additional charges.

- Regulatory uncertainty: Digital gold is not governed by SEBI, RBI, or any dedicated gold-market regulation, creating counterparty and continuity risk.

- Platform dependency: If the platform discontinues services, investors may face forced redemption or migration to another provider.

Liquidity is often marketed as “instant,” but this is only partially true. While apps allow immediate sell orders, the actual settlement may take time, and prices fluctuate quickly during volatile market periods. These realities highlight the practical differences in the digital gold vs physical gold comparison, especially for investors seeking reliable liquidity during emergencies.

Taxation also requires careful attention. Gains from selling digital gold are taxed as capital gains, similar to physical gold. Short-term gains are added to taxable income, and long-term gains (after three years) are subject to indexation benefits. However, documentation can be inconsistent across platforms, and consolidated statements are not always readily accessible-creating challenges during audits or tax filing.

Despite these limitations, digital gold remains a useful option for disciplined micro-investing and short-term accumulation. But within the digital gold vs physical gold decision-making process, investors must account for regulatory gaps, platform dependency, spreading costs, and documentation quality before allocating a meaningful share of their portfolio to digital gold in 2026.

Understanding Sovereign Gold Bonds (SGBs)

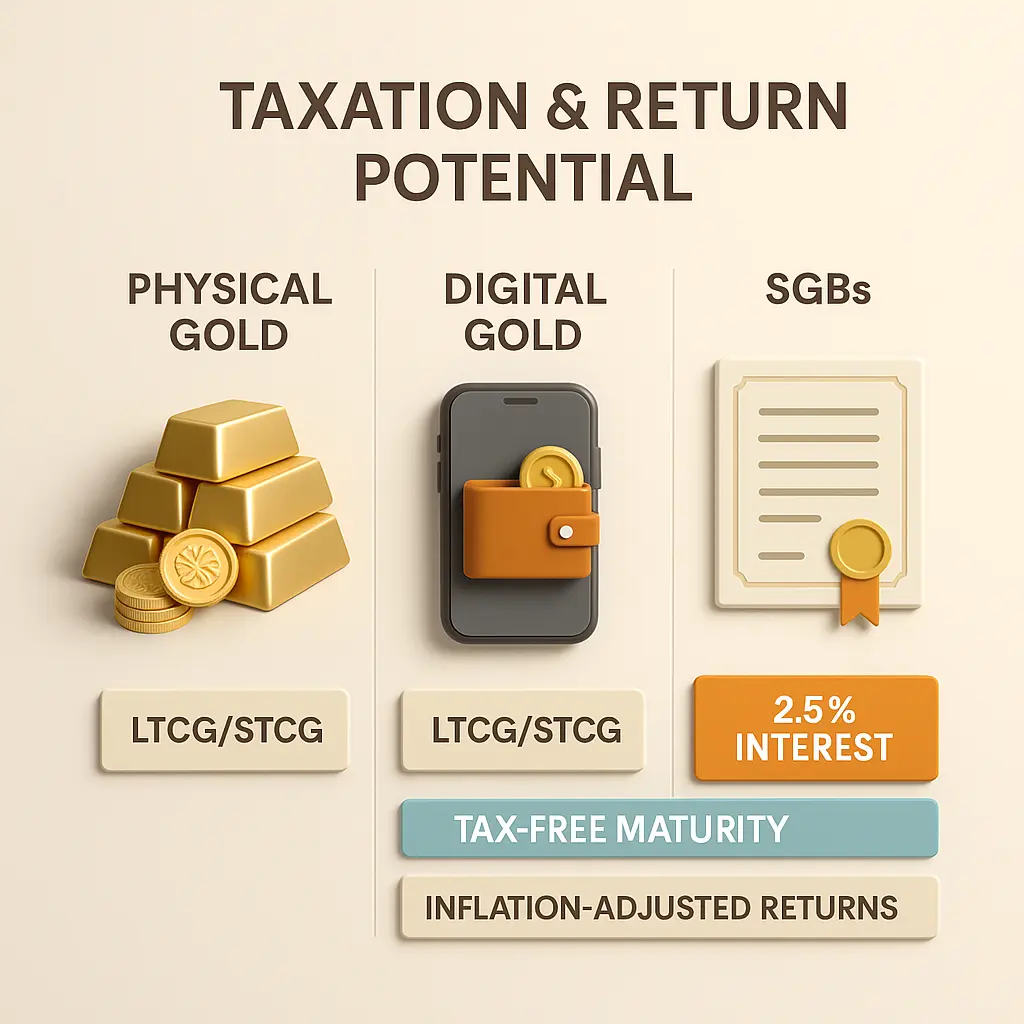

Sovereign Gold Bonds (SGBs) continue to stand apart as a unique instrument within the broader digital gold vs physical gold and SGB decision-making framework. Backed by the Government of India, SGBs provide exposure to gold prices without the operational burdens of storage, purity assessment, or resale negotiations. The 2.5% annual interest paid on the initial investment-over and above gold price appreciation-remains a compelling differentiator for long-term investors seeking predictable, low-risk returns.

SGB prices are directly linked to the domestic gold rate, offering the financial benefits of holding gold without physical possession. However, liquidity remains a key limitation. Although SGBs are listed on stock exchanges, secondary market liquidity is inconsistent, and many bonds trade at discounts to their fair value due to limited demand. Investors can exit prematurely only after the fifth year through designated RBI windows, which may not align with immediate cash-flow requirements. These constraints play a central role when evaluating SGBs alongside digital gold vs physical gold in 2026.

Key advantages of SGBs include:

- 2.5% assured interest credited semi-annually.

- Government-backed safety, with no purity or storage concerns.

- Tax-free maturity, as capital gains are fully exempt after eight years.

- Indexation benefits available on premature redemption after five years.

Key disadvantages of SGBs include:

- Liquidity gaps, especially in the secondary market.

- Potential discount pricing when selling before maturity.

- Long lock-in, limiting flexibility during emergencies.

- Unsuitability for short-term investors or those prioritizing immediate liquidity.

Overall, SGBs are well-suited for long-term, conservative investors who aim to accumulate gold in a structured, tax-efficient manner. However, individuals requiring flexibility, rapid liquidity, or transactional convenience may find SGBs less suitable when balancing them against digital gold vs physical gold and other gold investment routes available.

Side-by-Side Analytical Comparison of Gold Investment Options

Evaluating digital gold vs physical gold alongside Sovereign Gold Bonds requires a structured view of safety, cost, taxation, and long-term return potential. Each format carries distinct operational characteristics that influence both risk and wealth outcomes. Indian investors increasingly demand clarity on ownership protections, liquidity reliability, and inflation-adjusted returns-key variables that meaningfully differentiate one format from another.

Below is a consolidated comparison to help investors assess practical suitability:

| Evaluation Category | Physical Gold | Digital Gold | Sovereign Gold Bonds (SGBs) |

|---|---|---|---|

| Safety & Ownership | Tangible asset but exposed to theft, loss, purity risk, and storage dependency | Held via platform-vault partners; counterparty and regulatory risk present | Government-backed; no purity or storage concerns |

| Liquidity | Widely accepted but resale involves deductions, purity checks, and delays | App-based selling; spreads apply; settlement not always instant | Limited liquidity; exchange prices may trade at discounts; premature exit allowed only from year 5 |

| Cost Structure | GST, making charges, wastage, locker costs | Spread, storage charges, delivery fees | No storage cost; no GST on purchase; nominal issuance charges |

| Taxation | LTCG after 3 years with indexation; STCG taxed as income | Same as physical gold; documentation varies by platform | Tax-free maturity after 8 years; indexation on early exit |

| Inflation-Adjusted Returns | Moderate; costs eat into long-term gains | Moderate; spreads reduce compounding | Highest potential due to 2.5% interest + tax-free capital gains |

| Ownership Transparency | High but depends on documentation quality | Medium; dependent on platform records | High; reflected in demat or certificate form |

This comparison shows how the digital gold vs physical gold assessment becomes more nuanced when SGBs are included. Physical gold offers emotional assurance and widespread acceptance but carries significant frictional costs and storage risks. Digital gold provides convenience yet introduces platform dependency and regulatory uncertainty, which matter in the digital gold vs physical gold debate for risk-aware investors.

SGBs deliver superior inflation-adjusted returns due to tax-free maturity and interest income, but their liquidity constraints make them unsuitable for short-term needs. Ultimately, evaluating digital gold vs physical gold, with SGBs as the third variable, requires investors to balance convenience, long-term returns, and exit flexibility. A structured, goal-based approach yields the most efficient allocation across formats in 2026.

Suitability by Investment Horizon and Risk Profile

Investment horizon plays a decisive role in choosing between physical gold, digital gold, and SGBs. Within the broader digital gold vs physical gold framework, short-term liquidity needs contrast sharply with the long-term tax efficiency offered by financial gold instruments. Effective allocation requires aligning holding periods with risk appetite and expected cash-flow requirements.

Short-Term (0-2 Years): For Liquidity-Focused and Conservative Investors

Physical gold and digital gold are more practical for short horizons, given their accessibility and widespread acceptance. Physical gold works for individuals who value tangibility and may use it as collateral. Digital gold suits investors who prefer app-based convenience and incremental saving, though spreads and platform risk must be considered.

- Best fit: Conservative and liquidity-sensitive investors

- Avoid: SGBs due to lock-in and poor secondary market liquidity

Medium-Term (3–5 Years): For Balanced Investors Seeking Flexibility

Digital gold allows systematic accumulation without storage costs, while physical coins or bars help investors maintain direct ownership. A blended approach is often appropriate for balanced investors who want optionality but are not ready for long-term locking.

- Best fit: Balanced investors combining flexibility with moderate return expectations

- Consider cautiously: SGBs only if willing to hold until the fifth-year exit window

Long-Term (5-10+ Years): For Growth-Oriented and Tax-Efficient Strategies

SGBs stand out for extended horizons due to interest income and tax-free maturity. Their inflation-adjusted return profile is significantly stronger, making them a preferred choice for disciplined long-term investors. Physical gold and digital gold remain supplementary holdings for diversification but may underperform after accounting for costs-an important distinction when comparing digital gold vs physical gold over longer periods.

- Best fit: Conservative long-term savers and growth-focused investors aiming for tax efficiency

- Supplement with: Limited physical or digital holdings for tactical liquidity

By mapping goals, horizon, and risk appetite, investors can make more structured decisions within the digital gold vs physical gold landscape while integrating SGBs strategically for long-term growth.

Real-World Use Cases for Indian Investors

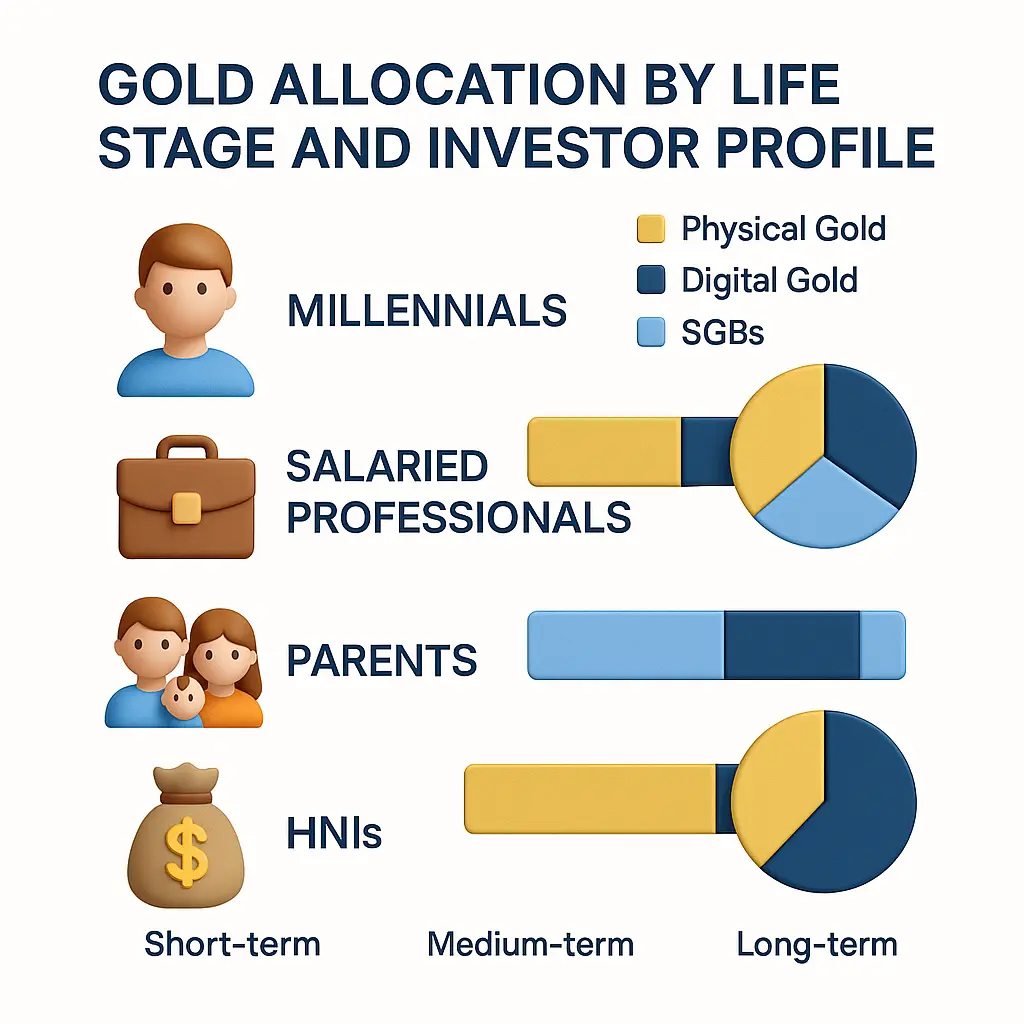

Investor behaviour varies widely across life stages, income levels, and financial goals. When evaluating digital gold vs physical gold, decisions must reflect liquidity needs, tax considerations, and long-term wealth priorities. Different Indian investor groups approach gold with distinct expectations, making personalized decision logic essential.

Salaried Professionals Seeking Convenience and Diversification

Working professionals often prioritise liquidity, predictable documentation, and seamless investing. Digital gold enables small, periodic investments without storage responsibilities, while SGBs offer a disciplined long-term route for wealth building.

- Use digital gold for short-term saving goals or staggered accumulation

- Allocate to SGBs for tax-efficient long-term exposure

- Keep minimal physical gold unless required for collateral or family use

Parents Saving for Children’s Education or Marriage

Parents often balance cultural needs with financial discipline. Physical gold remains relevant for future jewellery requirements, but its costs are substantial.

- Use SGBs for long-term financial gold accumulation with tax-free maturity

- Maintain a limited physical gold allocation for cultural commitments

- Avoid heavy reliance on digital gold due to regulatory gaps

Millennials Prioritizing Flexibility and Digital Convenience

Millennials favour transparency, app-based transactions, and low friction-key drivers in the digital gold vs physical gold choice.

- Digital gold suits short-term liquidity and micro-investing

- SGBs add structured long-term exposure

- Physical gold is kept minimal due to storage and resale friction

HNIs and Long-Term Wealth Builders

HNIs focus on risk control, tax optimisation, and portfolio allocation strategy.

- SGBs offer strong long-term compounding with tax-free returns

- Physical gold serves diversification and estate planning needs

- Digital gold is used sparingly due to counterparty and regulatory risk

Across all profiles, balancing convenience, liquidity, and long-term efficiency is critical. A structured approach helps investors integrate financial gold with clarity, aligning decisions naturally within the evolving digital gold vs physical gold framework.

The Role of Documentation and Portfolio Visibility in Gold Investing

Strong documentation and organised record-keeping have become critical in the digital gold vs physical gold ecosystem. As gold ownership shifts across formats-app-based holdings, paper certificates, and physical assets-investors face growing challenges related to taxation, compliance, inheritance, and long-term wealth visibility. Without structured documentation, investors risk valuation disputes, delayed liquidity, and tax penalties.

Physical gold requires clear invoices specifying weight, purity, and hallmarking details. Digital gold platforms issue online statements that may vary in format or accessibility, while SGBs generate certificates, demat entries, or e-receipts that must be preserved for maturity and taxation purposes. These diverse documentation trails make it essential to track all holdings in one organised system.

Key reasons why documentation matters across gold formats include:

- Invoice storage: Prevents resale disputes and ensures accurate purity verification.

- Purchase tracking: Helps determine cost of acquisition, capital gains, and indexation benefits.

- SGB maturity tracking: Prevents missed redemption windows and ensures timely tax-free exit.

- Taxation proof: Essential during audits, scrutiny, or high-value financial transactions.

- Inheritance clarity: Simplifies wealth transfer and avoids disputes or loss of unrecorded assets.

A structured documentation approach becomes even more important when comparing digital gold vs physical gold, as the risk of misplaced receipts or inaccessible platform records can disrupt both liquidity and tax filing. A neutral personal wealth documentation and tracking solution such as My Wealth Locker can help consolidate invoices, track SGB maturity dates, and maintain updated records without influencing investment decisions.

Ultimately, disciplined documentation strengthens the integrity of gold holdings across formats. Whether an investor holds physical jewellery, app-based units, or long-term bonds, portfolio visibility provides confidence, reduces compliance risk, and ensures that long-term wealth objectives are met-an increasingly critical factor in the modern digital gold vs physical gold landscape.

Common Mistakes Indian Investors Make While Buying Gold

Many investors approach gold with confidence but overlook critical details that directly affect returns, liquidity, and long-term wealth outcomes. Within the digital gold vs physical gold framework, these mistakes often stem from assumptions about purity, convenience, and resale value. Recognizing these pitfalls can help investors make more informed and financially sound decisions.

A frequent mistake is ignoring BIS hallmarking and purity verification. Non-hallmarked jewellery or coins may be sold at a discount, and purity disputes during resale can lead to lower valuations. Similarly, investors often overpay making charges and wastage, assuming jewellery automatically qualifies as an investment asset. These charges are largely non-recoverable and can erode long-term returns, especially when selling during urgent cash requirements.

Digital investors commonly underestimate platform and regulatory risk. Trusting unregulated apps without evaluating custody partners, documentation practices, or platform solvency is a major vulnerability in the evolving digital gold vs physical gold landscape. This creates counterparty risk, inconsistent record-keeping, and complications during redemption or conversion to physical form.

Investors also misinterpret SGB liquidity rules. Many assume they can redeem Sovereign Gold Bonds at any time, only to discover that premature exit is allowed only from the fifth year and that the secondary market often trades at a discount. This misunderstanding can disrupt financial planning or emergency liquidity needs.

Poor documentation is another widespread issue. Missing invoices, unclear purchase history, or scattered digital records lead to:

- Lower resale value due to unverifiable purity

- Difficulty calculating capital gains for tax filing

- Disputes during inheritance or asset transfer

- Delays in redeeming SGBs or claiming tax-free maturity benefits

Ultimately, avoiding these errors is essential for maximizing value, safeguarding ownership, and achieving clarity across all gold formats. Awareness of these consequences sharpens decision-making within the modern digital gold vs physical gold comparison and helps investors protect long-term wealth.

Macro Forces Shaping Gold Prices in India

Timing gold purchases requires understanding the broader forces driving domestic prices. In the digital gold vs physical gold decision, shifts in currency value, inflation expectations, and global monetary policy play a central role. Gold in India is priced in rupees but influenced heavily by global markets, making it sensitive to macroeconomic volatility and international risk sentiment.

A weaker USD-INR usually raises domestic gold prices. When the rupee depreciates against the dollar, import costs rise, directly pushing gold rates higher regardless of global price movements. For investors, this currency-driven effect amplifies long-term hedging value but increases the risk of mistimed lump-sum purchases. Inflation is another structural driver. As real purchasing power declines, gold acts as a store of value, attracting flows from both retail investors and institutions.

Global interest rates-especially U.S. Federal Reserve policy-shape gold demand by influencing opportunity cost. When rates fall or appear likely to fall, gold becomes more attractive relative to fixed-income assets. Geopolitical tensions and central bank accumulation further strengthen demand, often triggering sharp price spikes.

Key macro triggers to monitor include:

- Rupee depreciation increasing local gold premiums

- Global inflation trends affecting long-term demand

- Federal Reserve rate decisions impacting international flows

- Geopolitical risk events driving safe-haven buying

- Central bank purchases tightening global supply

These factors make timing strategies crucial in the digital gold vs physical gold framework. Lump-sum buying may suit investors who expect sustained inflation or prolonged rupee weakness. However, staggered purchases-weekly or monthly-help reduce timing risk and smooth out price volatility during uncertain macro cycles. This disciplined approach is particularly relevant in 2026, where global and domestic variables remain highly interconnected.

By combining macro awareness with structured buying, investors improve cost efficiency and reduce emotional decision-making within the modern digital gold vs physical gold timing environment.

Operational Considerations for Long-Term Gold Management

Effective gold planning extends beyond purchasing decisions. In the digital gold vs physical gold framework, emergency liquidity, nominee clarity, and long-term record maintenance play a direct role in how efficiently investors can access, transfer, or account for their holdings. Operational readiness reduces risk, prevents delays during critical moments, and strengthens financial control.

Emergency liquidity planning is essential because the speed of conversion varies across formats. Physical gold may require purity checks and negotiation, while digital platforms may impose spreads or settlement delays during volatile markets. SGBs carry the longest liquidity constraints, with premature exit allowed only from the fifth year. Investors should maintain clear visibility on which part of their gold allocation can be liquidated quickly and which requires advance planning.

Nominee clarity and estate transfer are equally important. Fragmented records-jewellery without invoices, digital units scattered across apps, or SGBs without updated nominations-can create disputes or result in unclaimed assets. Ensuring structured documentation protects beneficiaries and enables smooth wealth transfer.

Key operational priorities include:

- Emergency liquidity mapping: Identifying accessible versus locked-in gold assets.

- Nominee and ownership clarity: Updating nominations across digital platforms and SGB holdings.

- Estate transfer planning: Maintaining documented proof for legal transfer and family disputes.

- Tax audit readiness: Preserving invoices, transaction history, and SGB statements for accurate reporting.

- Long-term record maintenance: Tracking maturity dates, purchase values, and supporting documents.

These tasks become increasingly complex as investors diversify across formats within the digital gold vs physical gold landscape. A neutral personal wealth tracking aid such as My Wealth Locker can help centralize records, reducing fragmentation without influencing investment choice.

By proactively managing documentation, liquidity, and succession planning, investors enhance the operational resilience of their gold portfolio. This structured approach ensures that gold functions not only as an asset but as a dependable, accessible component of long-term wealth management.

Profile-Based Final Verdict for Indian Investors

Choosing between formats requires aligning time horizon, liquidity needs, and documentation discipline. Within the digital gold vs physical gold framework, SGBs add a third, highly efficient long-term alternative. The optimal choice varies sharply across investor profiles, especially when balancing convenience, taxation, and wealth-transfer clarity.

For short-term investors-traders, tactical allocators, and individuals seeking 3–6 month flexibility-immediacy matters more than cost efficiency. Digital gold offers frictionless buying and selling with no storage risk. Physical coins or bars can work for those who prefer tangibility, but making charges and resale spreads reduce viability for short cycles. SGBs are unsuitable due to their lock-in period. In the digital gold vs physical gold comparison, digital formats lead this segment decisively.

For 3–5-year investors-parents planning near-term goals, first-time gold allocators, and savers building emergency buffers-the decision becomes nuanced. Digital gold offers liquidity and transparent pricing, while physical gold supports ceremonial requirements and long-term possession. However, SGBs provide index-tied price appreciation plus 2.5 percent annual interest. Liquidity constraints and secondary market variability are trade-offs but manageable for disciplined investors.

For long-term investors-HNIs, wealth creators, and families optimizing tax efficiency-SGBs dominate. Capital gains are tax-free at maturity, and coupon income boosts net returns. Physical gold remains relevant for cultural and inheritance needs, while digital gold works as a liquid satellite allocation. But in the digital gold vs physical gold and SGB hierarchy, SGBs deliver the strongest combination of security, returns, and estate transfer clarity.

Investor-specific considerations include:

- Liquidity priority: Digital gold for quick access; physical only when resale conditions are known.

- Goal-linked savings: SGBs for long-term compounding; physical for ceremonial intent.

- Risk and compliance: Digital gold only through regulated, interoperable platforms; physical purchases with BIS purity and invoices.

- Documentation readiness: A critical factor in the digital gold vs physical gold evaluation, especially for families with shared assets.

Final Ranking Summary Table

| Investor Horizon | Rank 1 | Rank 2 | Rank 3 |

|---|---|---|---|

| Short Term (0–1 year) | Digital Gold | Physical Gold | SGB |

| Medium Term (3–5 years) | SGB | Digital Gold | Physical Gold |

| Long Term (5+ years) | SGB | Physical Gold | Digital Gold |

This structured verdict helps investors match their gold format to their financial behaviour, liquidity expectations, and long-term wealth strategy.

Building a Smart, Blended Gold Strategy

Gold allocation should reflect life stage, financial goals, and risk appetite. Within the digital gold vs physical gold framework, blending physical gold, digital gold, and SGBs can optimise liquidity, cost efficiency, and long-term wealth stability. A strategic mix allows investors to balance immediate accessibility with structured, tax-efficient growth.

Early-Career and Millennials

Investors in their 20s and early 30s may prioritise convenience and small-ticket accumulation. Digital gold suits systematic, app-based investing for short-term goals, while SGBs can be gradually added for long-term tax-free growth. Physical gold holdings can remain minimal, reserved for ceremonial occasions or gifting.

- Focus: Digital gold for liquidity and micro-investing

- Supplement with: SGBs for disciplined long-term exposure

- Keep physical gold light for cultural needs

Mid-Career and Parents Saving for Family Goals

Professionals with medium-term savings horizons may combine all three formats. SGBs provide tax-free, interest-accruing long-term holdings. Physical gold meets ceremonial obligations, while digital gold ensures liquidity for emergencies or goal-linked accumulation.

- Focus: SGBs for core long-term investment

- Digital gold for flexible liquidity

- Physical gold for tangible security and family events

Pre-Retirement and HNIs

Long-term wealth preservation and estate planning dominate priorities. SGBs form the backbone of the portfolio, maximising inflation-adjusted returns. Physical gold supports diversification, tangible ownership, and inheritance clarity. Digital gold can serve as a minor allocation for tactical liquidity or micro-trading, but regulatory and counterparty risks must be assessed.

- Focus: SGBs for long-term compounding and tax efficiency

- Physical gold for diversification and estate planning

- Limited digital gold for immediate access

Maintaining portfolio visibility across these formats is crucial. Tools like My Wealth Locker allow investors to consolidate invoices, track SGB maturities, and monitor digital holdings, providing a clear picture of total gold exposure.

By blending gold types according to life stage and horizon, investors can achieve an optimal balance of liquidity, stability, and long-term growth within the digital gold vs physical gold ecosystem, ensuring both financial and operational efficiency.

Conclusion

The gold investment landscape demands a nuanced understanding of cost, liquidity, taxation, and risk. Across the digital gold vs physical gold spectrum, each format offers distinct advantages physical gold provides tangibility and cultural relevance, digital gold delivers convenience and micro-investing flexibility, and Sovereign Gold Bonds (SGBs) offer government-backed security with tax-free maturity and 2.5% interest. Data from recent market trends indicate that investors who blend these options according to horizon and life stage achieve the most consistent inflation-adjusted returns while maintaining liquidity for emergencies.

Decision clarity emerges when personal goals are aligned with the inherent characteristics of each format. Short-term liquidity favors digital gold, medium-term goals benefit from a mix of physical and digital holdings, and long-term wealth preservation is best served by SGBs supplemented with physical gold. Proper documentation, nominee updates, and portfolio tracking-tools like My Wealth Locker-ensure operational efficiency and reduce compliance risk.

Ultimately, a disciplined, goal-oriented approach allows investors to balance risk, maximize tax efficiency, and safeguard wealth. Understanding the comparative strengths and limitations within the digital gold vs physical gold framework equips Indian investors to make informed, confident decisions in 2026.