Avoid These Wealth Management Mistakes Indians Commonly Overlook

In India, personal finance conversations often begin with fixed deposits and end with gold or real estate. Yet, according to a 2023 SEBI survey, nearly 70% of Indians admit they have no structured wealth plan. That means for most households, managing money becomes a reaction to life events rather than a strategic, long-term approach. This lack of planning explains why even well-earning individuals sometimes feel stuck despite years of saving. Many of these issues stem from deeply rooted behaviours-cultural beliefs, emotional biases, and outdated financial habits. When you look closely at the wealth management mistakes indians make, it’s clear that the problem isn’t just limited knowledge but also misplaced confidence in traditional methods.

To understand where things go wrong, here are some common patterns:

- Relying heavily on physical assets instead of building a diversified portfolio.

- Delaying investments because of fear, confusion, or lack of professional guidance.

- Following family advice blindly without evaluating risk or long-term impact.

- Mixing insurance and investment without understanding the costs involved.

- Ignoring tax-efficient options that could boost returns significantly.

- Keeping savings idle in low-interest accounts instead of making money work through compounding.

Recognising these patterns helps you avoid the wealth management mistakes Indians make and start building a disciplined, goal-driven financial strategy that grows with you.

The Reality of Wealth Management in India

India’s approach to money is deeply cultural, shaped by traditions passed down through generations. Older family members often encouraged saving instead of investing, which made sense in a slower, less volatile economy. For years, fixed deposits, gold purchases, and real estate were considered the safest choices. But the financial landscape of 2025 is very different-more dynamic, more digital, and far more complex. Unfortunately, many people still rely on outdated strategies, creating gaps in their financial growth and security. This is where many of the wealth management mistakes indians make begin, because habits are slow to change even when the world around us evolves.

To understand why these traditional approaches fall short today, consider the following challenges:

- Inflation consistently outpaces returns from old-school instruments like FDs.

- Financial products have become diverse, yet many invest without research or advice.

- Taxes impact long-term wealth, but planning is often ignored.

- People depend on real estate despite low liquidity and long holding periods.

- Insurance is purchased emotionally rather than strategically, leading to poor coverage.

- Technology-enabled tools exist, but many fail to track or optimise their portfolio regularly.

Recognising these patterns helps you avoid repeating the wealth management mistakes indians make and encourages a shift toward modern, data-driven wealth planning.

1. Lack of Budgeting

Budgeting is one of the most overlooked yet essential pillars of financial stability in India. Since budgeting is rarely taught in schools or discussed openly at home, most people grow up relying on rough mental calculations or casual tracking. This informal approach works only until expenses start rising, responsibilities increase, or income becomes irregular. Without a structured plan, it becomes difficult to understand where money is going, how much is being wasted, and what can realistically be saved. This lack of clarity is often the starting point for many wealth management mistakes indians make, particularly when it comes to controlling spending and planning future goals.

To understand why budgeting is crucial, here are the most common issues caused by not having a proper monthly plan:

- Overspending on non-essentials without realising it.

- Difficulty meeting savings targets due to untracked expenses.

- Emotional or impulsive buying leading to cash shortages.

- Poor investment planning because money is not allocated intentionally.

- Reliance on credit cards or loans during emergencies.

- Misalignment between income, lifestyle, and long-term goals.

The good news is that budgeting has become easier thanks to digital tools. Apps like Walnut, Goodbudget, and ET Money help track expenses automatically, set spending limits, and analyse patterns. Building this habit early helps avoid many wealth management mistakes indians make and lays the foundation for smarter financial decisions.

2. Over-Investing in Real Estate or Gold

For generations, Indian families have viewed real estate and gold as the safest and most reliable investments. Their tangibility provides emotional comfort, and cultural traditions reinforce the belief that these assets will always grow in value. While this may have been true decades ago, the financial landscape today is vastly different. Real estate prices have stabilised in many cities, rental yields are low, and gold often goes through long periods of stagnation. Yet, many investors continue pouring the majority of their savings into these asset classes. This imbalance is one of the classic wealth management mistakes indians make, mainly because it limits financial flexibility and restricts long-term wealth creation.

Here are the biggest issues that arise from over-investing in gold or property:

- Real estate is highly illiquid and difficult to sell during emergencies.

- Gold provides safety but rarely outperforms inflation consistently.

- A large portion of wealth gets locked, leaving little for high-growth investments.

- Overexposure reduces diversification and increases financial risk.

- High maintenance costs and taxes can further erode property returns.

- Emotional bias leads many to ignore better-performing alternatives.

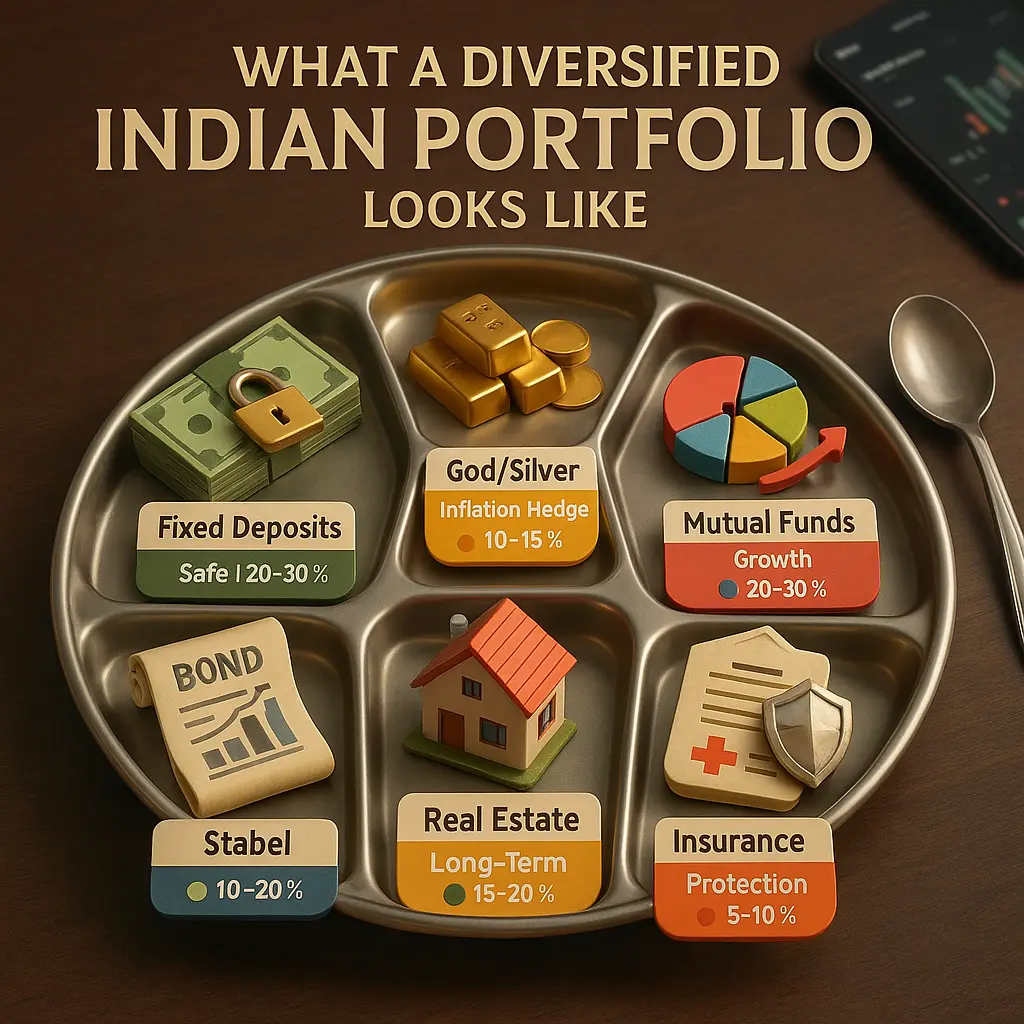

To build a healthier portfolio, it’s essential to limit overdependence on these traditional assets. Adding mutual funds, NPS, bonds, and equities ensures better liquidity, balanced risk, and stronger long-term growth. Avoiding this trap helps reduce the wealth management mistakes indians make and encourages a more modern, diversified approach to investing.

3. Underinsured or Uninsured

Insurance is one of the most misunderstood financial tools in India. Many people assume it is an unnecessary expense, especially when they are young, healthy, or earning well. This mindset often stems from a belief that “nothing will happen,” leading families to postpone buying coverage until it’s too late. But life is unpredictable, and one medical emergency or accident can drain years of savings within days. This lack of protection becomes one of the most expensive wealth management mistakes indians make, because it destabilises financial plans that took years to build.

Here are the most common risks faced by those who remain underinsured or uninsured:

- Medical emergencies that wipe out savings or lead to heavy debt.

- Loss of income after a major illness or disability.

- Dependents facing financial hardship due to the absence of term insurance.

- Difficulty rebuilding long-term goals after sudden financial shocks.

- Relying on employer health insurance, which may be insufficient or temporary.

- Using investments or loans to cover hospital expenses, slowing wealth creation.

The solution is simple: secure adequate health and term insurance based on your income, lifestyle, and family responsibilities. These policies act as financial shock absorbers, protecting your savings and ensuring peace of mind. Avoiding this mistake helps reduce many wealth management mistakes indians make and strengthens your long-term financial stability.

4. Poor Tax Planning

Tax planning is often treated as a last-minute activity in India. Most people wait until March to make hurried investment decisions, usually under pressure from employers or peers. This reactive approach results in missed opportunities for deductions, poor product selection, and investments that don’t align with long-term financial goals. Proper tax planning should be a year-round habit, not a seasonal rush. When individuals ignore this, it becomes one of the recurring wealth management mistakes indians make, because it directly affects returns, liquidity, and overall financial efficiency.

Here are the major issues that arise from poor tax planning:

- Investing in unsuitable products just to claim Section 80C deductions.

- Missing additional benefits under Sections 80D, 24(b), or NPS deductions.

- Paying more tax than necessary due to lack of documentation or awareness.

- Locking money into long-term schemes without understanding liquidity.

- Choosing insurance-cum-investment plans that offer poor returns.

- Failing to use employer benefits such as HRA or LTA effectively.

Modern fintech tools like ClearTax, TaxBuddy, and Black app simplify tax optimisation by providing real-time insights, deduction tracking, and personalised recommendations. When used consistently, these platforms help individuals make smarter choices throughout the year. Strengthening this habit is essential to avoid repeating the wealth management mistakes indians make and to maximise long-term wealth.

5. No Emergency Fund

An emergency fund is one of the simplest yet most powerful financial safety nets, but many Indians overlook it. Culturally, the focus has always been on saving for big goals-buying a house, children’s education, or weddings-while everyday risks are ignored. As a result, when unexpected events like job loss, medical emergencies, or urgent repairs occur, people are forced to rely on personal loans or high-interest credit cards. This creates a debt spiral that derails long-term financial plans. Not building an emergency buffer is one of the most avoidable wealth management mistakes indians make, because it exposes families to unnecessary financial stress.

Here are the major consequences of skipping an emergency fund:

- Borrowing at high interest during medical or financial emergencies.

- Liquidating investments prematurely, leading to losses or penalties.

- Increased dependence on credit cards and personal loans.

- Disruption of long-term goals like retirement or child education.

- Emotional stress and uncertainty during difficult situations.

- Inability to manage sudden expenses such as home or vehicle repairs.

The solution is simple and practical: set aside 3-6 months’ worth of expenses in a liquid mutual fund or a dedicated savings account. This ensures quick access to cash without disturbing investments. Building this buffer early helps prevent many wealth management mistakes indians make and creates a more resilient, secure financial foundation.

6. Investment Diversification Mistakes

Diversification is one of the core principles of smart investing, yet it’s often misunderstood or ignored in India. Many investors follow herd mentality-investing heavily in one trending sector, a single stock, or one type of product because friends, relatives, or social media recommend it. Others become overconfident in an asset class that once gave good returns and continue allocating more money to it without reviewing risks. This lack of balance creates volatility and exposes the portfolio to unnecessary losses. These errors are among the quiet but damaging wealth management mistakes indians make, especially when they rely on instinct rather than data.

Here are the most common issues caused by poor diversification:

- Heavy dependence on one sector that crashes during economic downturns.

- Investing only in equity and ignoring safer assets like debt.

- Putting too much money into gold or real estate and losing liquidity.

- Lack of exposure to government-backed schemes that offer stability.

- Emotional investing instead of following a structured asset allocation plan.

- Missing out on long-term gains due to inconsistent or unbalanced portfolios.

A well-diversified strategy includes equity for growth, debt for stability, gold for hedging, and government schemes for safety. Robo-advisor India platforms make this easier by analysing your goals, risk profile, and timelines. Following this approach helps avoid many wealth management mistakes indians make and builds a portfolio that grows consistently across market cycles.

7. ULIP vs Mutual Funds Confusion

The confusion between ULIPs and mutual funds is one of the most persistent issues in Indian personal finance. ULIPs are often aggressively sold by insurance agents as “double-benefit” products that offer both life cover and investment growth. This sales pitch convinces many first-time investors, especially those who prefer guaranteed or bundled products. However, ULIPs come with high charges, long lock-in periods, and limited flexibility. Mutual funds, on the other hand, offer transparency, lower costs, and better growth potential-but they are often misunderstood or overlooked. Mixing up insurance and investment leads to major financial inefficiencies and remains one of the misleading wealth management mistakes indians make, especially when decisions are influenced by incomplete advice.

Here are the biggest problems caused by ULIP–mutual fund confusion:

- Paying high premiums when pure term insurance would cost much less.

- Lower returns due to high fund management and policy charges.

- Being locked into long-term plans with limited exit options.

- Difficulty understanding performance metrics because ULIPs lack transparency.

- Missing out on the superior flexibility and diversification of mutual funds.

- Emotional buying based on trust in agents rather than factual comparison.

The smart approach is simple: keep insurance and investments separate. Term insurance protects your family, while mutual funds build long-term wealth. Following this structure helps avoid several wealth management mistakes indians make and ensures your financial choices remain efficient, flexible, and goal-oriented.

8. SIP Investment Mistakes

Systematic Investment Plans (SIPs) are one of the most popular investment options in India, but many investors still make avoidable errors. Most people choose funds based on advice from friends, trending lists, or social media-without checking whether the fund matches their own goals, time horizon, or risk appetite. As a result, when markets fluctuate, they panic and stop their SIPs midway, losing out on the benefits of compounding and rupee-cost averaging. This behaviour reflects a lack of planning and discipline, making SIP-related errors one of the modern wealth management mistakes indians make, especially among new investors.

Here are the most common SIP investment mistakes:

- Selecting funds based on popularity instead of long-term suitability.

- Stopping SIPs during market corrections instead of staying invested.

- Investing without defining financial goals or timelines.

- Ignoring risk tolerance and choosing overly aggressive funds.

- Not reviewing SIP performance periodically.

- Investing random amounts instead of using a proper goal-based plan.

The solution is to take a structured, data-driven approach. Using a SIP planner app India can help map your goals-such as retirement, education, or home purchase-to the right fund categories and timeframes. It ensures disciplined investing and reduces emotional decision-making. Avoiding these errors prevents many wealth management mistakes indians make and helps SIPs truly work in your favour.

9. Rookie Investment Mistakes

First-time investors often enter the markets with excitement but very little preparation. Social media influencers, friends, or office colleagues frequently become the primary source of advice-leading many to invest in products they barely understand. Without proper research or knowledge of market behaviour, new investors tend to chase quick returns, buy at the wrong time, or panic when prices fall. These emotional decisions lead to losses, frustration, and a belief that investing is “too risky.” Such beginner errors continue to be among the most common wealth management mistakes indians make, especially in an age where information is abundant but not always reliable.

Here are the most frequent rookie investment mistakes:

- Buying stocks or funds just because they are trending.

- Following influencers blindly without verifying facts.

- Selling investments during market dips due to fear.

- Putting all money into one stock or theme without diversification.

- Starting investments without clarity on goals or timelines.

- Avoiding financial education, relying only on hearsay.

The best way to avoid these pitfalls is to begin with foundational learning. Platforms like Zerodha Varsity and ET Money School offer simple, structured lessons that build confidence and improve decision-making. Developing this knowledge early helps prevent several wealth management mistakes indians make and creates a strong base for long-term wealth creation.

10. Tech-Based Finance Mistakes

Technology has transformed the way Indians manage money, offering convenience, automation, and real-time insights. However, this rapid shift has also created new challenges. Many users blindly trust finance apps without understanding their terms, features, or security measures. Some rely solely on app recommendations without researching the underlying product. Others fail to verify whether the platform is regulated, secure, or offering unbiased guidance. These habits often lead to poor investment choices, privacy risks, and dependency on misleading dashboards. Ironically, in a world full of digital tools, misusing them has become one of the fastest-growing wealth management mistakes indians make, especially among younger, tech-driven investors.

Here are the most common tech-related finance mistakes:

- Blindly following app-generated investment suggestions.

- Sharing personal data on unverified platforms.

- Ignoring SEBI regulations when choosing investment apps.

- Taking loans from instant lending apps with hidden charges.

- Misinterpreting returns shown in dashboards or charts.

- Relying on automation without understanding the basics of money management.

To stay safe and informed, it’s crucial to use only verified, regulated apps. Always read user reviews, check security standards, and understand features before committing money. When technology is used wisely, it simplifies wealth management instead of complicating it. Adopting this cautious and informed approach helps prevent many wealth management mistakes indians make in the digital era.

The Rise of Digital Tools and Fintech in India

Fintech is democratizing financial literacy in India. From Tier 1 to Tier 3 cities, digital finance tools are empowering people to take control of their money.

Apps like INDmoney, Groww, Paytm Money, and Kuvera simplify everything from investments to tax planning. Robo-advisor India platforms now provide AI-powered financial guidance at scale. Debt management apps India like Cred or OneScore help monitor loans and credit.

Need a SIP planner app India? There are dozens that help align your mutual fund investments with your goals.

Want a budgeting app India? Apps like YNAB, Money View, and Spendee help organize income and expenses effortlessly.

These tools directly address the wealth management mistakes indians make, replacing confusion with clarity and action.

Using Technology to Fix Financial Mistakes

Here’s how digital finance tools help correct common money mistakes:

Overspending?

Solution: Use budgeting and expense tracking apps to control your cash flow.

Underinsured?

Solution: Get term insurance quotes online and compare with tools like PolicyBazaar.

Diversification Issues?

Solution: Use robo-advisors to auto-diversify your portfolio based on your risk profile.

ULIP Confusion?

Solution: Read comparisons and get unbiased advice on fintech platforms to avoid such wealth management mistakes indians make.

Tax Planning Problems?

Solution: Use fintech solutions to calculate exemptions and suggest the best deductions.

Fintech isn’t just a convenience-it’s a powerful antidote to the wealth management mistakes Indians make every day.

1. Use Budgeting Apps India

To manage lifestyle expenses and savings goals efficiently.

2. Avoid Rookie Mistakes

By following credible financial content and using learning platforms like Zerodha Varsity.

3. Choose the Best Robo Advisor Apps India

To automate and simplify your investments without needing a personal financial advisor.

4. Create Long-Term SIP Plans

With a SIP planner app India, millennials can start early, stay consistent, and build real wealth.

Indian millennials must break the cycle of wealth management mistakes indians make by choosing smarter tools early in life.

Introducing “My Wealth Locker” – Your Personal Wealth Storage and Maturity Tracker

Managing your wealth is about clarity, control, and confidence. That’s exactly what the My Wealth Locker app delivers.

What is it?

A secure, offline wealth management app that lets you store, track, and monitor all your personal wealth-without ever uploading to a server.

What You Can Store:

- Bank FDs & Post Office FDs

- Recurring Deposits

- Gold, Silver & Jewellery

- Real Estate

- NSC, NPS, Bonds & KVP

- Diamonds & Other Physical Assets

Key Features:

- Maturity Alerts: Never miss a maturity date again

- Offline Mode: No data ever leaves your phone

- Unified Dashboard: View all wealth types in one place

- Peace of Mind: Your wealth data stays with you

Download My Wealth Locker today and take the stress out of managing your personal wealth.

Conclusion

Avoiding the common wealth management mistakes indians make starts with awareness-but ends with action.

Today’s world offers you smarter, faster, and more secure tools to plan, invest, and grow. From budgeting apps to robo-advisors to comprehensive platforms like My Wealth Locker, Indians can now build a financial future with more clarity and less stress.

Don’t just earn. Don’t just save. Manage your wealth smartly.

Download My Wealth Locker today and take the first step toward eliminating the wealth management mistakes indians make.