1. Introduction

Kisan Vikas Patra occupies a distinct position in India’s savings ecosystem as a sovereign-backed, fixed-return instrument designed to preserve capital and deliver predictable growth. For Indian professionals, small business owners, and conservative wealth planners, KVP represents a financial tool that prioritizes certainty over speculation, especially in an environment marked by market volatility, interest rate cycles, and evolving tax regimes.

While modern portfolios increasingly include equity, mutual funds, and pension-linked products, government-backed savings schemes continue to play a foundational role in risk management and capital efficiency. KVP, in particular, remains relevant not as a high-return product but as a stability anchor within a diversified long-term financial strategy.

1.1 The Role of Government-Backed Savings Schemes in Capital Preservation

Government-backed savings schemes in India are designed with a primary objective: protecting principal while ensuring modest, predictable growth. Instruments such as KVP, NSC, PPF, and government savings bonds are underwritten by the sovereign, making them virtually immune to default risk. For risk-averse investors and institutions managing surplus funds, this assurance is a critical decision factor.

From a financial planning standpoint, these schemes reduce dependency on market timing and behavioral discipline. They allow investors to lock in returns, simplify forecasting, and safeguard capital earmarked for medium- to long-term goals without exposure to equity or credit market fluctuations.

Why businesses and individuals prefer sovereign-backed instruments:

- Near-zero default risk due to the Government of India backing

- Predictable returns that simplify cash-flow and goal planning

- Immunity from market volatility and corporate credit events

- Strong alignment with capital protection and contingency reserves

- Ease of understanding and minimal operational complexity

1.2 Where KVP Fits in India’s Evolving Wealth-Planning Landscape

Despite the rapid growth of market-linked instruments such as mutual funds, ETFs, and the National Pension System (NPS), KVP continues to retain relevance as a non-correlated, fixed-income component. Its value lies not in outperforming markets, but in providing certainty, discipline, and structural balance to a portfolio increasingly exposed to volatility.

For Indian professionals managing multiple financial goals-such as education funding, capital reserves, or legacy planning-KVP functions as a low-maintenance asset. When combined with modern digital tracking tools like My Wealth Locker, investors can improve productivity by monitoring KVP certificates, maturity timelines, and reinvestment schedules alongside other government-backed instruments, without increasing administrative burden.

Strategic positioning of KVP in modern portfolios:

- Acts as a stabilizer against equity and market-linked volatility

- Suitable for goal-based allocations with fixed time horizons

- Complements NPS and equity by strengthening downside protection

- Enhances financial discipline through lock-in and fixed maturity

2. What Is Kisan Vikas Patra ? A Clear Definition

Kisan Vikas Patra is a government-backed, fixed-return savings certificate designed to encourage disciplined long-term savings while protecting invested capital. Unlike market-linked products, KVP operates on a predetermined interest framework, making outcomes measurable and predictable at the time of investment. Its simplicity, sovereign assurance, and fixed maturity value have made it a longstanding choice among conservative Indian investors.

From a wealth-planning perspective, KVP is best understood not as a growth accelerator, but as a capital efficiency tool-one that converts idle or surplus funds into guaranteed future value with minimal monitoring, compliance, or behavioral risk. Tools like My Wealth Locker eliminate the risk of forgotten certificates and missed maturities by centralizing all government savings records.

2.1 Historical Background and Policy Objective of KVP

KVP was introduced by the Government of India in 1988 as part of a broader policy effort to mobilize household savings and redirect them into formal financial channels. The scheme was originally targeted at rural and semi-urban populations, where access to banking and structured investment products was limited, and informal savings dominated.

Over time, KVP evolved into a mainstream savings instrument. While its investor base expanded beyond its original demographic, the underlying policy objective remained unchanged: encourage long-term savings through capital certainty and government backing, without linking returns to market performance.

Core policy intent behind KVP:

- Promote a long-term savings culture across income groups

- Channel household savings into secure, government-supported instruments

- Offer guaranteed capital growth without market or credit risk

2.2 Who Issues KVP and How It Is Regulated

KVP is issued by the Government of India through designated post offices and authorized public-sector banking channels. The scheme operates under the administrative control of the Ministry of Finance, with interest rates and terms notified periodically through official government circulars.

The regulatory framework ensures uniformity, transparency, and investor protection. Interest rates, lock-in conditions, and redemption rules are standardized nationwide, eliminating issuer-specific risk and discretionary variation.

Governance and regulatory oversight:

- Issued under the authority of the Government of India

- Administered via India Post and authorized financial institutions

- Interest rates and terms notified by the Ministry of Finance

2.3 Common Misconceptions About KVP Among Retail Investors

Despite its long history, KVP is often misunderstood, leading to either overestimation or underutilization in personal finance strategies. Many retail investors confuse KVP with tax-saving products or assume it offers liquidity and flexibility similar to bank fixed deposits, which can distort expectations.

A clear understanding of what KVP is and is not is essential for using it effectively within a broader wealth plan, particularly when managing multiple instruments and long-term goals.

Common misconceptions and clarifications:

- KVP is not a tax-saving instrument under Section 80C

- Returns are fixed, but interest is fully taxable

- KVP is not market-linked and does not benefit from equity upswings

- Liquidity is limited due to a mandatory lock-in period

- KVP is a savings certificate, not a recurring income product

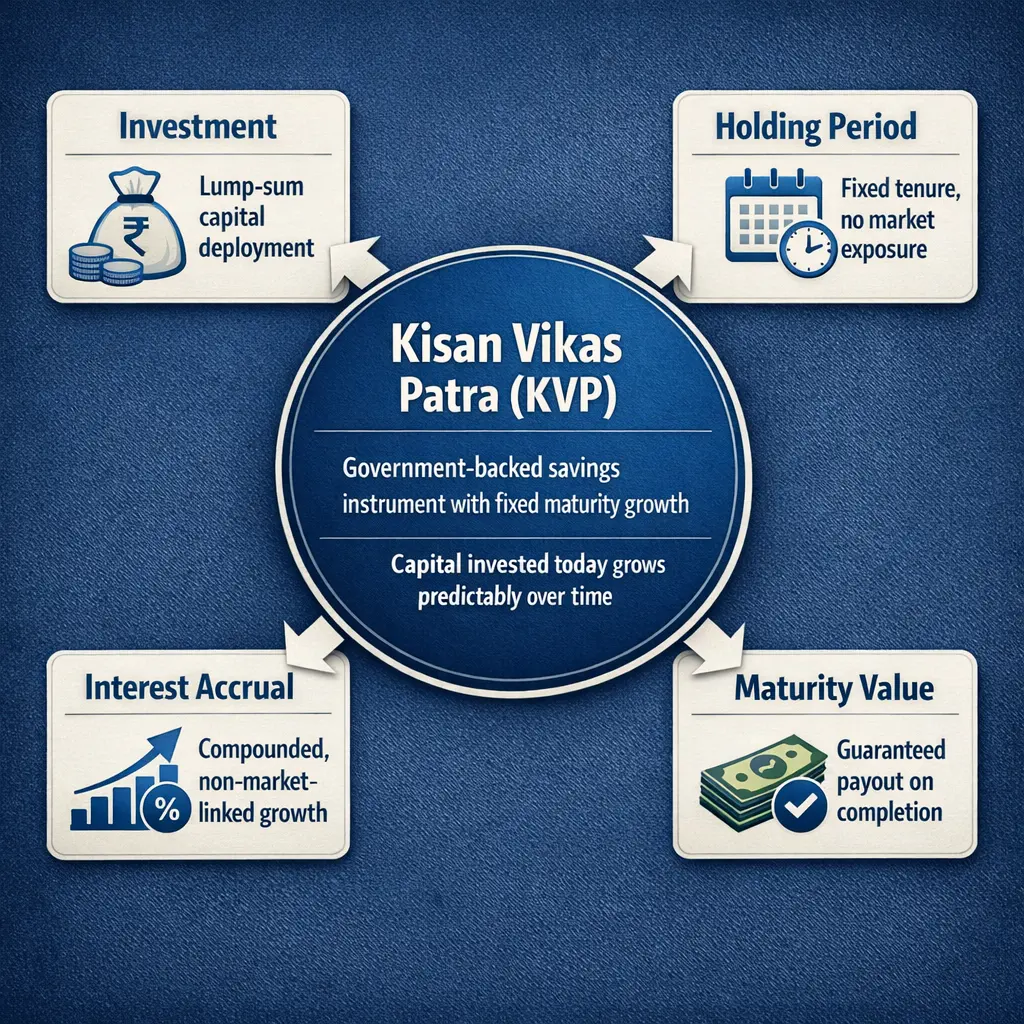

3. How KVP Works: Structure, Mechanics, and Growth Formula

Kisan Vikas Patra (KVP) operates as a certificate-based, fixed-return savings instrument that allows investors to lock in capital for a predetermined period while earning guaranteed growth. Its appeal lies in simplicity and predictability: the amount invested grows at a fixed interest rate until maturity, at which point the principal plus interest is fully repayable. Understanding the mechanics of purchase, holding, and redemption is essential for aligning KVP with broader wealth-planning objectives.

For long-term investors, Kisan Vikas Patra can serve as a capital preservation tool, providing a measurable outcome without exposure to market volatility. When integrated with modern tracking solutions like My Wealth Locker, investors can efficiently monitor maturity timelines, reinvestment schedules, and overall portfolio alignment, reducing administrative overhead.

3.1 Investment Process: Purchase, Holding, and Maturity

Investing in KVP begins with purchasing certificates through authorized channels, primarily post offices or select public-sector banks. The process is straightforward and does not require complex documentation beyond proof of identity and address. Once purchased, certificates are held until maturity, where the accumulated value can be redeemed in full.

The maturity value is calculated based on the prevailing interest rate at the time of purchase, and the investment doubles over a fixed period, offering a clear target for investors. The scheme requires disciplined holding, as premature withdrawal is allowed only under specified conditions after a mandatory lock-in period.

Key steps in the KVP investment process:

- Visit an authorized post office or public-sector bank branch to purchase certificates

- Submit KYC documents including identity and address proof

- Choose investment denomination based on personal financial goals

- Receive a physical certificate with unique serial number for tracking

- Hold the certificate until maturity to realize guaranteed growth

- Redeem at maturity, receiving principal plus accrued interest

3.2 Certificate-Based Ownership and Nomination Rules

KVP is a certificate-driven instrument, meaning ownership is evidenced by the physical certificate itself. Each certificate carries a unique number and purchase details, ensuring legal clarity and ease of transfer or redemption. Investors can also nominate individuals to receive proceeds in the event of death, enhancing succession planning and asset protection.

Ownership and nomination essentials:

- Certificates must be kept secure, as ownership is tied to the physical document

- Nomination of one or more beneficiaries is allowed

- Joint ownership is permitted in specific cases, including for minors

- Transfers between accounts or family members are regulated and require authorization

3.3 How KVP Doubles Your Money: Compounding Logic Explained Simply

The growth of KVP relies on a fixed, compounding interest mechanism where the invested capital accrues interest at pre-defined intervals. Unlike market-linked products, the compounding schedule and maturity timeline are predetermined, allowing investors to project returns with certainty. This predictability makes KVP an ideal tool for goal-based planning, such as saving for medium-term financial objectives or building a secure reserve.

Compounding in KVP is cumulative: interest earned over successive periods is reinvested into the principal, effectively accelerating growth without requiring additional contributions. By leveraging the doubling timeline, investors can map future cash flows and align them with personal or business financial targets.

Key points about KVP compounding:

- Interest compounds at fixed intervals, increasing total maturity value

- Growth is predictable, enabling disciplined financial planning

- Reinvestment occurs automatically within the certificate until maturity

4. KVP Interest Rate Explained: Returns, Compounding, and Predictability

Kisan Vikas Patra offers a fixed interest rate determined by the Government of India, ensuring predictable returns over the investment horizon. The rate is periodically revised and notified by the Ministry of Finance, reflecting broader economic conditions, inflation trends, and small savings rate policies. For long-term investors, the certainty of returns allows for precise financial planning, particularly when combining KVP with other government-backed instruments.

Integrating tools like My Wealth Locker can help investors track interest accruals, monitor maturity timelines, and align KVP holdings with overall portfolio targets without manual computation.

4.1 Current KVP Interest Rate and Revision Cycle

The current KVP interest rate is set by the Government and typically revised every quarter to align with prevailing economic conditions. Investors benefit from a transparent mechanism that communicates changes through official notifications, ensuring clarity and consistency.

Key points regarding the current interest rate:

- Fixed at the time of investment, affecting the maturity timeline

- Revisions are notified quarterly by the Ministry of Finance

- Rates are standardized across all post offices and authorized banks

4.2 Historical Interest Rate Trends and Stability

Historically, KVP has maintained a stable and predictable interest profile, though minor fluctuations have occurred in response to macroeconomic policy shifts. Over the past decade, the scheme has demonstrated resilience against market volatility, making it a reliable component for conservative portfolios.

Key points on historical trends:

- Rates adjusted periodically but remained within a narrow band

- Provides a consistent doubling timeline for invested capital

- Helps investors plan medium- to long-term goals without uncertainty

4.3 Illustrative Maturity Value Calculations

To visualize the financial impact of Kisan Vikas Patra, consider a scenario where an investor purchases certificates at the prevailing interest rate. The maturity value is fixed and predictable, allowing for goal-oriented planning and capital allocation decisions. This approach eliminates guesswork while providing clarity on expected returns.

Example: Investment Amount vs Maturity Value

| Investment Amount (INR) | Doubling Period (Years) | Maturity Value (INR) |

|---|---|---|

| 10,000 | 8.5 | 20,000 |

| 25,000 | 8.5 | 50,000 |

| 50,000 | 8.5 | 1,00,000 |

| 1,00,000 | 8.5 | 2,00,000 |

This table illustrates the predictable doubling feature of Kisan Vikas Patra, demonstrating its utility for capital preservation, strategic wealth planning, and systematic reinvestment decisions.

5. Lock-In Period and Liquidity: When and How You Can Exit KVP

Kisan Vikas Patra is designed to encourage disciplined, long-term saving by enforcing a mandatory holding period. This lock-in ensures that investors cannot withdraw funds immediately after purchase, preserving the capital for the intended growth period and reinforcing financial planning discipline. Understanding the lock-in, withdrawal options, and relative liquidity is essential for aligning KVP with broader wealth-management objectives.

5.1 Mandatory Lock-In Period and Rationale

The Kisan Vikas Patra certificate comes with a minimum lock-in period of 2 years and 6 months from the date of purchase. This duration is structured to allow the invested amount to accrue interest and reach the predefined doubling timeline efficiently. The rationale behind this lock-in is both policy-driven and investor-focused, promoting long-term savings behavior while preventing premature cash-outs that could undermine the compounding benefit.

Key points on lock-in period:

- Lock-in duration ensures the full benefit of compounding interest

- Protects investors from the temptation of early withdrawal

- Reinforces KVP’s role as a capital preservation and goal-based savings tool

5.2 Premature Withdrawal Rules

Although Kisan Vikas Patra is intended for long-term holding, the government allows premature encashment under specific conditions, primarily to address emergencies. Withdrawals before the minimum maturity period are subject to restrictions and are calculated according to the prevailing interest rates at the time of encashment.

Premature withdrawal guidelines:

- Allowed only after 2 years and 6 months from the purchase date

- Withdrawal before maturity results in reduced interest payout

- Certificates can be encashed at the issuing post office or bank branch

- Nominees can claim the proceeds in case of the investor’s demise

- Proper KYC and certificate presentation are mandatory for withdrawal

5.3 Liquidity Comparison with FD and Small Savings

While Kisan Vikas Patra provides capital safety and predictable growth, its liquidity is more restricted than bank FDs or some other small savings schemes. Investors need to plan redemptions carefully, considering the lock-in and maturity timelines. However, compared to long-term pension instruments, KVP remains moderately flexible for structured financial planning.

Liquidity insights:

- Fixed Deposits allow partial or full premature withdrawal, often with interest penalty

- NSC and PPF have longer lock-in periods or partial withdrawal restrictions

- Kisan Vikas Patra requires physical certificate presentation for encashment

- Despite limited liquidity, maturity timelines are predictable for cash-flow planning

6. Taxation of KVP: What Investors Must Know

Kisan Vikas Patra provides guaranteed returns, but the interest earned is fully taxable under Indian law, unlike some other small savings instruments such as PPF. Understanding taxation is critical for professional investors and long-term planners, as it affects post-tax returns and informs capital allocation decisions. Proper planning ensures that KVP remains an efficient tool for predictable growth without unintended tax consequences.

6.1 Tax Treatment of Interest Earned

Interest on Kisan Vikas Patra accrues cumulatively until maturity and is treated as income from other sources under the Income Tax Act. It is fully taxable in the financial year in which the certificate is encashed or matures. Professional investors often integrate tax projections into their KVP planning to assess net effective returns.

Key points:

- Interest is added to total taxable income at maturity

- No exemption under Section 80C or other tax-saving provisions

- Investors should consider post-tax yield when allocating capital

6.2 Taxability at Maturity

At maturity, the principal plus accumulated interest is payable in full. The interest portion is treated as taxable income, while the principal remains tax-free. For long-term financial planning, understanding this distinction is essential for projecting net cash flows and reinvestment strategies.

Key points:

- Principal is tax-free, only interest is taxable

- Maturity proceeds are reported as “Income from Other Sources” in ITR

- No TDS is deducted at maturity unless specified by government rules

6.3 TDS and ITR Reporting

While KVP interest is taxable, TDS is generally not deducted at source on post office KVP encashment. However, investors must report interest income in their Income Tax Return (ITR) to comply with regulations and avoid penalties. Using tools like My Wealth Locker can streamline tracking of interest accruals and ensure timely reporting across multiple Kisan Vikas Patra certificates and other government-backed instruments.

Tax treatment summary:

| Stage of Investment | Tax Implication | Reporting Requirement |

|---|---|---|

| At Purchase | No tax applicable | Not reported |

| During Holding (Interest Accrual) | Interest accumulates cumulatively | Not reported annually; tracked for planning |

| At Maturity/Encashment | Interest fully taxable | Report as “Income from Other Sources” in ITR |

This table clarifies the stages of taxation, helping investors forecast post-tax returns and integrate KVP efficiently into long-term wealth planning.

7. Eligibility and Investment Limits for KVP

Kisan Vikas Patra (KVP) is designed to be widely accessible, making it suitable for individual investors, joint holders, and even minors. Understanding eligibility criteria and investment thresholds is critical for compliance, goal planning, and portfolio structuring. These rules ensure that KVP remains a secure, standardized instrument while providing flexibility for diverse financial circumstances.

7.1 Who Can Invest in KVP (Resident Status, Age Criteria)

KVP is available to resident Indian citizens and select non-resident investors through designated channels. Individuals, joint holders, and guardians on behalf of minors can participate, making it a versatile option for personal and family wealth planning.

Eligibility highlights:

- Open to resident Indian citizens above 18 years of age

- Joint investments permitted for spouses and minors via guardians

- Investors must provide valid KYC documents at the time of purchase

7.2 Minimum and Maximum Investment Thresholds

Kisan Vikas Patra investment denominations are standardized to promote accessibility while allowing meaningful capital deployment. The flexibility in investment amounts enables alignment with individual goals and risk profiles, from small savings to medium-term capital accumulation.

Investment limit details:

- Minimum investment starts at INR 1,000 per certificate

- No strict maximum per individual, though cumulative limits may apply in practice

- Certificates are available in multiple denominations to suit financial planning

- Investors can purchase multiple certificates for staggered maturity and goal alignment

7.3 Joint Holding, Minor Investment, and Nomination Norms

Kisan Vikas Patra allows joint holdings and minor account investment, which is useful for family wealth planning and succession management. Nomination is mandatory to ensure smooth transfer of proceeds in case of unforeseen events, enhancing security and administrative clarity.

Key norms:

- Joint holders can include spouses or guardians for minor investments

- Minors can invest through legal guardians until reaching majority

- Nomination is mandatory and can include multiple beneficiaries

- Certificates remain legally binding and transferable within regulatory limits

8. Risk Profile of KVP: Capital Safety and Inflation Considerations

Kisan Vikas Patra (KVP) is inherently a low-risk investment vehicle, backed by the Government of India. Its primary appeal lies in capital protection and predictable returns rather than market-beating performance. For professionals and long-term planners, understanding its risk characteristics-sovereign safety, inflation impact, and interest rate exposure-is crucial for strategic portfolio allocation.

8.1 Sovereign Backing and Default Risk Assessment

Kisan Vikas Patra is fully sovereign-backed, which effectively eliminates default risk. Unlike corporate bonds or market-linked instruments, the government guarantees the principal and interest, making KVP suitable for risk-averse investors. This stability supports financial planning for critical goals without exposure to credit events.

Key points on sovereign safety:

- Principal and accrued interest guaranteed by the Government of India

- No credit or corporate default risk

- Suitable as a foundational, low-volatility asset in diversified portfolios

8.2 Inflation Risk and Real Return Analysis

While Kisan Vikas Patra offers nominally predictable returns, inflation can erode real purchasing power over its 8–10 year doubling period. Long-term planners should evaluate KVP as part of a balanced strategy, combining it with inflation-hedged instruments to maintain real growth of wealth.

Considerations regarding inflation:

- Fixed interest may underperform during high-inflation periods

- Real returns may be lower than nominal yields, affecting goal-based outcomes

- Suitable for capital preservation rather than aggressive wealth creation

8.3 Interest Rate Risk Versus Market-Linked Instruments

KVP carries minimal interest rate risk for investors holding to maturity, as returns are fixed. However, opportunity cost arises if prevailing market rates increase after purchase. Unlike market-linked instruments, KVP does not adjust to interest rate cycles, emphasizing the importance of planning entry timing.

Interest rate insights:

- Returns remain fixed regardless of future rate fluctuations

- Opportunity cost exists if alternate high-yield instruments emerge

- Best suited for investors prioritizing certainty over maximizing yield

9. Who Should Invest in KVP? Suitability Analysis by Investor Profile

Kisan Vikas Patra (KVP) is best suited for investors seeking predictable, low-risk capital growth within a structured time horizon. Its fixed returns and government backing make it an ideal option for professionals, conservative savers, and those managing family wealth or contingency funds. Understanding the suitability helps integrate KVP strategically into a broader portfolio without overexposing to opportunity cost.

9.1 Ideal Use Cases: Conservative Investors and Capital Protection Goals

Kisan Vikas Patra aligns with objectives where capital preservation and guaranteed returns outweigh the desire for high growth. Professionals and business owners can use it to secure medium-term funds while maintaining a disciplined savings routine.

Advisory points for ideal use:

- Investors with low tolerance for market volatility

- Those prioritizing principal protection over maximum returns

- Professionals saving for predictable cash-flow needs

- Individuals building an emergency or contingency fund

- Retirees or pre-retirees seeking secure, fixed-income assets

9.2 KVP for Short- to Medium-Term Financial Objectives

Kisan Vikas Patra can serve as a goal-based instrument for objectives within an 8-10 year horizon, such as children’s education, down payments, or personal projects. Its doubling feature provides clarity on expected proceeds, allowing disciplined planning.

Practical considerations for medium-term goals:

- Suitable for horizon-aligned investments of 5-10 years

- Predictable maturity value simplifies budgeting and allocation

- Complements fixed deposits and NSC for layered goal planning

- Can be staggered to align multiple goal timelines

- Reduces behavioral risk associated with market-linked instruments

9.3 When KVP May Not Be the Right Choice

While Kisan Vikas Patra offers security, it is less effective for aggressive wealth creation or inflation-beating objectives. Investors seeking high returns or immediate liquidity may find alternative instruments more suitable.

Advisory points on limitations:

- Not ideal for short-term liquidity needs (<2.5 years)

- Fixed returns may underperform inflation over long periods

- Does not benefit from equity or market-linked growth

- Opportunity cost exists if higher-yield instruments are available

- Less suitable for tax-efficient portfolios due to taxable interest

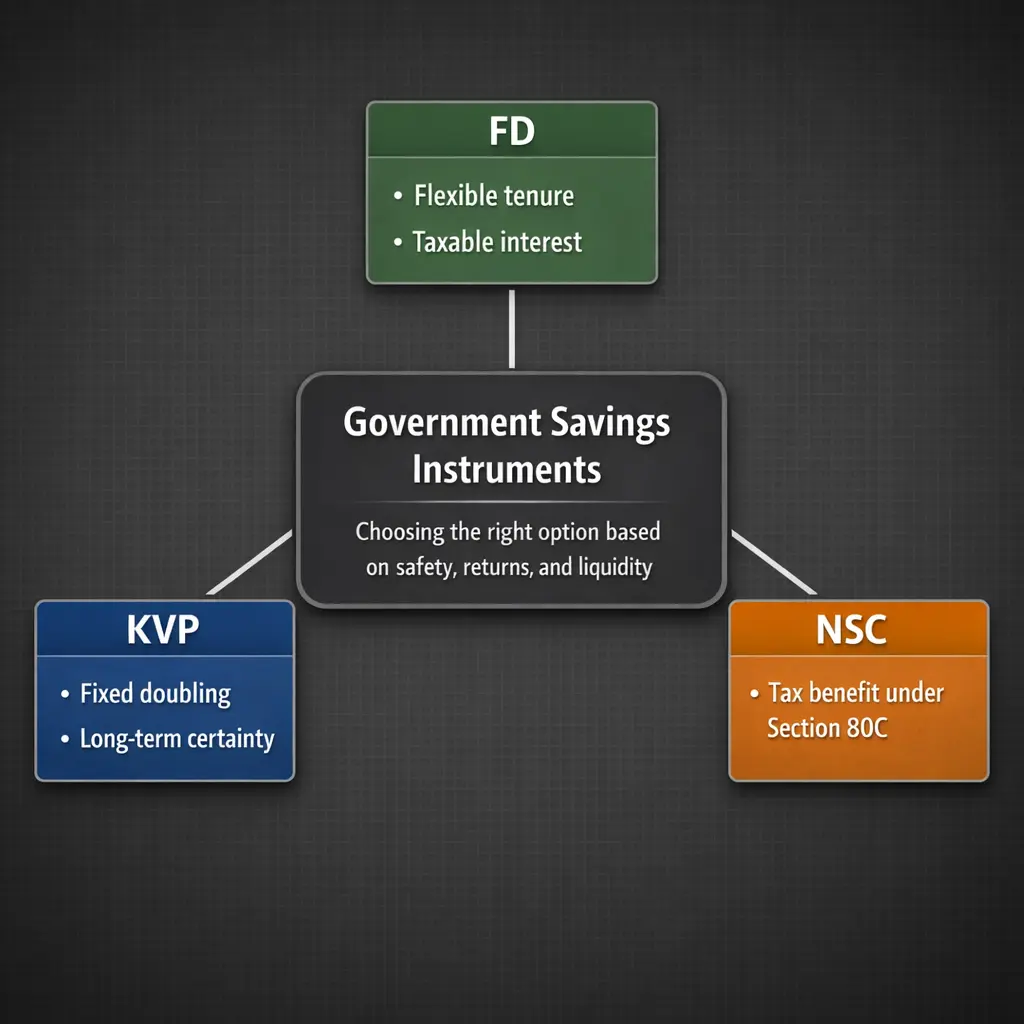

10. KVP vs Fixed Deposit (FD): Safety, Returns, and Flexibility

Kisan Vikas Patra and bank Fixed Deposits (FDs) are both conservative savings instruments, but they differ in interest structure, liquidity, and risk exposure. Understanding these differences helps professionals and long-term planners choose the right instrument for specific financial goals while balancing capital protection and predictability.

10.1 Interest Rate and Return Predictability

Kisan Vikas Patra offers fixed, government-backed returns, while FDs provide bank-determined interest that may vary based on tenure, deposit amount, and market rates. KVP guarantees a doubling period, whereas FD returns compound monthly, quarterly, or annually depending on the bank’s terms.

10.2 Liquidity, Lock-In, and Premature Exit Differences

FDs are generally more flexible, allowing partial or full withdrawals before maturity with an interest penalty. Kisan Vikas Patra requires a mandatory lock-in of 2 years and 6 months, with premature withdrawal subject to government rules. This makes KVP less liquid but more structured for disciplined savings.

10.3 Tax Efficiency and Post-Tax Return Comparison

FD interest is fully taxable and subject to TDS if it exceeds the threshold, while Kisan Vikas Patra interest is also taxable but TDS may not be applied automatically. Effective post-tax yield can differ, particularly for higher-income investors, and should inform portfolio allocation.

Comparison Table: KVP vs FD

| Feature | Kisan Vikas Patra | Fixed Deposit (FD) |

|---|---|---|

| Issuer | Government of India | Banks (Public or Private) |

| Interest Rate | Fixed, government-determined | Fixed, bank-determined |

| Compounding | Predetermined doubling period | Monthly, quarterly, or annual |

| Lock-In Period | 2 years 6 months minimum | Flexible, based on chosen tenure |

| Premature Withdrawal | Allowed after lock-in with interest adjustment | Allowed with penalty |

| Tax Treatment | Interest fully taxable, TDS may not apply | Interest fully taxable, subject to TDS |

| Risk | Sovereign-backed, very low risk | Low risk, bank-dependent |

Key Takeaways from Comparison:

- KVP provides guaranteed, government-backed returns, while FD returns depend on banking sector rates

- FDs offer higher liquidity, making them preferable for short-term needs or emergency funds

- Tax efficiency is similar, but TDS on FD interest may require additional compliance

- KVP’s structured doubling makes it suitable for goal-based planning, whereas FDs offer flexible compounding options

- Professionals can combine both instruments to balance predictability, flexibility, and risk

11. KVP vs National Savings Certificate (NSC): Which Is Better for You?

KVP and NSC are both government-backed, low-risk savings instruments, but they serve slightly different purposes in a wealth-planning strategy. While KVP focuses on predictable doubling of capital, NSC is primarily a tax-saving vehicle under Section 80C that also provides cumulative interest over a fixed tenure. Comparing these two instruments helps investors optimize their portfolios for risk, return, and tax efficiency.

11.1 Investment Horizon and Compounding Structure

Kisan Vikas Patra offers a predetermined doubling period, making it predictable for medium-term financial goals. NSC typically has a 5-year maturity period with compound interest credited annually, which makes it suitable for structured savings aligned with tax planning.

Key points on horizon and compounding:

- Kisan Vikas Patra doubling period is fixed and easy to project

- NSC compounds annually, allowing interest to add to principal for reinvestment

- Both are suitable for medium-term goals, but KVP provides more clarity on final proceeds

- Investors can ladder NSC and KVP to match multiple goal timelines

11.2 Tax Benefits under Section 80C: NSC vs KVP

NSC provides tax benefits under Section 80C, allowing investors to reduce taxable income while saving. KVP, in contrast, does not offer tax exemptions, though interest is deferred until maturity, which may help with tax planning through timing.

Tax considerations:

- NSC principal qualifies for deduction under Section 80C

- Kisan Vikas Patra offers no immediate tax benefit on investment amount

- Interest earned in both instruments is fully taxable at maturity

- Professionals can combine NSC and KVP to optimize tax and capital growth strategies

11.3 Goal-Based Suitability Comparison

KVP is more suitable for investors prioritizing guaranteed capital growth, whereas NSC suits those who want tax-efficient, medium-term savings. Evaluating investment objectives, risk tolerance, and liquidity needs helps determine which instrument to prioritize.

Suitability insights:

- KVP ideal for capital preservation and predictable doubling

- NSC ideal for maximizing Section 80C benefits while earning stable returns

- KVP better for straightforward goal-based planning without tax dependency

- Combining both instruments can provide stability, tax efficiency, and portfolio diversification

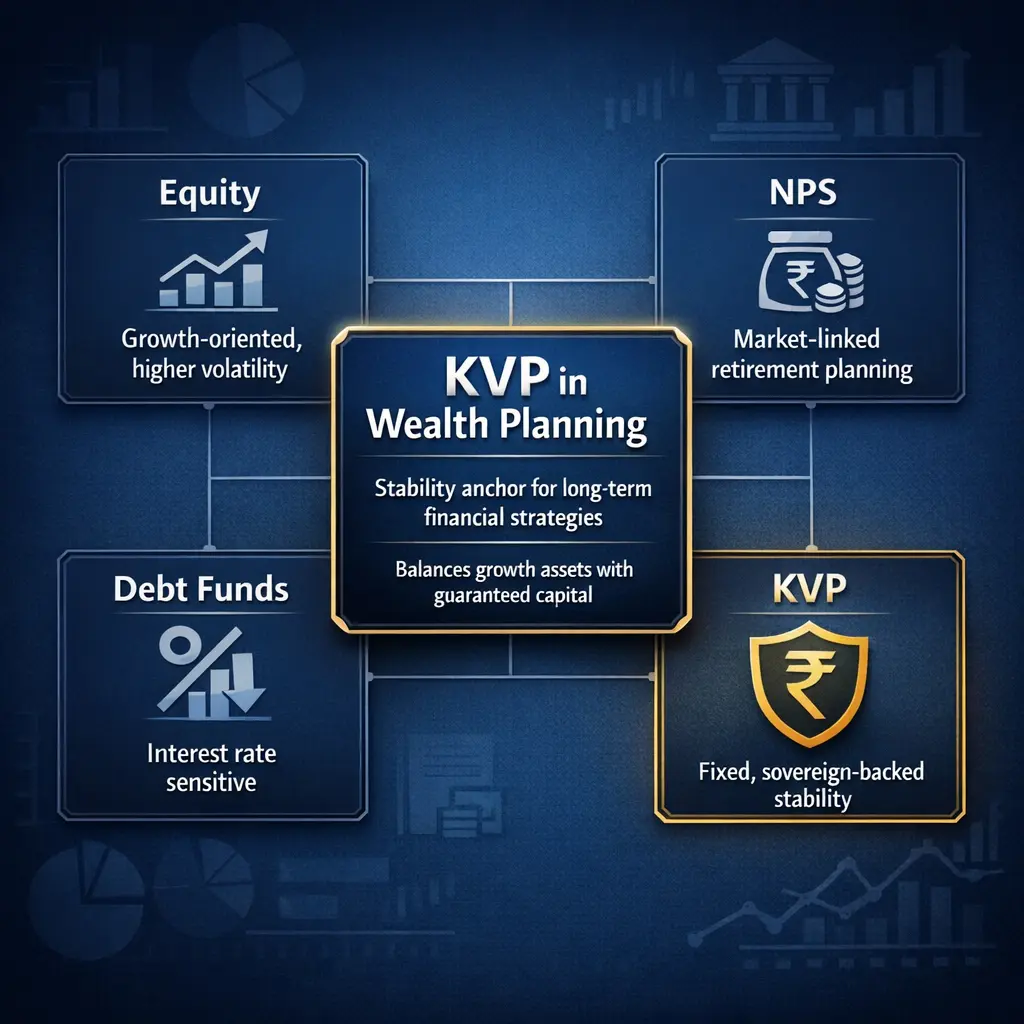

12. KVP vs National Pension System (NPS): Different Tools, Different Goals

KVP and the National Pension System (NPS) serve distinct roles within a long-term financial strategy. While KVP focuses on capital preservation and predictable growth, NPS is designed to provide retirement income through market-linked returns. Understanding their differences allows Indian professionals and long-term planners to strategically allocate resources for goal-specific outcomes, risk management, and portfolio diversification.

12.1 Capital Protection vs Market-Linked Growth

KVP guarantees the principal and accrues interest at a fixed rate, making it a low-risk, predictable instrument. NPS, on the other hand, exposes investments to equity, corporate bonds, and government securities, resulting in variable returns that depend on market performance.

Strategic insights:

- KVP ensures capital protection, ideal for conservative allocations

- NPS offers potential for higher long-term growth through equity exposure

- Combining KVP with NPS can balance stability with market-linked upside

12.2 Liquidity and Retirement Planning Implications

KVP provides moderate liquidity after the mandatory lock-in period, while NPS is primarily a retirement-focused vehicle with partial withdrawal rules. Investors need to consider horizon, cash-flow requirements, and emergency funds when integrating these instruments.

Advisory points:

- KVP can serve as a medium-term buffer before retirement

- NPS is best for long-term retirement accumulation with controlled withdrawals

- Proper sequencing of KVP and NPS ensures predictable cash-flow management

12.3 How KVP Complements NPS in a Diversified Portfolio

KVP can function as a stability anchor in a portfolio that includes NPS and other market-linked investments. By combining fixed, guaranteed returns with long-term growth strategies, investors can optimize risk-adjusted outcomes while preserving liquidity for mid-term goals.

Strategic takeaways:

- KVP reduces overall portfolio volatility when paired with NPS

- Provides predictable cash flows to complement retirement planning

- Supports a layered approach to asset allocation across fixed-income and market-linked instruments

13. Using KVP Strategically in Long-Term Wealth Planning

Kisan Vikas Patra (KVP) can play a key role in structured, goal-oriented wealth planning. Its predictability, guaranteed returns, and low-risk profile make it a reliable instrument for professionals and long-term planners looking to balance capital protection with broader portfolio growth. Strategic integration of KVP ensures that funds for medium- to long-term objectives are secure, while freeing higher-risk capital for growth-oriented investments.

13.1 Role of KVP in Asset Allocation and Risk Mitigation

KVP serves as a stability anchor in diversified portfolios, reducing overall risk while providing predictable cash flows. Its fixed returns help offset volatility from equities and market-linked instruments, ensuring more consistent portfolio performance over time.

Strategic considerations:

- Provides low-risk exposure to safeguard a portion of capital

- Balances equity and debt allocations for risk-adjusted returns

- Supports predictable cash flow for medium-term financial goals

- Helps maintain portfolio discipline during market volatility

13.2 Laddering KVP Investments for Predictable Cash Flows

Investors can stagger multiple KVP certificates with different purchase dates to create a laddered structure. This approach allows for periodic maturity payouts, aligning with recurring financial needs or reinvestment opportunities.

Practical laddering strategies:

- Stagger purchases to create overlapping maturity timelines

- Align maturities with medium-term goals like education or down payments

- Mitigate reinvestment risk by spreading certificates across periods

- Monitor ladder using tools like My Wealth Locker for efficiency

13.3 Combining KVP with Equity, NPS, and Debt Instruments

KVP is most effective when used in combination with other investment instruments, creating a layered portfolio that addresses growth, retirement, and capital preservation simultaneously. This strategic mix allows investors to meet long-term objectives while controlling risk exposure.

Portfolio integration points:

- Use KVP as the low-risk core while equities provide growth potential

- NPS complements retirement goals with market-linked returns

- Debt instruments can fill gaps in liquidity or short-term obligations

- Regular monitoring ensures alignment with evolving financial objectives

14. Managing and Tracking KVP Investments Efficiently

Efficient management of Kisan Vikas Patra (KVP) certificates is essential for long-term financial planning, especially when investors hold multiple certificates across different purchase dates. Maintaining accurate records, tracking maturity timelines, and planning reinvestments can be time-consuming and prone to error if done manually. Integrating modern digital tools, such as My Wealth Locker, allows investors to increase productivity, reduce errors, and maintain a consolidated view of all government-backed investments.

14.1 Organizing Physical and Digital KVP Certificates Securely

Proper organization of KVP certificates-both physical and digital-is critical to avoid loss, misplacement, or delayed maturity encashment. Structured record-keeping ensures smooth succession planning and prevents administrative errors.

Key organization practices:

- Maintain a secure storage system for physical certificates

- Digitize records to create backup and improve accessibility

- Track purchase dates, denominations, and serial numbers

- Regularly reconcile physical and digital records to reduce errors

14.2 Tracking Maturity Timelines and Reinvestment Opportunities Using My Wealth Locker

My Wealth Locker can simplify the monitoring of multiple KVP certificates, ensuring timely awareness of approaching maturities and potential reinvestment windows. Automated alerts and centralized dashboards improve planning accuracy and save time.

Productivity-enhancing practices:

- Set reminders for upcoming maturity dates and lock-in completion

- Monitor interest accruals and projected maturity value

- Identify opportunities for reinvestment in line with financial goals

- Reduce administrative errors through automated tracking

14.3 Consolidating Government Savings Instruments in One Personal Wealth Dashboard

A comprehensive dashboard consolidates KVP alongside other small savings instruments, providing a holistic view of portfolio performance, cash flows, and risk exposure. This integration allows professionals to manage multiple instruments efficiently without manual tracking.

Advisory points for consolidation:

- Combine KVP, NSC, and FD holdings for complete visibility

- Use dashboard insights to prioritize reinvestments and liquidity planning

- Monitor overall capital allocation and diversification across instruments

- Reduce oversight errors and ensure alignment with long-term goals

15. Digital Record-Keeping and Succession Planning for KVP

Effective record-keeping and succession planning are critical for Kisan Vikas Patra (KVP) investors, particularly when multiple certificates are held across family members or long-term goals. Accurate documentation ensures smooth transfer of proceeds, minimizes disputes, and prevents unclaimed investments. Leveraging digital tools like My Wealth Locker can streamline record management, track nominees, and maintain a consolidated view of all government savings instruments.

15.1 Importance of Documentation and Nominee Clarity

Clear documentation and properly designated nominees reduce the risk of delays or legal complications in transferring KVP proceeds. Investors should periodically review nominee details and ensure certificates are organized for easy access during emergencies or succession events.

Best practices:

- Maintain up-to-date nominee information for all certificates

- Store copies of certificates securely alongside original documents

- Keep a record of purchase dates, denominations, and issuing post offices

- Review documentation periodically to reflect family or financial changes

15.2 Avoiding Unclaimed Investments Through Centralized Tracking

Centralized tracking reduces the risk of unclaimed or forgotten KVP certificates. By recording all holdings digitally, investors and their successors can easily identify maturing certificates, ensure timely redemption, and allocate proceeds efficiently.

Practical steps for efficient tracking:

- Use a single digital platform for all KVP and other government-backed holdings

- Monitor maturity dates to prevent missed redemption opportunities

- Link certificate details to nominees for clarity during succession

- Employ automated alerts and dashboards via tools like My Wealth Locker

Optional Table: KVP Record-Keeping Checklist

| Task | Purpose | Frequency/Notes |

|---|---|---|

| Update nominee details | Ensure smooth succession | Review annually or after life events |

| Record certificate serial numbers | Avoid misplacement or duplication | At purchase and digitization |

| Track maturity and interest accrual | Plan reinvestment and cash flows | Quarterly review recommended |

| Maintain digital backup | Reduce risk of loss or damage | Continuous updates recommended |

This table provides a concise framework for investors to maintain accurate, secure, and actionable KVP records, minimizing risk and administrative errors while supporting long-term wealth planning.

16. Key Advantages and Limitations of KVP at a Glance

Kisan Vikas Patra (KVP) offers a simple, predictable, and low-risk savings option for Indian investors. Its structured nature and sovereign backing make it an effective instrument for medium- to long-term wealth planning. However, like all financial products, it has specific limitations that must be considered to align with individual goals and portfolio strategy.

Advantages of KVP

- Guaranteed principal and fixed returns backed by the Government of India

- Predictable doubling period allows disciplined, goal-based planning

- Low-risk instrument suitable for conservative investors and capital protection

- Easy to purchase and manage through post offices and authorized banks

- Supports succession planning via nominee designation

- Complements other instruments like NPS, FDs, and NSC in diversified portfolios

Limitations of KVP

- Interest earned is fully taxable, reducing post-tax returns for higher-income investors

- Mandatory lock-in period of 2 years 6 months limits short-term liquidity

- Returns may be lower than inflation during high inflation periods, affecting real growth

- Does not benefit from market-linked growth opportunities

- Not suitable as a tax-saving instrument under Section 80C

17. Conclusion

Kisan Vikas Patra (KVP) remains a reliable, low-risk savings instrument that prioritizes capital preservation and predictable returns. Its fixed doubling timeline and sovereign backing make it an ideal tool for professionals, conservative investors, and long-term planners seeking clarity and stability in their wealth-building strategies. By offering a disciplined approach to savings, KVP allows investors to plan medium- to long-term financial goals with confidence, without the uncertainty associated with market-linked instruments.

Beyond predictable growth, KVP encourages structured financial behavior. The mandatory lock-in period and clearly defined maturity value reinforce disciplined investment practices, while integration with tools like My Wealth Locker enhances productivity and accuracy in tracking multiple certificates, monitoring maturity timelines, and organizing government-backed instruments securely. This combination of simplicity, structure, and digital oversight ensures that investors can optimize both planning efficiency and capital safety.

In a diversified portfolio, KVP functions as a stability anchor, complementing higher-risk assets such as equities and market-linked retirement instruments. For Indian professionals and long-term wealth planners, it offers a dependable foundation for asset allocation, risk mitigation, and predictable cash flow, enabling informed decisions that align with both immediate financial needs and future financial objectives.

Interest rates, rules, and tax treatment are subject to change as per Government of India notifications. Investors should verify current terms before investing.