1. Introduction: The Silent Crisis of Lost Investments in India

India’s wealth landscape is expanding faster than most households can organise it. While digital finance is growing, the average investor still manages a mix of bank deposits, insurance plans, post office schemes, mutual funds, real estate, and gold-often scattered across institutions, family members, and documents. This fragmentation has created a silent but widespread problem: lost investments in India.

RBI and IRDAI data shows the scale of this challenge. Over ₹42,000 crore lies unclaimed across banks and insurance companies, and this number continues to rise every year. This is not just a statistic-it represents financial opportunities eroded due to poor visibility, misplaced documents, lost investments in India, and ineffective tracking systems.

The reality is simple: even financially aware Indians struggle to track investments in India consistently. And when visibility declines, wealth leakage begins.

1.1 The Scale of the Problem: Why Tracking Wealth Is Harder Than It Looks

Most investors underestimate how easy it is to lose track of financial assets. In India, the challenge is amplified by structural and behavioural factors:

- Multiple asset classes and formats-FDs, NSCs, gold, ULIPs, mutual funds, real estate records.

- High dependence on paper documents, especially for legacy products and property.

- Family-driven investment patterns, where decisions are scattered across individuals.

- Siloed financial systems, with limited interoperability across banks, insurers, and government portals.

As portfolios grow, so does the complexity. Even well-organised individuals eventually face issues of duplicated accounts, forgotten maturity dates, misplaced certificates, or lost investments in India known only to one family member.

This is why lost investments in India are not just a problem of negligence-they are a by-product of an ecosystem that lacks a unified investment tracking system.

1.2 What This Article Solves: Visibility, Control, and Financial Decision Confidence

This article breaks down the real reasons Indians lose track of their wealth and provides a structured roadmap to regain control. It is designed for beginners and financially aware readers who want actionable clarity, not generic advice.

You will learn how to:

- Improve financial visibility across all asset classes.

- Reduce the risk of misplaced documents, forgotten maturities, and unclaimed assets.

- Build a practical, easy-to-maintain investment tracking system for your family.

- Increase ROI by eliminating avoidable leakages and inefficiencies.

- Make faster, more confident financial decisions with complete data in one place.

By the end, you will understand not only why lost investments in India happen-but also exactly how to prevent them with a systematic, future-ready approach.

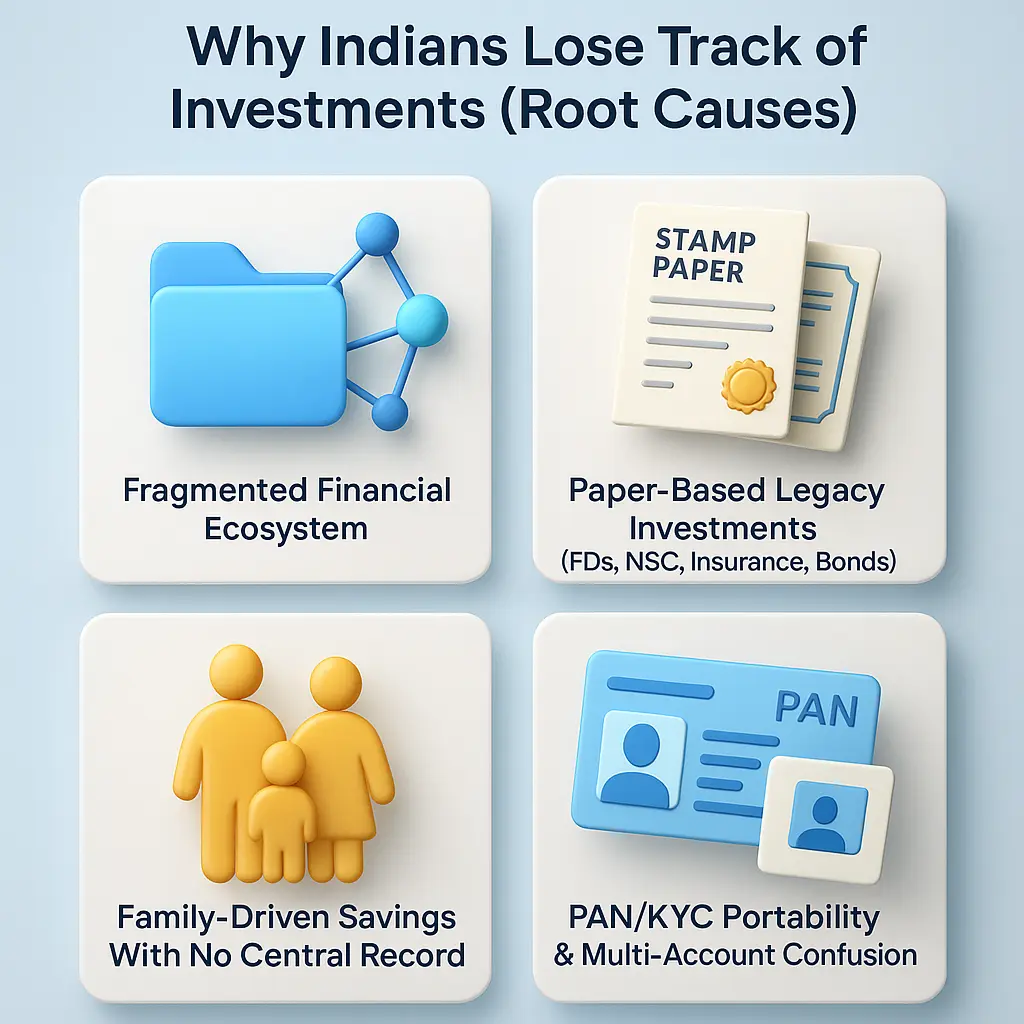

2. Why Indians Commonly Lose Track of Their Investments

The issue of lost investments in India is not accidental-it is rooted in how our financial system has evolved and how households traditionally manage money. From fragmented financial products to poor documentation standards, multiple structural and behavioural forces create blind spots that ultimately lead to unclaimed investments in India and wealth leakage.

Below are the core reasons investors, even financially aware ones, lose visibility and control.

2.1 Fragmented Financial Landscape: Too Many Institutions, No Unified View

India’s investment ecosystem spans banks, cooperatives, post offices, insurers, brokers, AMCs, and digital platforms-each operating in silos. Most households accumulate assets across 8-12 different entities over decades.

Why this creates lost visibility:

- No centralised reporting for multi-asset portfolios.

- Statements, passbooks, and policy documents all follow different formats.

- Older investments sit in offline accounts while newer ones shift to digital systems.

- Family members often use different banks and providers, multiplying complexity.

The result is simple but damaging: when information is scattered across multiple touchpoints, forgotten investments India becomes an inevitable outcome.

2.2 Paper-Based Legacy Products: High Risk of Misplacement and Non-Tracking

A large portion of Indian household wealth still sits in long-term, paper-heavy instruments:

- Fixed Deposits (FDs) with physical receipts

- Post Office schemes (NSC, KVP, MIS, RD) recorded only on passbooks

- Traditional insurance bonds requiring manual premium tracking

- Gold purchase invoices, not stored systematically

- Physical mutual fund statements or folios from pre-demat days

How this contributes to lost investments in India:

- Physical documents are easily misplaced, damaged, or lost during house moves.

- Many products have long maturities (5–20 years), making tracking inconsistent.

- Investors often forget to update contact details, leading to undelivered reminders.

- Families do not always know where certificates or receipts are kept.

These legacy assets form one of the highest categories of unclaimed investments in India, simply because documentation breaks down over time.

2.3 Family-Driven Savings Behaviour: Scattered Decisions Across Members

Indian households typically manage money collaboratively-but not always systematically. Savings are often influenced by parents, spouses, siblings, and elders, leading to distributed, undocumented decisions.

This causes tracking failures such as:

- One family member opening FDs that others are unaware of.

- Insurance policies purchased “just in case,” but not documented or shared.

- Gold accumulated over years without valuation records or inventory tracking.

- Real estate papers stored by different relatives without a central record.

In household wealth management, lack of shared visibility is one of the biggest reasons for lost investments in India, especially during emergencies or succession.

2.4 Multiple PANs, KYC Gaps, and Limited Account Portability

India’s regulatory framework has improved, but historical inconsistencies still affect millions of investors.

Common pain points include:

- Investors with two PANs (due to marriage name changes or old applications).

- KYC completed in one system but not updated across banks or brokers.

- Address changes not propagated across institutions.

- Old accounts that cannot be easily linked to new mobile numbers or emails.

These gaps create mismatches in ownership records, causing:

- Missed communication from institutions

- Dormant accounts that slip out of view

- Assets that beneficiaries cannot claim due to incomplete KYC

Such structural issues are a major driver of lost investments in India, especially for older-generation assets.

Collectively, these factors explain why even disciplined individuals end up with forgotten investments India and unclaimed wealth. The following sections explore the deeper behavioural patterns and the measurable financial impact of these visibility gaps.

3. Behavioral Causes: How Human Biases Lead to Investment Blind Spots

Beyond system-level issues, a significant portion of lost investments in India can be traced back to predictable human behaviours. These biases shape how households make decisions, store documents, delegate responsibilities, and recall financial information. Understanding these psychological patterns is essential for anyone trying to improve how to track investments and build long-term visibility.

Indian families are not careless-they are operating in a complex environment with long-tenure products, multiple stakeholders, and inconsistent documentation. Human behaviour simply fills the gaps.

3.1 The “Set and Forget” Mindset With Long-Term Products

Indian investors often treat long-tenure financial products as one-time decisions. Traditional instruments like PPF, NSC, insurance policies, and FDs are purchased with the belief that they will “take care of themselves.”

This mindset creates blind spots because:

- Products mature in 5, 10, or 15 years-well beyond most people’s natural recall cycles.

- Renewals, nominations, and address updates are rarely revisited once the product is purchased.

- Many investors assume institutions will track everything automatically, which is rarely true for older or offline assets.

Example: A family invests in NSCs for a child’s future but forgets the physical certificates in a locker. 10 years later, nobody remembers the exact maturity date-a typical pathway to lost investments in India.

3.2 Mental Accounting Bias and Scattered Decision-Making

Indian households mentally categorise money into separate buckets-“gold for weddings,” “FDs for emergencies,” “post office schemes for parents,” “SIP for the child.” While helpful for goal-setting, this habit fragments the overall portfolio.

This bias results in:

- Investments distributed across multiple institutions without a central record.

- Inconsistent tracking because each asset is mentally assigned a different “owner.”

- Partial recall, where families remember why they invested but not the specifics of the investment itself.

Mental accounting makes investment documentation irregular, leading to overlooked folios, forgotten SIPs, or untracked small FDs created during bonus seasons.

3.3 Overconfidence in Memory and Underestimation of Complexity

A surprising number of investors rely on memory to track assets-especially those who have invested for decades. People assume they will remember maturity dates, premium cycles, demat accounts, or locker contents.

This confidence becomes risky because:

- Financial lives become more complex over time-multiple bank accounts, insurance plans, mutual funds, digital wallets, and real estate documents.

- Memory recall drops dramatically for low-frequency events like 5-year or 10-year renewals.

- Important details like nominations, folio numbers, and document locations are forgotten.

This is how people unintentionally add to the pool of lost investments in India-not through neglect, but through misplaced confidence.

3.4 Delegation to Family Members Without Shared Visibility

Indian families often divide financial responsibilities informally:

- One spouse handles insurance

- Another manages SIPs

- Parents handle FDs

- Siblings manage property documents

While this division seems efficient, it rarely comes with structured visibility.

Common consequences include:

- Critical documents stored by one person but unknown to others.

- Investments made in someone’s name but tracked by someone else.

- Assets forgotten after a family member moves, marries, or passes away.

This is one of the biggest long-term risks in family wealth management, where delegation without documentation leads to unintentional wealth loss.

Example: A parent buys a traditional LIC policy for a child, pays premiums for years, but never communicates the policy details. When the parent is no longer around, the policy becomes another case of unclaimed wealth-a preventable form of lost investments in India.

Human behaviour, while natural, creates systematic tracking gaps. The next section will explore how structural and institutional issues further amplify these blind spots-and how they collectively turn organised financial plans into forgotten or unclaimed assets.

4. Systemic Causes: Structural Issues That Make Tracking Difficult

Even the most disciplined investors struggle with personal finance organization when the broader financial ecosystem itself is fragmented. Several institutional and structural constraints make it easy for households to lose visibility, leading to a growing volume of lost investments in India. These systemic gaps persist despite digital progress and directly weaken long-term wealth management.

4.1 Non-Standardized Statements Across Banks, AMCs, and Insurers

Every financial institution follows its own reporting format. Banks issue monthly PDFs, AMCs send CAS statements, insurers share renewal notices, and post offices still rely on physical updates.

Why this causes tracking failures:

- No unified layout or terminology; every statement looks different.

- Multiple folio numbers, policy numbers, and account IDs across providers.

- Difficult for families to maintain consistent historical records.

- Inadequate reminders for long-term or offline products.

Without standardization, households spend disproportionate time reconciling data, and assets easily slip into the category of lost investments in India.

4.2 Offline Products and Physical Documents at Constant Risk

A large share of Indian wealth still relies on physical proof-FD receipts, NSC certificates, property papers, gold invoices, and insurance bonds.

Key risks include:

- Loss during house shifts, renovations, or reorganizing cupboards.

- Damage due to moisture, termites, or ageing.

- Storage in multiple locations: home, lockers, relatives’ houses.

- Missing nomination updates on paper-based legacy accounts.

When documentation is physical and scattered, the probability of financial visibility drops sharply. Many dormant or forgotten assets can be traced back to misplaced paperwork.

4.3 Poor Digital Interoperability Across Institutions

Despite Aadhaar, CKYC, PAN, and digital onboarding, India’s financial infrastructure remains siloed. Data does not flow seamlessly between providers.

Common interoperability barriers:

- Bank KYC updates do not reflect in insurance or mutual fund records.

- Mobile number or email changes must be updated separately across platforms.

- Government portals (EPFO, Post Office, PM Schemes) have limited integration with fintech systems.

- Legacy accounts opened decades ago cannot be digitally linked.

This fragmentation means that reminders, statements, and alerts often fail to reach investors-a major contributor to lost investments in India and unclaimed proceeds.

4.4 Limited Multi-Asset Consolidation Tools for the Average Household

Most available platforms focus on a single asset class-equity, mutual funds, or insurance. But Indian portfolios are deeply diversified, including real estate, gold, FDs, post office schemes, and government bonds.

This creates structural tracking gaps:

- No single dashboard for all assets across digital and offline categories.

- Families maintain spreadsheets that quickly become outdated or incomplete.

- Hard to track maturities, renewals, and document validity across products.

- Multi-generational portfolios lack a centralized investment tracking system.

As a result, entire categories of wealth-especially older, offline, or low-frequency assets-become invisible over time and fall into the pool of lost investments in India.

These systemic constraints make it clear that even organised investors face institutional roadblocks. Without stronger digital integration, standardized reporting, and consolidated tracking, households will continue to struggle with financial visibility-regardless of intent or discipline.

5. The Real Risks of Lost or Untracked Investments

When assets slip out of sight, the financial consequences are far more severe than most households anticipate. The growing pool of lost investments in India represents not just forgotten money, but lost compounding, tax penalties, and delays in accessing funds when families need them most. These risks accumulate silently and can weaken long-term household wealth management.

5.1 Unclaimed Deposits, Unpaid Insurance, and Dormant Investments

India already has tens of thousands of crores in unclaimed investments in India, spread across banks, insurers, mutual funds, and small savings schemes. Much of this wealth was never intentionally abandoned-it was simply not tracked.

Common scenarios include:

- FDs maturing silently because the investor changed phone numbers or moved cities.

- Life insurance policies where premiums were missed unintentionally, resulting in policy lapse.

- Post Office schemes like NSC or MIS that are forgotten due to missing physical certificates.

Example: A ₹1,00,000 FD forgotten for 10 years at a 6% rate loses nearly ₹80,000 in potential compounded growth if it remains idle or gets renewed at a lower rate without visibility.

Unclaimed money is not just “missing”-it is expensive.

5.2 Lapsed Policies, Missed Maturity Dates, and Loss of Compounding

Long-tenure products are particularly vulnerable to tracking failures. When investors forget renewal cycles or maturity timelines, the financial impact compounds.

Key risks:

- Lapsed insurance policies offer no protection and no return after years of premiums.

- Missed PPF or SSY contributions reduce long-term corpus growth.

- Bonds and FDs automatically renew at lower interest rates without consent.

- Idle funds remain in low-yield accounts instead of being reinvested.

Example: Missing a renewal on a ₹20,000 annual LIC premium for just two years can reduce the final maturity value by ₹1–2 lakh, depending on the policy term.

These gaps directly reduce wealth creation potential.

5.3 Tax Inefficiencies and Penalties Due to Poor Documentation

Inadequate tax documentation for investments leads to avoidable penalties, disputes, or missed tax-saving opportunities.

Common tax-related risks:

- Missing old capital gains statements results in higher tax outgo when selling assets.

- Forgotten FDs or bonds generate unnoticed interest, creating compliance gaps.

- Incomplete records make it difficult to claim TDS refunds.

- Untracked investments cause under-reporting or over-reporting in ITR filings.

Example: If TDS of ₹3,000 on FD interest isn’t claimed because the FD was forgotten, the investor effectively loses that refund permanently.

Lost documentation often translates directly into lost money.

5.4 Family Wealth Erosion During Emergencies or Succession

This is one of the most critical but underestimated consequences of lost investments in India. When key financial details reside only in one person’s memory, families face uncertainty during emergencies, illness, or inheritance.

Key vulnerabilities:

- Family members may not know the location of property documents or insurance papers.

- Post Office and small savings scheme records are often accessible only to the original investor.

- Multiple bank accounts, demat accounts, and lockers go unclaimed due to incomplete visibility.

- Beneficiaries struggle to claim assets without nominations or proper documentation.

Example: A family unaware of a parent’s ₹5 lakh insurance policy may lose the entire amount simply because no one has the policy number or insurer details.

This is not just a financial loss-it is a breakdown in intergenerational wealth continuity.

The risks of lost investments in India extend far beyond misplaced documents. They translate into lower returns, higher taxes, delayed claims, and reduced family security. The next sections will quantify these impacts further and outline a structured plan to build full visibility across your financial life.

6. Data Insights: What Indian Studies Reveal About Wealth Visibility

The scale of lost investments in India becomes clearer when viewed through official data. Reports and disclosures from RBI, IRDAI, AMFI, and SEBI consistently highlight rising volumes of unclaimed or dormant assets-a direct result of weak investment documentation, fragmented systems, and low financial visibility across households.

These numbers illustrate not only forgotten money but also the operational drag created by disorganised portfolios.

6.1 RBI Data: Rising Unclaimed Deposits and Dormant Bank Accounts

RBI’s public disclosures show a steady increase in unclaimed deposits across banks. As of recent updates, unclaimed amounts have crossed ₹42,000 crore, much of it linked to:

- Dormant bank accounts

- Forgotten FDs

- Unreturned maturity proceeds

RBI also notes that millions of accounts become dormant every year due to inactivity, outdated KYC, and missing contact information-all major contributors to lost investments in India.

6.2 IRDAI Data: Large Volumes of Unclaimed Insurance Proceeds

IRDAI regularly reports substantial unclaimed insurance payouts, often exceeding ₹25,000 crore across life and general insurers. Most of this arises because:

- Policyholders shifted cities or changed phone numbers

- Families remained unaware of existing policies

- Premiums lapsed without record-keeping

- Claims were never initiated due to missing documents

This reinforces the need for stronger family-level documentation in financial planning.

6.3 AMFI & SEBI Insights: Unclaimed Dividends and Forgotten Mutual Fund Folios

AMFI data shows thousands of crores in unclaimed mutual fund dividends, often due to:

- Bank account mismatches

- Old folio numbers not mapped to new KYC

- Investors forgetting reinvestment vs. payout options

- Email and mobile details not updated

SEBI has repeatedly highlighted that many households lack a consolidated view of their folios, particularly legacy ones created before digitisation.

6.4 Household Productivity Costs: Time Lost Searching for Information

Beyond financial loss, Indian households face significant productivity drain due to missing information. Poor organisation forces families to repeatedly search for:

- Old FD receipts

- Insurance bonds

- Property documents

- Past-year statements

- Salary slips and tax proofs

It’s common for families to spend 5–10 hours per year simply recovering misplaced documents or chasing institutions for records. For multi-generational families, this can escalate to 20+ hours, reducing decision speed and increasing stress during emergencies.

This hidden productivity cost is a major but under-recognised consequence of lost investments in India.

Snapshot: Types of Unclaimed or Dormant Investments in India

| Type of Asset / Investment | Common Reason for Loss | Estimated Financial Impact |

|---|---|---|

| Bank FDs & Savings Deposits | Dormant accounts, outdated KYC | Lower returns, loss of compounding on ₹42,000+ crore |

| Insurance Policies | Unclaimed payouts, lapsed premiums | ₹25,000+ crore in unpaid benefits |

| Mutual Fund Dividends | Old folios, bank mismatches | Thousands of crores sitting unclaimed |

| Equity Dividends | Physical shares, address changes | Large sums moved to IEPF due to non-claimed dividends |

These data points show that lost investments in India are not isolated events-they represent a national pattern of fragmented systems, poor documentation, and low portfolio visibility. The next section will translate these insights into measurable financial impact and long-term wealth implications.

7. Financial Impact: How Poor Tracking Reduces ROI and Increases Risk

The financial consequences of disorganised portfolios go far beyond inconvenience. Poor tracking erodes returns, increases tax leakage, delays family decisions, and amplifies risk exposure. A large portion of lost investments in India stems from these avoidable inefficiencies-each of which compounds over time. When households fail to track investments in India systematically, the long-term cost can run into lakhs.

7.1 Quantifying the Cost of Missed Maturity Dates and Ignored Statements

Missed maturities are one of the biggest causes of silent wealth erosion. When products roll over automatically or maturity proceeds stay idle, returns drop significantly.

Common financial impacts:

- FDs often auto-renew at 2–3% lower interest rates than the original term.

- NSCs and KVPs that mature but are not encashed lose 100% of potential reinvestment gains.

- Traditional insurance payouts may lie unclaimed for years due to missed communication.

Example:

A ₹2,00,000 FD maturing at 7% but auto-renewing at 4% for five years results in a loss of nearly ₹70,000 in missed interest.

The ROI loss due to poor tracking is immediate and measurable.

7.2 Impact on Financial Planning, Asset Allocation, and Liquidity

When households lack a unified view of assets, financial planning becomes reactive instead of strategic.

Key consequences:

- Overexposure to low-yield products (FDs/post office schemes) without realising it.

- Underutilisation of liquid funds during emergencies, forcing high-interest borrowing.

- Excess cash sitting in dormant accounts instead of compounding.

- Poor goal alignment due to unknown timelines or undocumented asset values.

Example:

A family keeping ₹1,50,000 in a dormant account earning 2.5% instead of deploying it into a 7% instrument loses ₹6,750 every year simply due to oversight.

Over decades, this compounds into lakhs of avoidable opportunity loss.

7.3 The Cost of Delayed Family Decisions and Information Bottlenecks

A fragmented, undocumented financial landscape slows down decision-making. Families often take weeks to “gather all documents” before investments, claims, or tax filings.

This leads to:

- Delayed reinvestment after redemption or maturity.

- Missed tax-saving deadlines such as 80C or capital gains exemptions.

- Slower loan processing due to incomplete documentation.

- Inability to act quickly during market opportunities.

Example:

If a family delays reinvesting ₹5,00,000 for three months because documents were missing, they lose ₹8,750–10,000 in forgone returns (assuming 7–8% annual yield).

This productivity drag is a major hidden cost in personal wealth tracking.

7.4 Measuring Long-Term Wealth Drag of Disorganised Portfolios

Disorganisation affects long-term wealth more than daily spending habits. When visibility is poor, investors make less informed decisions, leading to structural inefficiencies.

Long-term financial drag includes:

- Suboptimal asset allocation reducing potential CAGR by 1–2% annually.

- Missed compounding on reinvestment delays cutting long-term corpus growth by 10–20%.

- Inability to optimise taxes resulting in annual leakage of ₹5,000–₹25,000 for average households.

- Lost or forgotten assets reducing net worth visibility by 5–15% for many families.

Even a modest 1% reduction in portfolio CAGR over 20 years can shrink a ₹10 lakh investment by ₹7 lakh-a massive impact caused purely by poor tracking.

When viewed collectively, these numbers show how lost investments in India and poor tracking systems silently weaken household financial health. The next section will outline practical, structured solutions to reverse this wealth drag and build a high-visibility, high-efficiency portfolio.

8. Practical Solutions: How Indians Can Build a High-Visibility Investment System

Preventing lost investments in India requires structure, discipline, and the right tools. Most households don’t need complex financial software-they need a clear, repeatable system that improves visibility and reduces dependency on memory. The following steps help build an organised, future-ready investment tracking system tailored to Indian portfolios.

8.1 Set Up a Structured, Asset-Class-Wise Documentation Approach

Start by creating a single, central record of every financial asset your family owns. This forms the backbone of strong personal finance organization.

Steps to implement:

- List all asset classes-FDs, mutual funds, PPF, NPS, insurance, post office schemes, real estate, gold, bonds, demat holdings.

- Document essential details-account/folio numbers, maturity dates, premium schedules, nominee details, and institution contacts.

- Create a uniform structure-one format for all assets so information becomes easy to update annually.

- Include ownership mapping-who owns what, and who is the nominee for each item.

This reduces the chance of blind spots and ensures no product quietly turns into a forgotten or dormant asset.

8.2 Create a Digital Backup System for All Critical Documents

Digitising investment records is crucial for long-term security. Paper-based files deteriorate over time, and misplaced documents are one of the biggest causes of lost investments in India.

How to implement digital continuity:

- Scan every financial document-FD receipts, NSC/KVP certificates, property papers, insurance bonds, share certificates.

- Use a secure cloud drive (Google Drive/OneDrive/iCloud) with two-factor authentication.

- Create organised folders-one for each asset class, with naming consistency.

- Add PDF statements and renewal notices as soon as you receive them.

- Back up on two separate platforms to prevent data loss.

This ensures every asset remains accessible, even if physical documents are lost or damaged.

8.3 Standardize Naming, Mapping, and Renewal Tracking

Consistency is the foundation of a robust investment tracking system. When everything follows a predictable format, you avoid confusion and reduce errors.

Practical standards to adopt:

- Adopt a naming format-e.g., “FD_HDFC_2025_Maturity” or “LIC_JeevanLabha_PolicyNo”.

- Tag every document with the owner’s name and asset type.

- Maintain a single renewal calendar for premiums, maturities, SIPs, EMIs, and policy anniversaries.

- Use reminders-monthly, quarterly, and annual-so no date is missed.

- Record changes immediately-new bank accounts, mobile numbers, nominees, address updates.

This prevents maturity leaks, lapsed policies, and the subtle ROI loss caused by inconsistent tracking.

8.4 Define Family-Level Visibility Protocols for Continuity and Security

Most gaps in Indian household tracking arise because only one person knows where documents are. To prevent long-term lost investments in India, families need structured visibility-not casual sharing.

Family-level protocols to establish:

- Identify a primary and secondary custodian for financial records.

- Share access to key documents with spouse or adult children via secure folders.

- Maintain an emergency file listing must-know assets and contacts.

- Update nominees across banks, insurers, and mutual funds to match family goals.

- Conduct a quarterly review where the entire family gets a status update.

When every stakeholder knows what exists, where it is stored, and who manages it, long-term continuity becomes seamless.

A disciplined, structured approach to documentation and visibility can eliminate 80–90% of risks associated with fragmented portfolios. The next section explores digital tools that make these steps easier and help Indian families maintain financial clarity across generations.

9. Digital Tools That Reduce Investment Blind Spots

A significant portion of lost investments in India can be prevented simply by using the right digital tools. Modern platforms help investors consolidate data, store documents securely, and maintain real-time visibility across asset classes. The goal is not to complicate personal finance, but to use technology to simplify tracking and reduce dependency on memory or paper-based systems.

9.1 Consolidators and Reporting Systems for Equity, Mutual Funds, and Insurance

Digital consolidators have become essential for households that want visibility across financial products held in different institutions.

Key benefits include:

- Portfolio snapshots across mutual funds, stocks, NPS, and insurance.

- Automated transaction updates instead of manual entries.

- CAS integration for consolidated mutual fund reporting.

- Policy information retrieval via insurer data links.

These systems reduce oversight errors and help households detect gaps before they turn into unclaimed or lost investments in India.

9.2 Secure Document Vaults and Reminder Systems

Document vault apps and digital lockers solve one of India’s biggest problems-misplaced paper documents.

Important capabilities:

- Upload and organise FD receipts, NSC certificates, insurance bonds, property papers.

- Enable restricted sharing with family members for continuity.

- Set maturity, premium, and renewal reminders to avoid lapses.

- Maintain long-term digital continuity even if physical copies degrade.

For families juggling multiple accounts and assets, a secure vault eliminates the risk of losing critical evidence of ownership.

9.3 Multi-Asset Trackers for Real Estate, Gold, and Alternative Assets

Most wealth in India sits outside the stock market-in real estate, gold, and traditional savings instruments. Yet tracking tools for these categories remain limited.

Multi-asset trackers help by:

- Recording property details, purchase documents, valuations, and loan information.

- Maintaining gold inventories with invoices and updated valuations.

- Tracking government schemes like SCSS, POMIS, KVP, and Sukanya Samriddhi.

- Creating a unified portfolio view instead of scattered records across households.

This helps families make evidence-based decisions instead of relying on fragmented memory.

9.4 Where My Wealth Locker Fits In: A Unified Dashboard for Visibility & Continuity

For families seeking a single view of their entire financial landscape, a structured platform like the My Wealth Locker app can help reduce blind spots without adding complexity. It functions as a multi-asset, multi-format organiser rather than a transactional platform.

How it supports long-term tracking:

- Brings together bank deposits, insurance, mutual funds, gold, property records, and government schemes into one wealth tracking app.

- Offers a secure digital vault for storing and retrieving investment documents when needed.

- Helps maintain family-level visibility by enabling controlled access for dependents.

- Ensures continuity for offline assets and legacy products that are often overlooked in digital systems.

By simplifying document storage and providing a consolidated dashboard, My Wealth Locker works as a wealth management app that enhances clarity and reduces the risk of assets slipping into the category of lost investments in India.

Digital tools don’t replace financial discipline-they reinforce it. With the right combination of consolidation, secure storage, and multi-asset tracking, Indian families can significantly improve their visibility, reduce leakages, and maintain long-term control over their wealth.

10. How My Wealth Locker Enhances Productivity and Reduces Financial Risk

A structured, centralised system can significantly lower the probability of lost investments in India, especially when households manage multiple financial products across banks, insurers, post office schemes, and physical assets. My Wealth Locker is designed to serve as a practical, business-like organiser-reducing manual effort, preventing document loss, and improving financial visibility. It functions not as a transactional product, but as a personal wealth tracking app that brings discipline, continuity, and clarity to household finances.

10.1 Automating the Essentials: Timely Alerts and Zero Missed Deadlines

Most investment leakage happens because families miss renewals, maturities, or premium deadlines. Automation closes this gap.

Key productivity and risk-reduction benefits include:

- Automated alerts for FD maturities, NSC/KVP renewals, insurance premiums, PPF deadlines, and policy expiries.

- Reduction in manual calendar tracking, which is especially important for multi-generational households.

- Lower chances of products becoming inactive, unclaimed, or slipping into forgotten status.

By eliminating dependence on memory, My Wealth Locker helps households create timely, confident decisions-a core barrier behind lost investments in India.

10.2 Reduced Tracking Errors Through Centralised Document Storage

Physical paperwork is one of the biggest sources of friction in India’s wealth landscape. A secure, organised system dramatically lowers the risk of missing or misplaced documents.

How the app strengthens documentation discipline:

- Stores digital copies of FD receipts, insurance bonds, property papers, gold invoices, and postal scheme certificates.

- Creates structured folders for every asset class-improving retrieval accuracy.

- Maintains continuity even when physical documents degrade, shift locations, or are stored across multiple family homes.

- Minimises disputes or delays during claims, renewals, or verification processes.

As an investment document storage app, it ensures that critical proofs remain intact and accessible, preventing asset loss due to missing paperwork.

10.3 Safe Family-Level Access and Continuity Planning

Many Indian households face financial disruptions because key information sits with one person. Lack of structured sharing is a hidden factor behind long-term lost investments in India.

My Wealth Locker improves continuity and family-level coordination through:

- Controlled access for spouses, children, or dependents without exposing sensitive data unnecessarily.

- Clear documentation of what exists, where it is stored, and how it can be claimed.

- Improved decision-making during medical emergencies, travel, or generational transition.

- Lower admin costs and faster settlement when family members have the right information at the right time.

This enables families to move from fragmented knowledge to shared visibility-a shift that strengthens household resilience and prevents wealth erosion.

With automation, structured documentation, and secure family visibility, My Wealth Locker helps Indian households operate with greater clarity and discipline. The result is measurable: less leakage, fewer errors, higher productivity, and significantly reduced risk of lost investments in India.

11. Real-World Scenarios: How Investments Get Lost-and How to Fix Them

Understanding how everyday situations lead to lost investments in India helps households build stronger prevention systems. These scenarios reflect common challenges across Indian families-misplaced documents, fragmented information, and reliance on memory instead of structured processes. Each example shows what typically goes wrong and how a disciplined approach to household wealth management can fix it.

11.1 Misplaced FD Receipts and Maturity Misses

A retiree renews FDs every few years but stores the receipts in different folders, some in a bank file and others at home. When one FD matures, the family doesn’t realise it for months, delaying reinvestment and losing interest income.

Fix: Maintain a digital backup of all FD receipts, set maturity reminders, and consolidate bank-wise deposits so you can track investments in India without relying on scattered paperwork.

11.2 Forgotten Insurance Policies and Lapsed Benefits

A salaried professional buys a traditional life insurance plan ten years ago but never updates his address or email. Over time, premium notices stop arriving, and the policy quietly lapses. Years later, the family assumes it is still active, creating a financial gap.

Fix: Create a central insurance register, store policy documents digitally, and activate premium reminders to prevent these avoidable lost investments in India.

11.3 Single-Member Knowledge Leading to Family Blind Spots

In many households, one person-often the husband, wife, or parent-handles all finances. When that person travels, falls ill, or is unavailable, no one else knows about FDs, SIPs, insurance, gold invoices, or property documents. This leads to confusion during emergencies and long-term asset loss.

Fix: Share a controlled, need-to-know summary of all assets with at least one family member to ensure household wealth management is not dependent on a single individual.

11.4 Multi-Generational Document Tracking Challenges

A family inherits property and old postal savings from grandparents, but the documents are stored across multiple relatives’ homes. Some papers are torn, others missing, and a few products were never updated with nominees. Years later, the family spends weeks searching for proof, and some assets remain unclaimed.

Fix: Digitise all legacy documents, tag them by asset category, record ownership details, and maintain a searchable archive to avoid multi-generational lost investments in India.

These examples reflect the everyday realities that quietly erode wealth across Indian families. With structured documentation, digital backups, and shared visibility, households can prevent these losses and build a resilient, trackable financial system.

12. The Strategic Value of a Centralized Wealth Visibility System

A structured, centralised framework for managing personal finance does more than prevent lost investments in India–it transforms how families make decisions, optimise returns, and secure long-term financial continuity. When all assets, documents, and timelines sit in one place, households move from reactive management to proactive wealth strategy. Improved financial visibility becomes a measurable competitive advantage for any family.

12.1 Faster, More Confident Financial Decisions

When information is scattered, decisions slow down-whether it’s choosing between FDs and mutual funds, refinancing a loan, or reallocating underperforming assets. A central dashboard speeds up evaluation and reduces dependency on memory.

Strategic benefits include:

- Immediate access to asset values, liabilities, and upcoming maturities.

- Faster rebalancing during market changes.

- Reduced friction in comparing options and selecting the best-fit product.

- Shorter decision cycles for high-value choices like property or insurance.

A well-structured investment tracking system makes households more agile and better prepared for financial opportunities.

12.2 Higher ROI Through Better Optimisation and Tax Planning

Disorganised finances silently erode returns. Missed lock-in periods, ignored maturity dates, and delayed tax documentation each create micro-losses that compound over time. With centralisation, these losses shrink dramatically.

Key optimisation gains:

- Timely reinvestment of maturing deposits and bonds to avoid idle funds.

- Better tax planning through consolidated visibility of 80C, capital gains, and TDS credits.

- Early identification of underperforming assets.

- Smoother documentation flow during ITR filing.

A reliable personal wealth tracking approach ensures decisions are made based on data, not assumptions-directly improving long-term ROI.

12.3 Reduced Disputes, Smoother Family Coordination, and Empowered Dependents

A large share of lost investments in India arises after life events-illness, relocation, or generational transition. The absence of a single source of truth creates confusion, delays, and sometimes family disputes.

Centralised visibility enhances continuity by:

- Reducing uncertainty about who owns what and where documents are stored.

- Ensuring nominees, dependents, and spouses can act quickly when required.

- Minimising conflicts caused by missing papers or contradictory information.

- Enabling a clear, shared understanding of wealth distribution and obligations.

This shift empowers families, protects assets, and ensures wealth transfers smoothly without operational shocks.

A centralised wealth visibility system is not just an organisational tool-it is a strategic asset. It raises productivity, strengthens decision-making, and significantly reduces the risk of financial leakage. For Indian households navigating both traditional and modern investments, this structure is essential for long-term financial stability and clarity.

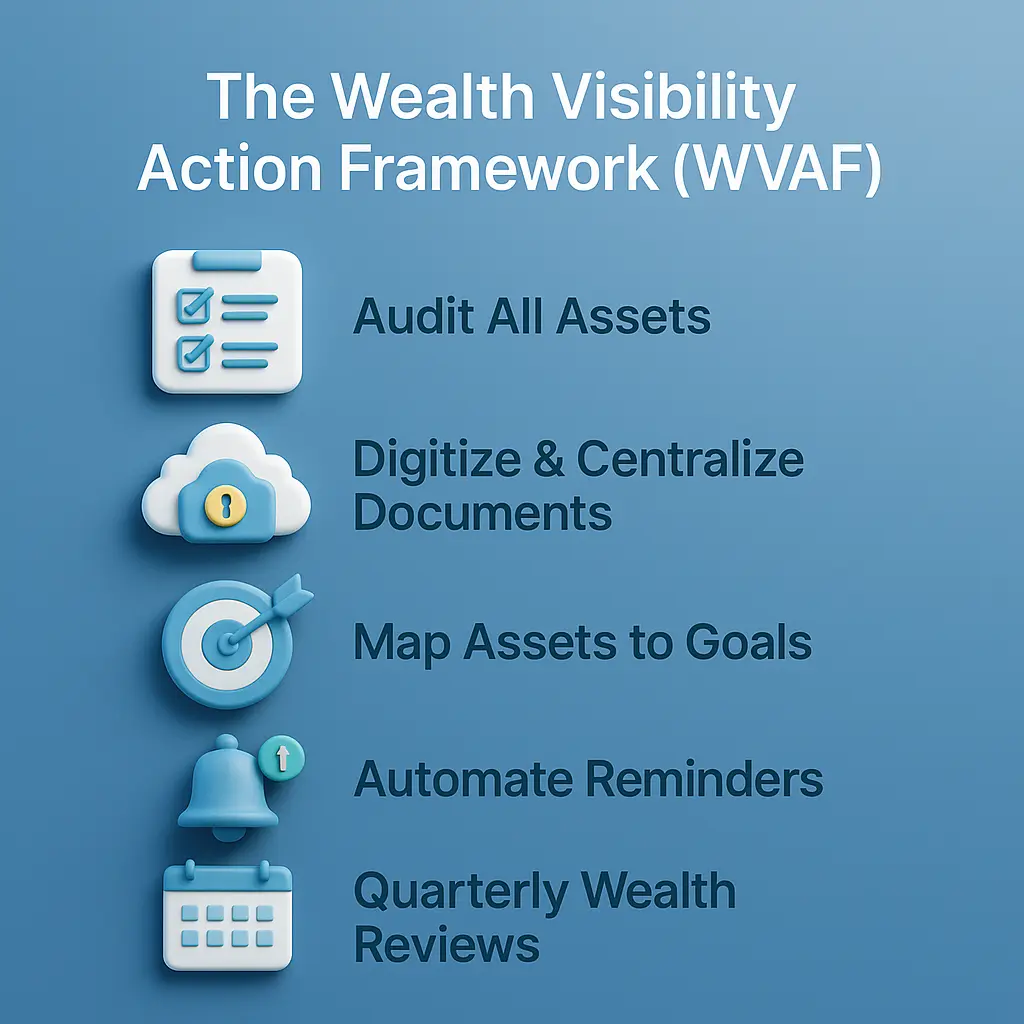

13. The Wealth Visibility Action Framework (WVAF)

A structured, repeatable process is the most effective way to eliminate lost investments in India and bring discipline to personal finance. The Wealth Visibility Action Framework (WVAF) is a five-step model designed for Indian households managing both modern and legacy assets. It enhances clarity, reduces leakages, and builds long-term financial confidence through systematic personal finance organization.

13.1 Step 1: Audit Every Asset You Own

Begin with a comprehensive, zero-assumption asset audit. Most families underestimate how many documents, accounts, and certificates they actually hold.

- List all bank accounts, FDs, NSCs, insurance policies, mutual funds, and physical assets.

- Identify missing documents, mismatched nominee details, and dormant products.

- Tag each item as “active,” “uncertain,” or “unverified.”

This audit often reveals hidden gaps-the early warning signs that later turn into lost investments in India.

13.2 Step 2: Digitize & Centralize All Financial Records

Once assets are identified, the next step is to remove dependency on scattered files and memory.

Digitizing investment records reduces retrieval time and prevents long-term loss.

- Scan FD receipts, insurance bonds, property papers, and KYC proofs.

- Store them in one secured digital hub.

- Use a consistent naming format for easier search and classification.

A centralized approach immediately strengthens your investment tracking system.

13.3 Step 3: Map Each Asset to a Financial Goal

Financial products deliver the best results when they serve specific, time-bound goals.

- Assign FDs to short-term needs, debt funds to medium-term goals, and equity to long-term growth.

- Align life and health insurance with risk-protection objectives.

- Reassess outdated products that no longer match current priorities.

Goal-based mapping ensures assets work strategically rather than sitting idle or forgotten.

13.4 Step 4: Automate Reminders & Renewal Cycles

A key cause of lost investments in India is missed maturity dates and premium deadlines.

- Set automated reminders for FDs, PPF, SIP renewals, insurance premiums, and loan EMIs.

- Use a unified digital system instead of phone calendars or manual lists.

- Ensure reminders trigger early enough for timely action.

Automation removes human error-the single biggest source of investment leakage.

13.5 Step 5: Conduct Quarterly Visibility Reviews

Visibility improves only when it is refreshed regularly. Quarterly reviews keep the system sharp and updated.

- Check asset performance and ensure documentation is still current.

- Update records after new purchases, redemptions, or nominee changes.

- Review goal alignment and rebalance when needed.

Quarterly reviews reinforce discipline and ensure that personal finance remains organised, accurate, and future-ready.

The WVAF model enables households to move from reactive, paper-driven habits to a structured, high-clarity system. With these five steps, families gain control, minimise leakages, and significantly reduce the long-term risk of lost investments in India.

14. Conclusion

A disciplined, structured approach to wealth tracking is now a strategic necessity, especially as lost investments in India continue to arise from fragmented records, weak follow-ups, and poor intergenerational visibility. When families build a unified system for financial clarity, they move from reactive decisions to proactive wealth building-every asset becomes accessible, every maturity is tracked, and every financial choice becomes faster and sharper.

Strong personal wealth tracking enhances confidence, prevents administrative delays, strengthens tax planning, and ensures continuity across generations, dramatically reducing the risk of lost investments in India. Over the long term, consistent documentation, digitisation, and regular reviews protect against leakages, improve ROI, and ensure that every rupee is working with purpose. With the right investment tracking system, households eliminate blind spots, avoid lost investments in India, and build a resilient, growth-focused wealth strategy-track better, protect more, build faster.