Top Financial Goals to Set This Year for a Stronger, Smarter Money Future

Setting clear financial goals is the first step toward building a stronger and smarter money future. Many Indians struggle with inconsistent savings, rising expenses, and the pressure of managing family responsibilities. Whether you’re a young professional starting your career, a newly married couple managing joint finances, or someone trying to break free from debt, the right approach can transform your financial life. When you define what truly matters and set realistic targets, your money decisions become easier, more disciplined, and more aligned with your future dreams.

To help you get started, here are some practical steps you can take to create meaningful goals and stay committed to them:

- Identify your biggest money pain points such as overspending, debt, or low savings.

- Set short-term, mid-term, and long-term targets based on your lifestyle and income.

- Track your daily and monthly cash flow to understand where your money goes.

- Start small with habits like saving ₹50-₹100 a day or automating savings.

- Review and adjust your goals every 3-6 months to stay on track.

- Use apps or budgeting tools to maintain consistency.

- Celebrate small milestones to stay motivated and confident.

By approaching your journey with clarity and discipline, you can achieve your financial goals and build long-term stability for yourself and your family

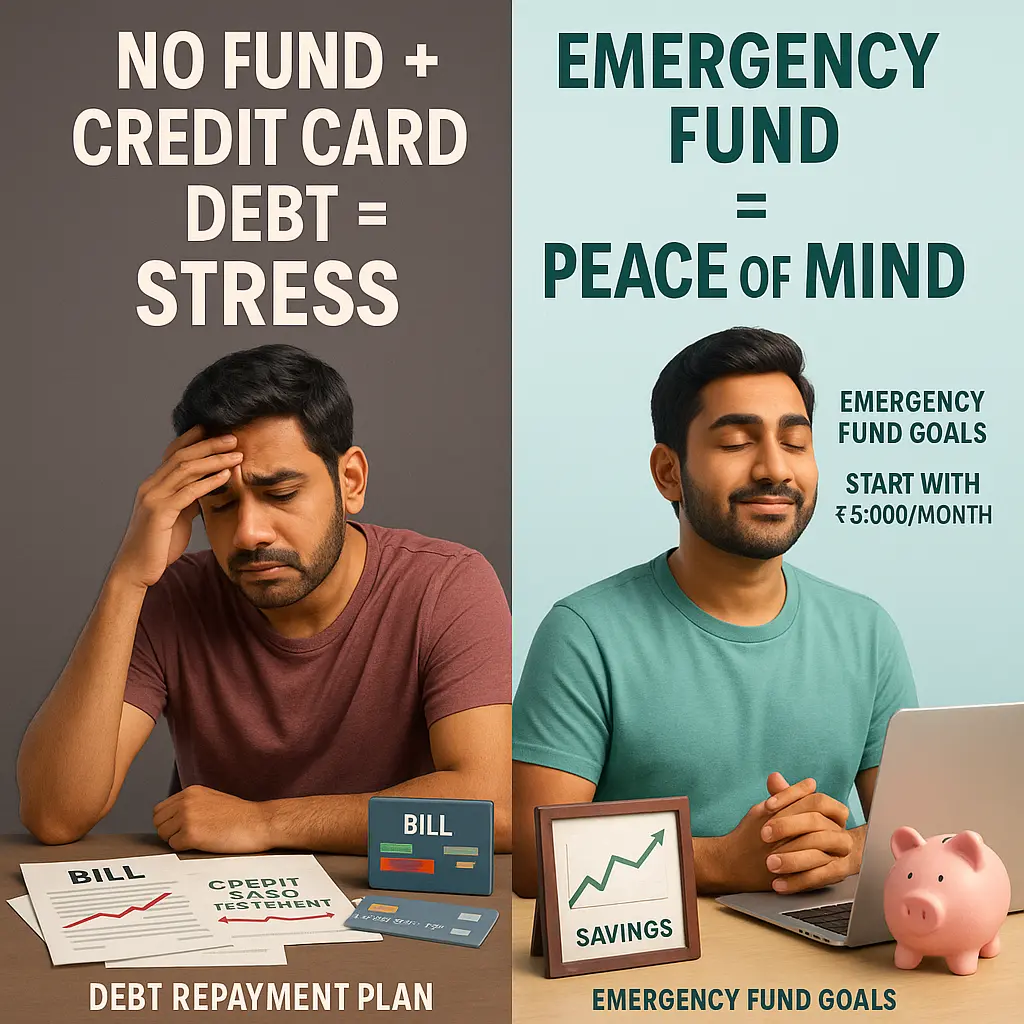

1. Build an Emergency Fund

Building an emergency fund is one of the most essential steps in strengthening your financial foundation. Unexpected moments such as medical bills, sudden job loss, or urgent home repairs can cause major stress if you’re not financially prepared. That’s why creating a dedicated safety cushion should be among your highest financial goals this year. In India, where many households depend on a single income source and healthcare costs continue to rise, having this buffer can make a huge difference in your peace of mind and stability.

Many people underestimate how quickly financial emergencies can derail long-term plans. A simple habit of setting aside a small amount every month can protect you from taking high-interest loans or relying on credit cards during tough times. The goal isn’t to save a large amount overnight-it’s about building consistency and discipline.

Here’s how you can make your emergency fund stronger and more reliable:

- Start by calculating your average monthly expenses.

- Save at least 3–6 months’ worth of essential costs.

- Keep the money in a liquid, easily accessible account.

- Automate monthly contributions to avoid skipping.

- Increase the amount whenever your income grows.

- Avoid using this fund unless it’s a real emergency.

By treating your emergency fund as a non-negotiable part of your financial goals, you protect yourself and your family from life’s uncertainties with confidence.

2. Clear High-Interest Debt

Clearing high-interest debt is a crucial step toward financial freedom and should be considered one of your top financial goals this year. Debt, especially from credit cards and personal loans, can act like a leaky bucket-no matter how much you earn, the interest keeps draining your money, leaving little for savings or investments. In India, credit card interest rates often range from 36% to 48% annually, making it financially toxic to carry balances month after month. Tackling debt early ensures that more of your hard-earned money works for you rather than against you.

Many Indians delay debt repayment, thinking they can manage minimum payments. However, this prolongs the burden and increases interest costs significantly. Adopting a structured repayment strategy helps you regain control, reduce financial stress, and free up funds for other priorities. Real-life examples, like Rahul, a Pune-based IT consultant who cleared his Rs. 1.2 lakh credit card debt using the snowball method, show that disciplined repayment can lead to long-term benefits.

Key steps to clear high-interest debt effectively:

- Prioritize paying off credit cards and personal loans first.

- Avoid minimum payments; aim to pay full amounts whenever possible.

- Use debt repayment calculators to plan and track progress.

- List debts from smallest to largest and consider the snowball method.

- Allocate extra income or bonuses toward debt repayment.

- Avoid accumulating new high-interest debt while paying off old balances.

Focusing on debt clearance as a financial goal helps secure a strong foundation for wealth-building and financial independence.

3. Start a SIP for Long-Term Wealth

Starting a Systematic Investment Plan (SIP) is one of the most effective ways to grow wealth over time and should be a key financial goal this year. SIPs allow you to invest a fixed amount regularly in mutual funds, harnessing the power of rupee cost averaging and compounding. This disciplined approach makes investing manageable, even for beginners, and reduces the impact of market volatility. In India, SIPs have gained immense popularity, with over 6 crore investors participating, highlighting their proven effectiveness in wealth creation.

Investing via SIPs is especially suitable for long-term goals like buying a house, funding children’s education, or planning for retirement. By starting early and staying consistent, your money can grow significantly over a decade or more. Real-life examples, like Ankit and Priya from Bengaluru, show that a modest monthly SIP of Rs. 7,000 can potentially accumulate over Rs. 15 lakhs in 10 years, demonstrating the power of consistent investing.

Key steps to start a successful SIP:

- Choose equity mutual funds for goals more than 5 years away.

- Start with an amount you can comfortably invest every month.

- Increase SIP contributions as your salary grows.

- Use SIP calculators to estimate future returns and plan better.

- Stay invested during market fluctuations; avoid stopping for short-term volatility.

- Review your SIP portfolio annually to ensure it aligns with your financial goals.

Making SIPs a part of your financial goals helps you build wealth steadily while keeping your long-term aspirations on track.

4. Set Short-Term and Long-Term Goals

Setting clear short-term and long-term financial goals is essential to bring focus and structure to your money management. By distinguishing between goals achievable within a few years and those requiring a decade or more, you can choose the right investment strategies and avoid unnecessary risks. Defining these timelines helps you prioritize your spending and saving, ensuring that urgent needs are met while long-term aspirations are steadily funded. This clarity is one of the most valuable financial goals to set this year, as it keeps your financial journey aligned with your personal and family priorities.

In India, many households juggle multiple responsibilities simultaneously-saving for a child’s education, planning for a wedding, or buying a new car. Without categorizing goals based on time horizons, it’s easy to misallocate funds, risking short-term liquidity or long-term growth. Real-life examples, like Akash from Hyderabad, highlight how splitting goals into short-term (a new car in 2 years) and long-term (daughter’s education in 15 years) helps in selecting the right investment vehicles and achieving targets efficiently.

Key steps to set effective short-term and long-term goals:

- Short-term goals (<3 years): use fixed deposits (FDs), recurring deposits (RDs), or PPF.

- Long-term goals (>5 years): invest in mutual funds, NPS, or diversified equity funds.

- Match each goal with the investment type that balances risk and returns.

- Review goals annually and adjust contributions based on changing income or priorities.

- Break large goals into smaller milestones to track progress.

- Maintain a separate fund for short-term liquidity needs.

Categorizing your objectives ensures your financial goals are realistic, actionable, and aligned with your life’s milestones.

5. Start Retirement Planning Early

Starting retirement planning early is one of the smartest steps you can take toward long-term financial security. While retirement may feel decades away, the power of compounding makes early investments significantly more impactful. Making retirement planning a priority ensures you maintain your lifestyle and independence in your golden years without relying solely on family support or government schemes. This is why saving for retirement is one of the most important financial goals to set this year.

In India, only about 12% of the working population has formal pension coverage, and many people rely solely on the Employees’ Provident Fund (EPF). While EPF is valuable, it may not be sufficient to meet future financial needs. Diversifying with instruments like the National Pension Scheme (NPS), pension-focused mutual funds, and retirement-oriented SIPs can help create a robust retirement corpus. Real-life examples, like Neha, a 30-year-old marketing executive, show that starting early with NPS contributions and retirement mutual fund SIPs can make a substantial difference over time.

Key steps for effective retirement planning:

- Start early with NPS to get tax benefits and long-term growth.

- Include pension mutual funds or ULIPs in your portfolio.

- Automate monthly contributions to stay consistent.

- Monitor and rebalance investments yearly to align with risk tolerance.

- Estimate retirement corpus based on lifestyle expectations.

- Increase contributions with salary hikes to maximize compounding.

By making retirement planning a core financial goal, you secure your future and enjoy peace of mind today.

6. Automate Monthly Savings and Investments

Automating your monthly savings and investments is one of the most effective ways to build consistent financial discipline. Many people struggle to save because life’s expenses come first, and relying on willpower alone often fails. By setting up automated transfers, you make saving and investing a priority, ensuring that your money works for you even when you’re busy or forgetful. This approach should definitely be one of your key financial goals to set this year, as it removes the guesswork and keeps your financial journey on track.

In India, while the average household saves around 30% of its income, a significant portion of these savings remain idle in savings accounts rather than being productively invested. Automation bridges this gap by directing funds toward investments like SIPs, recurring deposits (RDs), or gold savings, turning passive money into wealth-building capital. Real-life examples, like Dev from Delhi, show how small, structured allocations-Rs. 3,000 to SIP, Rs. 2,000 to RD, and Rs. 500 to gold-can steadily grow over time and build financial security.

Key steps to automate savings effectively:

- Set auto-transfers on your salary credit date.

- Prioritize savings before spending on discretionary expenses.

- Allocate funds to different goals (SIP, RD, gold) based on priorities.

- Use goal-tracking apps available in India to monitor progress.

- Adjust amounts annually based on income growth.

- Treat automated savings as non-negotiable monthly commitments.

Incorporating automation into your financial goals ensures discipline, consistency, and steady growth toward your long-term aspirations.

7. Diversify and Secure Your Assets

Diversifying and securing your assets is one of the smartest strategies to protect your wealth and should be a priority financial goal to set this year. Relying on a single asset class, whether equities, real estate, or gold, exposes you to unnecessary risk. Economic fluctuations, market volatility, or unexpected life events can quickly impact your finances if your investments are not well-balanced. By spreading your money across different asset types, you reduce risk and ensure that poor performance in one area does not derail your overall financial progress. Diversification also helps create a stable portfolio that can generate consistent returns over the long term.

In India, a balanced portfolio typically includes equities for growth, fixed income for stability, gold as an inflation hedge, and real estate for long-term wealth. Real-life examples, like Smita, a 40-year-old investor, demonstrate that combining corporate bonds, PPF, digital gold, and property investments allows her portfolio to remain resilient despite market swings.

Key steps to diversify and secure your assets:

- Mix equity, debt, gold, and fixed-income instruments.

- Track maturity dates, returns, and performance regularly.

- Avoid chasing high returns; focus on security and steady growth.

- Rebalance your portfolio annually to maintain target allocation.

- Include insurance and emergency funds for additional protection.

- Seek professional advice for complex or high-value portfolios.

Making asset diversification a central part of your financial goals ensures long-term stability while maximizing growth opportunities.

8. Save for Your Child’s Education

Saving for your child’s education is one of the most emotionally rewarding financial goals you can set this year. With education costs in India rising rapidly, parents who start early can significantly reduce financial stress in the future. Higher education, especially professional courses like MBAs or medical degrees, can cost anywhere between ₹10-25 lakhs, and inflation for education averages 10–12% annually. Planning ahead allows you to leverage the power of compounding and ensure your child’s aspirations are supported without compromising your family’s financial stability.

Investing systematically over time ensures that funds grow steadily and are available when your child reaches college age. Real-life examples, like Swati and Rajesh from Noida, illustrate the impact of disciplined investing. By putting aside ₹8,000 per month into a child education mutual fund when their son was just 2 years old, they expect to accumulate over ₹30 lakhs by the time he turns 18. Starting early not only makes large goals achievable but also reduces the need to take loans or incur high-interest debt later.

Key steps to save for your child’s education:

- Start investing early to maximize compounding benefits.

- Use SIPs, PPF, or Sukanya Samriddhi Yojana for structured savings.

- Track your goal progress using Indian goal-tracking apps.

- Review and adjust contributions annually based on inflation.

- Diversify investments to balance growth and safety.

- Treat this fund as non-negotiable to avoid withdrawals for other expenses.

By making your child’s education a core part of your financial goals, you ensure a secure, stress-free future for them while building disciplined saving habits.

9. Plan for Big Life Events (Wedding, Travel, Home)

Planning for big life events, such as weddings, international travel, or buying a home, is a critical part of achieving financial security and should be considered one of your key financial goals to set this year. These events often involve significant expenses, and without proper planning, many people resort to high-interest personal loans, creating financial stress and long-term debt. By defining your goals early and saving systematically, you can enjoy these milestones without compromising your financial stability.

In India, personal loans carry hefty EMIs and interest rates, making proactive planning essential. Allocating separate funds for each life event allows you to track progress, stay disciplined, and avoid mixing funds meant for different purposes. Real-life examples, like Mansi, a 27-year-old architect from Ahmedabad, show how effective goal-oriented planning works. She created separate savings plans for her Goa wedding and honeymoon, using short-term mutual funds and digital gold, successfully accumulating ₹5 lakhs in just two years. This approach ensures that life’s special moments are memorable without financial strain.

Key steps to plan for big life events:

- Break down large expenses into smaller, manageable milestones.

- Use recurring deposits (RDs), digital gold, and flexi mutual funds for targeted savings.

- Label separate accounts for each goal to avoid confusion.

- Automate monthly contributions to stay consistent.

- Track progress regularly and adjust amounts as needed.

- Avoid taking loans for planned events whenever possible.

Making big-event planning a part of your financial goals ensures you celebrate life’s milestones confidently and debt-free.

10. Build a Side Income Stream

Building a side income stream is one of the most effective ways to accelerate your financial progress and should be a key financial goal to set this year. Whether it’s freelancing, affiliate marketing, online tutoring, or any skill-based gig, additional income can help you pay off debt faster, increase investments, and reach other monetary objectives sooner. A side income also provides financial security by reducing dependence on a single salary and gives you more flexibility to pursue long-term goals.

In India, about one in four millennials actively look for side hustles to supplement their primary income. Real-life examples, like Kunal, a 32-year-old software engineer from Gurugram, show the practical benefits of this approach. By taking up freelance web development on weekends, Kunal earns an extra ₹15,000 per month, which he directs entirely toward his SIP. This disciplined strategy not only boosts his wealth accumulation but also ensures that the extra income contributes to meaningful financial goals rather than lifestyle inflation.

Key steps to build a successful side income stream:

- Identify marketable skills or hobbies that can generate income.

- Dedicate specific hours weekly to your side hustle.

- Channel all extra income toward financial goals instead of discretionary spending.

- Reinvest a portion to grow your side business or for long-term wealth.

- Track earnings and expenses separately for clarity.

- Continuously upgrade skills to increase earning potential.

Adding a side income stream strengthens your overall financial foundation while helping you achieve goals faster and more confidently.

11. Insure Yourself and Your Family

Insuring yourself and your family is a fundamental step in securing financial stability and should be a top financial goal to set this year. Life is unpredictable, and without adequate protection, medical emergencies, accidents, or the loss of an earning member can derail even the best-laid financial plans. Adequate life and health insurance ensures that you and your loved ones are financially safeguarded while allowing your investments and savings to continue growing uninterrupted.

In India, medical emergencies are the leading cause of financial distress among middle-class households. Many families find themselves taking loans or dipping into savings when faced with large hospital bills. Real-life examples, like Saurabh and Meena from Bhopal, illustrate the importance of timely insurance decisions. After witnessing a friend’s ICU expenses wipe out their savings, the couple purchased a ₹1 crore term life insurance plan and a ₹10 lakh family floater health plan, providing both security and peace of mind.

Key steps to insure yourself and your family effectively:

- Get term life insurance equal to 10-15 times your annual income.

- Ensure all family members have individual or family health coverage.

- Avoid mixing insurance and investment; skip endowment or ULIP plans for pure protection.

- Review coverage periodically and increase it as your income or liabilities grow.

- Compare policies from trusted insurers to get the best value.

- Keep all policy documents and nominations updated for easy claims.

Making insurance a priority in your financial goals protects your family and preserves your wealth, no matter what life throws your way.

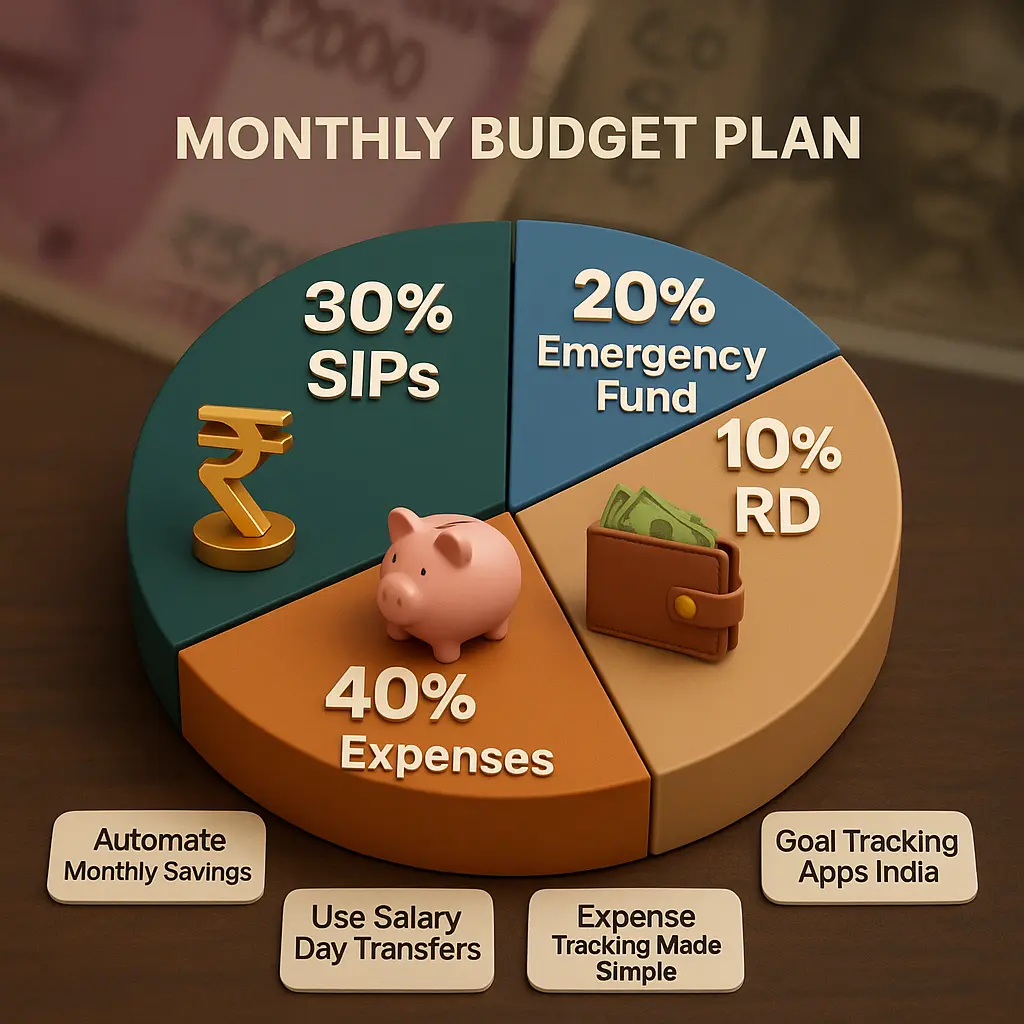

12. Create a Monthly Budget and Stick to It

Creating a monthly budget and sticking to it is the foundation of a strong financial plan and one of the most practical financial goals to set this year. Without a clear budget, it’s easy to overspend, accumulate debt, or neglect savings. A well-structured monthly plan allows you to allocate funds for essential expenses, discretionary spending, and investments, giving you control over your finances and enabling you to achieve your long-term financial objectives.

In India, despite the benefits of budgeting, many households do not follow structured plans, leading to unnecessary debt and missed opportunities for saving. Real-life examples, like Tanya from Chennai, demonstrate the impact of disciplined budgeting. By following the 50/30/20 method-50% for needs, 30% for wants, and 20% for savings-she managed to pay off ₹75,000 of debt in just eight months while still enjoying her lifestyle. This shows that budgeting is not about restriction but about prioritizing what matters most.

Key steps to create and maintain a monthly budget:

- Track all income and expenses using apps or Excel sheets.

- Categorize spending into needs, wants, and savings.

- Allocate funds for debt repayment, emergency savings, and investments.

- Review and adjust the budget monthly based on actual spending.

- Reward yourself for meeting targets to stay motivated.

- Stick to the plan consistently to achieve both short-term and long-term goals.

By making a monthly budget a central part of your financial goals, you gain control, reduce financial stress, and build a disciplined path toward wealth and stability.

Introducing: My Wealth Locker

Managing all your wealth data across banks, investments, and properties is stressful. That’s why My Wealth Locker exists.

What it does:

- A personal wealth storage and maturity tracking tool for all your assets

You can store:

- Bank FDs, Post Office FDs, RDs

- Gold, silver, diamond, jewellery

- Real estate, NSC, NPS, bonds

Key features:

- Single dashboard to view and manage everything

- Maturity reminders so you never miss returns

- Zero server/cloud access-your data stays on your device

- Helps you track your financial goals to set this year effortlessly

Why people love it:

- Peace of mind knowing everything is in one place

- Never miss out on maturing investments

- Simple, clutter-free design

Final Words: You Can Do This

Setting financial goals to set this year isn’t about perfection-it’s about progress. Each step you take today makes tomorrow easier. Whether you’re starting small or planning big, what matters is that you begin.

Your turn: Download My Wealth Locker to organize your wealth goals.

Let’s build your financial future-one smart goal at a time.