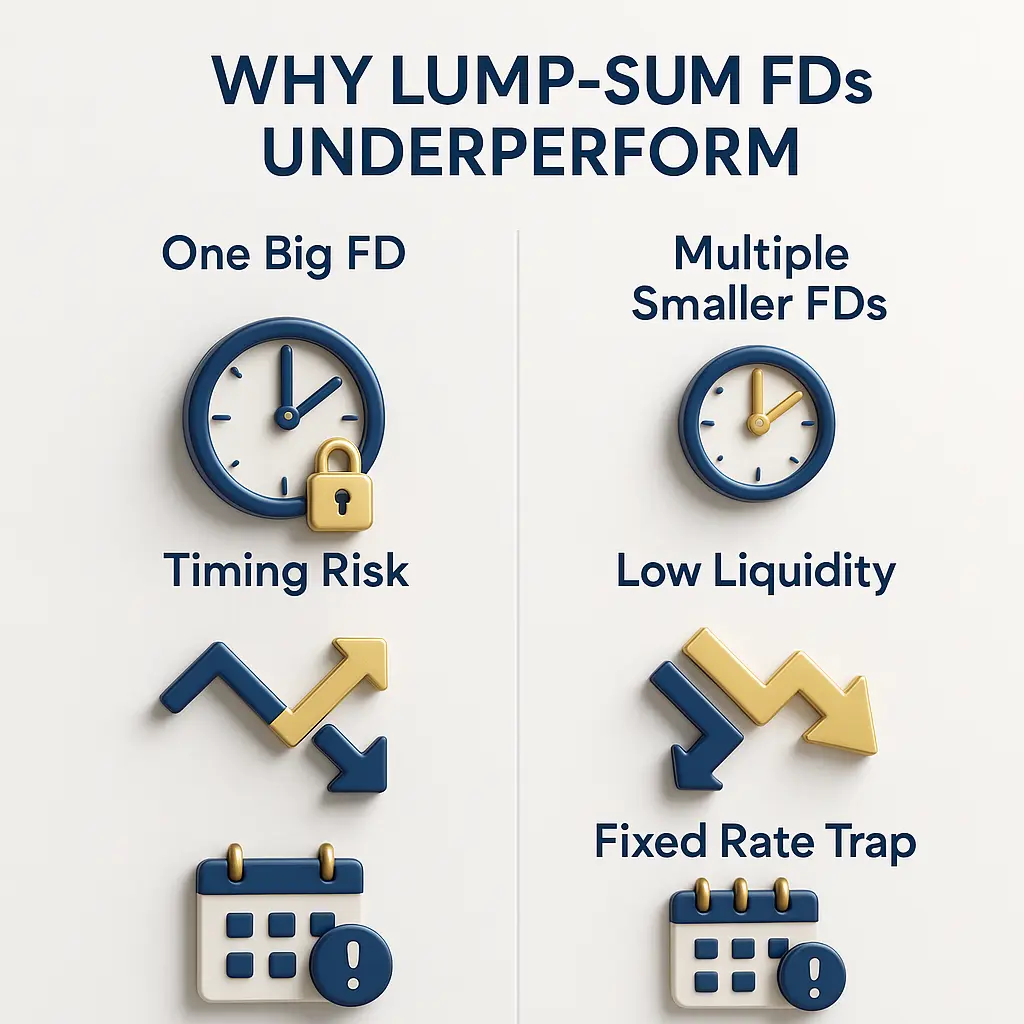

1. The FD Return Problem Most Indian Families Don’t See Coming

Most Indian households continue to rely on lump-sum fixed deposits as their safest and most predictable savings option. But in reality, traditional FDs rarely deliver the effective returns people expect. Understanding this gap is the foundation for answering the bigger question many savers ask: how to get better returns from FD without taking on additional risk.

The first issue is the behaviour of interest rate cycles. FD rates in India move in multi-year waves. When rates are low-like the 5-6% window seen during 2020–2022-locking your entire corpus into a single long-tenure FD caps your return for years. When rates rise later, you miss the opportunity to benefit. This is the core of FD reinvestment risk: your money may be stuck earning outdated rates while the market improves.

Lock-ins make this worse. Breaking an FD results in penalties and interest loss, so most savers simply hold on to low-rate deposits until maturity. A single timing mistake can suppress returns for 3–5 years.

Inflation adds another layer of erosion. Even today, with many banks offering 6.5–7.5% for standard tenures, average Indian inflation trends between 5–6%. For retirees in the higher tax brackets, post-tax returns often fall to 4.5–5.5%, which means real returns hover close to zero. For a salaried household earning 7% on a ₹5 lakh FD at 20% tax, the effective return drops to roughly 5.6%. With inflation at 6%, purchasing power actually declines. This illustrates the long-term inflation impact that most savers underestimate.

Because of these structural issues, families commonly make avoidable mistakes that further reduce returns:

- Locking all savings into a single FD tenure.

- Missing renewal dates and allowing funds to auto-renew at lower default rates.

- Holding multiple FDs across banks without tracking maturity schedules.

- Reinvesting during a low-rate phase simply because liquidity was not planned in advance.

Addressing these issues is the first step toward strategically improving outcomes and understanding how to get better returns from FD in real-world Indian conditions. A structured approach helps households avoid timing errors, reduce risk, and protect purchasing power while answering the core question: how to get better returns from FD consistently over time.

2. What Is FD Laddering and Why It Delivers Higher Effective Returns

FD laddering in India is a simple, practical strategy where you divide one large FD into several smaller FDs with different maturities-for example 1, 2, 3, 4, and 5 years. Instead of locking your entire amount at one interest rate, you create staggered maturity points that allow parts of your money to renew at potentially higher future rates. This approach directly answers the question many savers ask: how to get better returns from FD without increasing risk.

The strength of FD laddering lies in timing advantage. RBI data shows clear interest rate cycles: periods like 2013–2015 and 2022–2023 saw rates rise sharply, while 2017–2020 saw prolonged declines. When all your money is locked in a single long-term FD, you either get stuck with a low rate during rising cycles or miss protection during falling cycles. Laddering smooths out this risk by ensuring that some portion of your money matures every year. When rates rise, part of your FD renews at the new, higher rate. When rates fall, the longer-tenure FDs keep earning the older, higher rates. This helps reduce FD reinvestment risk significantly.

Laddering also improves liquidity. Most Indian families need money for annual expenses such as school fees, insurance premiums, or emergencies. Having yearly maturity points provides predictable access to funds without breaking long-term deposits. Crucially, this added flexibility does not reduce safety-you are still using the same banks, the same DICGC protection limits, and the same underlying FD product.

Below is a simple comparison that shows why FD laddering in India works better for long-term savers:

| Strategy | Lump-sum FD | Laddered FD |

|---|---|---|

| Exposure to interest rate cycles | High | Balanced across years |

| Reinvestment risk | Concentrated | Reduced through staggered renewals |

| Liquidity availability | Low | Annual or semi-annual |

| Safety | Same | Same |

| Ability to capture rising rates | Weak | Strong |

By stabilising returns, improving liquidity, and aligning maturities with real-life cash flow needs, laddering provides a structured answer to how to get better returns from FD. It ensures long-term consistency and helps savers understand how to get better returns from FD even in unpredictable rate environments.

3. When FD Laddering Works Best for Indian Investors

FD laddering is often the best FD strategy for Indian Investors households because it aligns naturally with the way Indian families earn, save, and plan their finances. It provides predictable liquidity, protects returns during uncertain interest rate cycles, and reduces the mistakes that come from managing scattered FDs across banks. Understanding where it fits best also helps answer a key question for many savers: how to get better returns from FD while keeping risk near zero.

Salaried Professionals: Managing Bonuses, Idle Funds, and Emergency Buffers

For working individuals, income arrives in uneven bursts-monthly salary, annual bonuses, incentives, and tax refunds. FD laddering helps convert these irregular inflows into a structured savings system.

How it helps salaried earners:

- Deposit annual bonuses into a 3-5 year ladder instead of a single FD to capture future rate increases.

- Convert idle bank balance into short-term rungs (6-12 months) to avoid cash drag.

- Maintain an emergency buffer with staggered maturities so funds are available yearly without breaking FDs.

- Renew maturing FDs during favourable interest rate windows, improving long-term outcomes.

This ensures professionals stay liquid when needed while still improving yield-one of the most practical answers to how to get better returns from FD for salaried households.

Retirees: Stable Income With Inflation Protection

Retirees depend on predictable cash flow. FD laddering creates a reliable income stream while reducing reinvestment timing mistakes.

Benefits for retirees:

- Annual maturities provide a steady withdrawal option without eating into principal.

- Longer rungs lock in higher rates during peak cycles, offering partial inflation protection.

- Reduces the risk of reinvesting an entire corpus at low rates during market downturns.

- Helps manage 5-10 year financial visibility without compromising safety.

This balances stability with rising cost-of-living needs-critical when thinking about how to get better returns from FD post-retirement.

Families: Education, Housing, and Multi-Account FD Planning

Indian families often manage multiple goals and multiple FDs across spouses, parents, and children. Laddering brings structure to this complexity.

Family-specific advantages:

- Aligns FD maturities with school fees, higher education milestones, or down payment timelines.

- Helps avoid liquidity crunches during big expenses.

- Prevents mismanagement across multiple accounts by spacing out maturity points.

FD laddering brings order, timing advantage, and flexibility-exactly what middle-class families need to plan confidently.

4. How to Build an Optimal FD Laddering Structure in India

Creating a well-designed ladder is a practical way for households to improve returns, maintain liquidity, and reduce reinvestment mistakes. A systematic approach helps answer the recurring question: how to get better returns from FD in a way that works reliably through different interest rate cycles. Below is a clear, step-by-step framework tailored for Indian investors.

Step 1: Segment Your FD Corpus Across 1–5 Year Tenures

Instead of putting your entire amount into one FD, divide it across staggered maturities:

- 20–25% in 1-year FD

- 20–25% in 2-year FD

- 20–25% in 3-year FD

- 20–25% in 4-year FD

- 20–25% in 5-year FD

This structure ensures that a part of your capital matures every year, giving you timing flexibility during rising and falling rate cycles. It is a foundational tactic for how to get better returns from FD without taking additional risk.

Step 2: Choose the Right Type of Institution (Bank vs SFB vs Corporate FD)

Each category offers a different balance of return and safety:

- Large Banks: Highest safety, moderate returns. Ideal for conservative rungs like 4-5 years.

- Small Finance Banks (SFBs): Higher interest rates, slightly higher perceived risk. Suitable for 1-2 year rungs where liquidity is quicker.

- Corporate FDs: Highest rates but require careful credit rating evaluation. Limit exposure to a small portion of the ladder.

Allocating across categories helps improve yield while respecting risk boundaries.

Step 3: Align FD Maturities With Annual Cash Flow Needs

Plan maturities around predictable expenses:

- School/college fees

- Insurance premiums

- Home renovation or EMI buffer

- Medical and emergency needs

This reduces the need to break FDs, preserving returns over time-critical for investors thinking about how to get better returns from FD sustainably.

Step 4: Set Clear Auto-Renewal and Reinvestment Rules

To avoid losing out on rate opportunities:

- Enable auto-renewal only for rungs aligned with future cash flow requirements.

- Disable auto-renewal for rungs you want to reassess each year.

- Review rates at maturity and shift rungs to better tenures when cycles change.

- Use a reminder tool like My Wealth Locker to avoid missing renewal windows.

A disciplined renewal strategy ensures the ladder stays efficient and continuously aligned with market conditions.

5. Three Proven Laddering Models for Indian Investors

Different households have different liquidity needs, risk preferences, and income patterns. The following three laddering models show how investors can structure their deposits while staying aligned with their financial goals. Each model answers the common question of how to get better returns from FD by balancing stability, timing advantage, and long-term consistency.

Comparison of Laddering Models

| Model | Liquidity | Safety | Return Potential |

|---|---|---|---|

| Conservative Ladder | High (annual or semi-annual) | Very High | Moderate |

| Moderate Ladder | Balanced (annual) | High | Higher |

| Aggressive Ladder | Low–Moderate | Medium–High | Highest (rate-cycle capture) |

Conservative Ladder: Designed for Retirees and Low-Risk Households

The conservative ladder focuses primarily on stability and predictable access to funds. It places more capital in shorter tenures (1–3 years) to ensure frequent liquidity and minimal reinvestment timing stress.

Key advantages:

- Ideal for retirees requiring yearly withdrawals

- Protects capital while still offering rate flexibility

- Minimises breakage penalties and helps manage medical or emergency needs

This model works best for families who prioritise safety and steady cash flow over chasing higher yields.

Moderate Ladder: Best Fit for Salaried Professionals

The moderate ladder spreads money evenly across 1–5 year tenures, giving a strong balance of liquidity and return. It offers a systematic approach to how to get better returns from FD for households that want improved yields without compromising on accessibility.

Benefits include:

- Annual maturity points allow for rate optimisation

- Longer rungs help capture peak interest cycles

- Suitable for planning education fees, insurance premiums, and short-term goals

Aggressive Ladder: For Yield Maximisation and Rate-Cycle Advantage

This structure allocates more capital to longer tenures (3–5 years) to secure higher rates for extended periods. Shorter rungs are fewer but strategically placed to capture future rate increases.

Why it works:

- Maximises long-term returns during high-rate periods

- Reduces exposure to falling cycles

- Helps serious savers understand how to get better returns from FD with disciplined reinvestment

The aggressive model suits investors comfortable with lower liquidity in exchange for higher yield potential while still staying within safe FD frameworks.

6. How FD Laddering Improves Returns-Real Numerical Scenarios

FD laddering shows its true strength when tested across different interest-rate conditions. The following practical scenarios illustrate how households can make smarter decisions and understand how to get better returns from FD using real-world rate patterns.

Scenario A: Flat Rate Cycle (6.5% Steady Rates)

Raman invests ₹5 lakh during a period when FD rates stay constant at around 6.5% for three straight years.

- Lump-sum outcome: A single 3-year FD earns roughly ₹1.04 lakh in interest.

- Laddered outcome: Raman splits the same ₹5 lakh into five rungs. Even with flat rates, the ladder provides yearly liquidity for reallocation, lets him adjust for cash flow needs, and avoids any penalty risk.

While the total interest remains similar, the ladder increases flexibility-critical for understanding how to get better returns from FD without sacrificing safety.

Scenario B: Rising Rate Cycle (6% → 7.5% → 8%)

Neha locks ₹6 lakh into a lump-sum FD at 6% just before rates climb.

- One year later, banks offer 7.5%. Two years later, the peak touches 8%.

- A ladder would allow 20% of her deposit to renew each year at the new, higher rates.

Over three years, the ladder captures improving yields, producing 8–12% higher cumulative interest than the lump-sum strategy. This timing advantage explains how to get better returns from FD when rates rise sharply.

Scenario C: Falling Rate Cycle (7.5% → 6.5% → 5.8%)

Arun invests at the peak of a high-rate period.

- With a lump-sum FD, he locks the entire amount at the prevailing 7.5%.

- A ladder protects him even better: the 4-5 year rungs continue earning 7.5% while only a small portion reinvests each year at declining rates.

This cushions long-term returns and reduces reinvestment losses.

Scenario D: Multi-Family FD Coordination

A family with FDs spread across parents, spouse, and children often faces rate mismatches, missed renewals, and unplanned breakages.

Creating a shared 1-5 year ladder smooths cash flow for school fees, medical needs, and home planning-while also ensuring everyone understands how to get better returns from FD through coordinated maturity cycles.

Across all scenarios, laddering consistently protects returns, improves timing advantages, and reduces financial friction.

7. Risk Management: Maximising Returns Without Compromising FD Safety

A well-designed laddering strategy is effective only when supported by strong risk controls. Indian households often overlook regulatory limits, bank-level exposure, and documentation inconsistencies that can directly affect liquidity and claim settlement. Strengthening these areas is essential for anyone trying to understand how to get better returns from FD while keeping their capital fully protected.

DICGC Coverage: Use Limits Intelligently

The Deposit Insurance and Credit Guarantee Corporation (DICGC) insures deposits up to ₹5 lakh per depositor, per bank (including principal + interest). To stay within compliant safety boundaries:

- Spread deposits across multiple banks rather than concentrating large sums in one institution.

- Treat each family member as a separate insured entity, but ensure proper account titling.

- Review interest accruals annually so the total does not exceed ₹5 lakh per bank when nearing maturity.

Avoid Concentration Risk in Small Finance Banks

Small Finance Banks (SFBs) often offer higher FD rates, but households should balance return with diversification:

- Allocate only a limited percentage (e.g., 15–25%) of the ladder to SFBs.

- Prioritise well-rated banks for long-tenure rungs (3–5 years).

- Review financial health indicators periodically, especially for aggressive ladder structures.

A diversified approach safeguards long-term stability without compromising yield.

Nominee, PAN, and KYC Consistency Across All Accounts

Administrative gaps are among the most common reasons for delayed or rejected claims. Ensure the following:

- All FD accounts have updated nominee details.

- PAN is consistent across banks to prevent TDS mismatches.

- KYC is renewed promptly, especially for senior citizens or dormant accounts.

- Joint-holder instructions and survivor rights are clearly recorded.

Maintaining clean, compliant documentation strengthens the overall FD strategy and improves the reliability of outcomes, especially for families aiming to balance safety with how to get better returns from FD in a disciplined manner.

8. How to Track, Renew, and Optimise Your FD Ladder Over 5-10 Years

A ladder is not a one-time setup-it must be reviewed annually to stay aligned with interest rate cycles, liquidity needs, and market conditions. A disciplined audit process ensures your structure continues delivering value and provides a clear roadmap for anyone asking how to get better returns from FD over the long term.

Annual FD Audit Checklist

Review each FD rung once a year with a structured, compliance-focused checklist:

- Check maturity dates for the next 12–18 months and plan liquidity needs.

- Compare current bank rates with market-leading options (banks, SFBs, corporate FDs).

- Verify DICGC coverage to ensure total deposits per bank remain under ₹5 lakh.

- Assess cash flow timelines such as school fees, insurance premiums, or medical contingencies.

- Review TDS deductions and confirm PAN accuracy across all banks.

- Validate nominee and joint-holder details to avoid future claim issues.

- Identify low-yield FDs still locked at outdated rates from past cycles.

- Track auto-renewals to ensure they don’t default into lower-rate tenures.

- Consolidate scattered FDs and close dormant accounts where necessary.

- Use a reminder tool like My Wealth Locker to avoid missed maturity alerts and reinvestment delays.

Optimising Renewals During Rate Movements

Renewal timing can significantly influence long-term yield. When rates rise, it is beneficial to extend maturing rungs to 3–5 years to lock in higher returns. When rates fall, keeping renewals shorter (1–2 years) protects flexibility. This dynamic adjustment is essential for households evaluating how to get better returns from FD across unpredictable cycles.

Avoid automatic renewals when rates are changing. Instead, manually reassess each FD on the day of maturity and shift it to the tenure that best aligns with the current interest cycle.

Refinancing Low-Yield FDs Into Higher-Yield Rungs

Many investors still hold deposits opened during low-rate periods (5–6%). When breakage penalties are minimal or when maturity is near, refinancing into a fresh ladder can boost long-term returns. Redirect maturing or low-return deposits into stronger rate windows to maintain a competitive blended yieldone of the most effective ways of understanding how to get better returns from FD consistently over time.

By following this cycle of auditing, optimising, and refinancing, your FD ladder remains efficient, resilient, and aligned with your overall financial strategy.

9. Final Impact: How FD Laddering Strengthens Long-Term Financial Stability

A well-structured FD ladder delivers measurable long-term advantages for Indian households. It improves yield consistency, enhances liquidity, and ensures capital is deployed efficiently-core elements for anyone trying to understand how to get better returns from FD without taking additional risk. The impact is both strategic and practical, especially over a 5–10 year horizon.

The biggest advantage is higher effective yields. By renewing portions of the ladder at different points in the interest-rate cycle, investors naturally capture peak-rate periods while shielding themselves from downturns. This blended approach often outperforms a single lump-sum FD, which is overly exposed to timing errors. Over time, small differences in renewal rates compound into meaningful value for families.

Another major benefit is improved liquidity. Instead of locking money for long tenures, laddering ensures that a portion of capital matures every year. This reduces the need to prematurely break FDs-one of the most common sources of return leakage. Whether it’s school fees, medical expenses, or home repairs, households gain predictable access to funds without disrupting their financial structure.

FD laddering also combats idle capital, a frequent issue in Indian families where savings often sit in low-yield accounts for months. Shorter rungs allow savers to quickly deploy surplus cash into productive FDs, improving overall capital efficiency. This is a simple but powerful way to think about how to get better returns from FD in daily financial behaviour.

Finally, the ladder instils reinvestment discipline. Renewals become periodic, planned decisions rather than rushed actions at random times. Families are less likely to miss maturity dates, fall into auto-renewal traps, or reinvest during weak rate cycles. This structured approach creates long-term financial stability and reinforces smart decision-making-an essential part of how to get better returns from FD with consistency and control.

10. Conclusion

FD laddering stands out as one of the few strategies that can improve returns without increasing risk, complexity, or administrative burden. By structuring deposits across staggered maturities, families gain the dual advantage of flexibility and yield optimisation-an essential combination for anyone evaluating how to get better returns from FD in a stable, predictable manner. What makes laddering uniquely powerful is that it does not rely on forecasting interest-rate movements; it simply positions the investor to benefit from both rising and falling cycles through disciplined renewal timing.

Over a multi-year horizon, this approach transforms FDs from a passive savings tool into a more strategic asset. Investors who adopt laddering reduce reinvestment mistakes, avoid premature withdrawals, and ensure every rupee is deployed at the most appropriate tenure. This structured behaviour directly addresses the practical challenges Indian households face-cash-flow uncertainty, missed maturities, and underperforming long-tenure deposits. It also strengthens long-term financial control, which is often missing in traditional one-time FD setups.

The result is a more resilient and efficient savings system. Capital remains safe, liquidity becomes predictable, and returns improve naturally through better timing. For families, retirees, and salaried professionals, laddering provides a sustainable, compliance-friendly path to enhanced outcomes. It is not just a tactic-it is a disciplined framework that answers how to get better returns from FD without compromising security.

Adopting this strategy reinforces financial discipline, reduces avoidable losses, and builds a stable foundation for long-term wealth planning. In a landscape where interest rates fluctuate and household needs evolve, FD laddering is the most reliable and structured answer to how to get better returns from FD year after year.